U.S. Broadcast Shakeup: New Calculus for K-Content

스트리밍 전환과 규제·정치 리스크, ‘규모 기반 최혜국 대우’ 질서 속에서 미국 방송 대재편이 K-콘텐츠의 유통·채널 전략에 미치는 영향

Trump Disrupts FCC Reform as TV Industry Consolidation Accelerates

Nexstar-TEGNA $6.2B merger, Sinclair-Scripps bid reshape distribution landscape | Trump blasts ABC, NBC as "virtual arm of the Democrat Party" | Conservative media divided over ownership rules | FAST channels and ATSC 3.0 emerge as new frontier for Korean content providers

US broadcast television is in the midst of its biggest transformation in decades. Squeezed by streaming competition and shrinking cable revenues, local TV stations are racing to consolidate. But what began as a business story has become a political one—with implications that extend far beyond U.S. borders.

For Korean media companies eyeing the American market, the upheaval demands attention. The rules governing who can own what in U.S. broadcasting are suddenly up for grabs, and the outcome will shape the distribution landscape for years to come.

American broadcast television is undergoing its most significant transformation in decades. Squeezed by streaming competition and shrinking cable revenues, local TV stations are racing to consolidate. But what started as a business story has become a political one—with implications that reach far beyond U.S. borders.

For Korean media companies eyeing the American market, the upheaval presents both challenges and unexpected opportunities. As traditional distribution models buckle under pressure, new pathways are opening up: FAST (Free Ad-Supported Streaming Television) channels and ATSC 3.0, the next-generation broadcast standard, are emerging as promising avenues for K-content to reach American audiences.

A Presidential Intervention

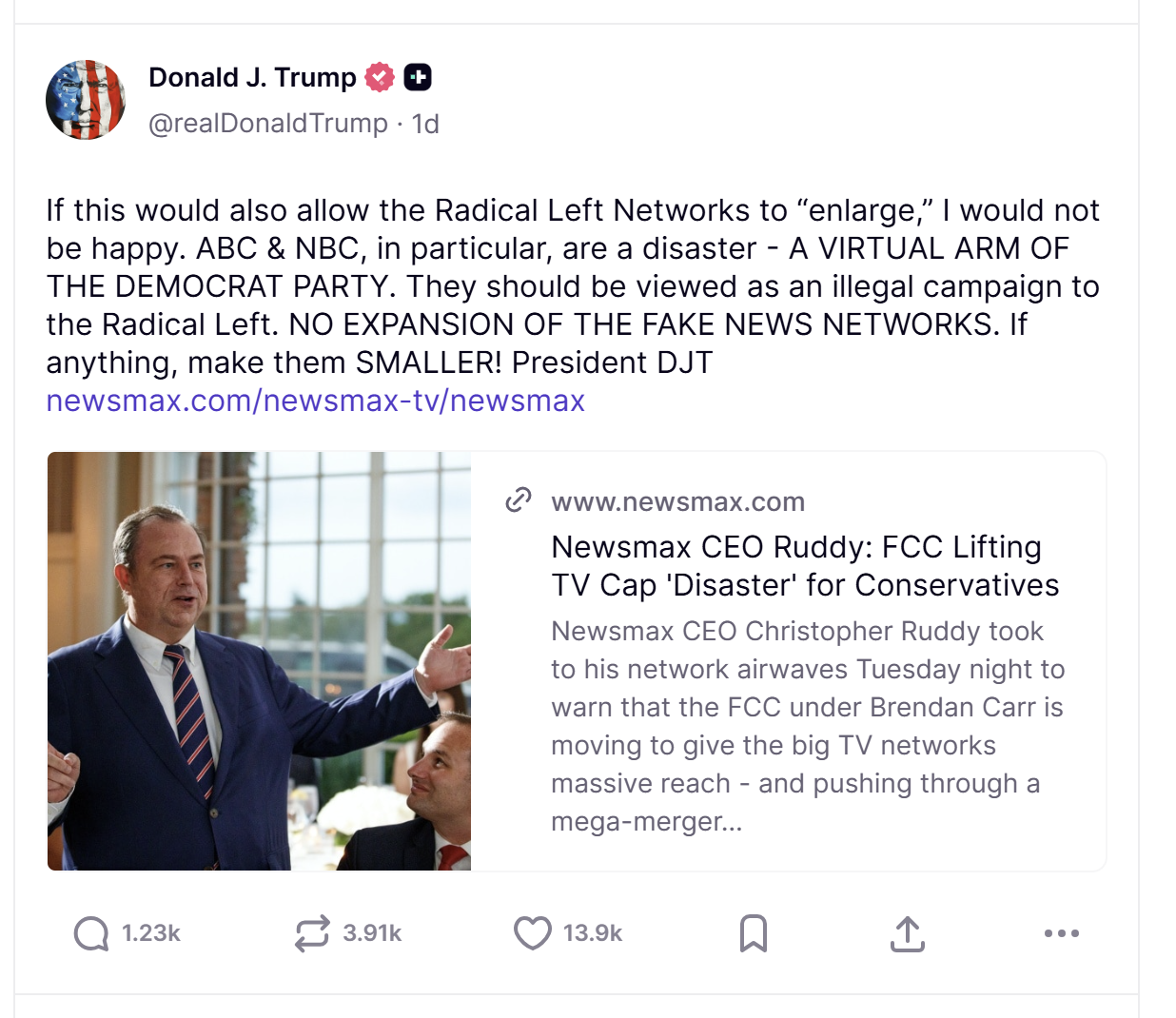

On November 24, President Donald Trump inserted himself into an obscure but consequential FCC regulatory debate—with characteristic bluntness.

"If this would also allow the Radical Left Networks to 'enlarge,' I would not be happy. ABC & NBC, in particular, are a disaster - A VIRTUAL ARM OF THE DEMOCRAT PARTY. They should be viewed as an illegal campaign to the Radical Left. NO EXPANSION OF THE FAKE NEWS NETWORKS. If anything, make them SMALLER! President DJT"

The Truth Social post followed a tense Oval Office exchange days earlier, when Trump called Disney-owned ABC a "crappy company" and told reporter Mary Bruce the network's broadcast license "should be taken away." He urged FCC Chairman Brendan Carr to "look at that."

Trump's comments aligned him with Newsmax CEO Chris Ruddy, who has been lobbying against FCC efforts to relax broadcast ownership limits. OAN CEO Charles Herring has taken the same position.

What's Actually at Stake

At the heart of the debate is the 39% cap—a rule preventing any single company from owning TV stations that reach more than 39% of American households.

Chairman Carr has pushed to modernize these rules, arguing they handicap local stations trying to survive in a streaming-dominated world. His stated goal: give local broadcasters more autonomy from network headquarters in New York and Hollywood.

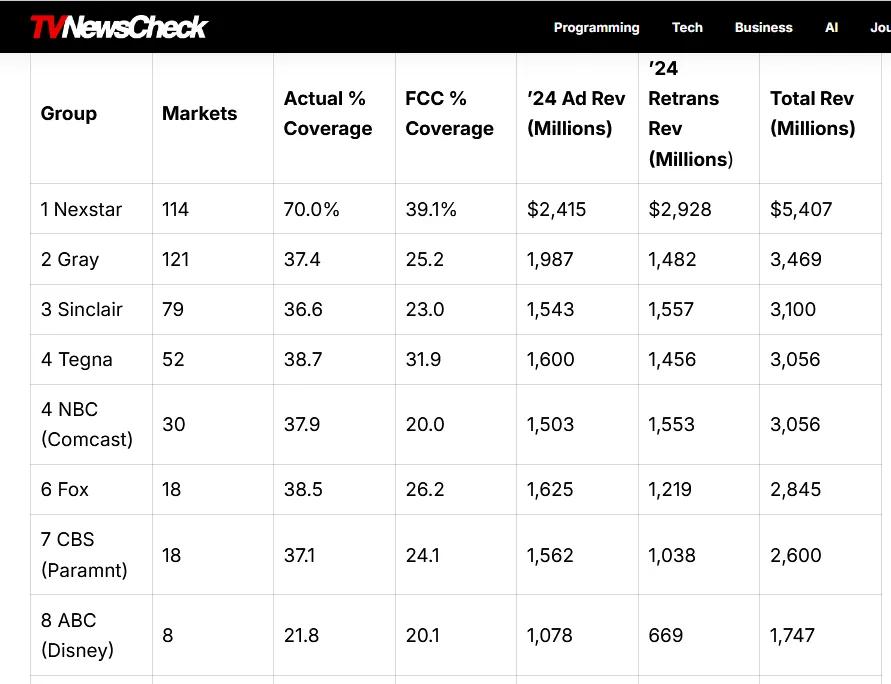

The Big Four networks aren't bumping against the ceiling. According to BIA Advisory Services, NBC reaches 20% of households, ABC 20.1%, CBS 24.1%, and Fox 26.2%. All have room to grow under current rules.

The real pressure point lies elsewhere. Nexstar Media Group, already at 39.1%, filed last month to acquire rival TEGNA for $6.2 billion. If approved, the combined company would reach 56.4% of U.S. households—well above the cap. Nexstar has requested a waiver.

A Conservative Family Feud

What makes this fight unusual is where the battle lines fall. This isn't liberals versus conservatives. It's conservatives versus conservatives.

Newsmax's Ruddy worries that relaxing ownership limits would create broadcast behemoths capable of capturing most of the carriage fees paid by cable and satellite operators. Channels like his, he fears, would be left with crumbs.

The National Association of Broadcasters sees it differently. "Ownership modernization is not about making national networks larger," said NAB communications chief Alex Siciliano. "It is about empowering local broadcasters that serve their communities with trusted news, emergency information and local journalism."

NAB's top lawyer, Rick Kaplan, was more pointed: "Newsmax isn't worried about local journalism; it's worried about competition. And it fears a stronger broadcast industry because a stronger broadcast industry might mean more conservative voices with larger audiences—voices with whom Newsmax would have to actually compete."

The Deals Keep Coming

Political uncertainty hasn't slowed the M&A train.

Sinclair Broadcast Group confirmed on November 24 that it had made an unsolicited offer for E.W. Scripps. The move came after Sinclair disclosed it had quietly accumulated an 8% stake in the Cincinnati-based broadcaster.

Scripps said its board would "carefully review" the proposal but warned it would take "all steps appropriate" to protect shareholders from "opportunistic actions." Its stock jumped 8.5% on the news.

For Sinclair, this is a second swing. The company had pursued TEGNA earlier this year before losing out to Nexstar's winning bid.

Why Consolidation Won't Stop

The consolidation wave isn't a choice—it's a necessity driven by multiple forces.

Cable TV subscribers keep leaving for streaming services, and they're not coming back. That means less advertising revenue for local stations and less leverage when negotiating retransmission fees with pay-TV operators. UBS estimates cable providers will lose another 1.7 million broadband subscribers this year alone.

But there's another factor accelerating the push for scale: the rollout of ATSC 3.0, also known as NextGen TV. This new broadcast standard requires significant capital investment in transmission infrastructure and equipment upgrades. Larger broadcast groups can spread these costs across more stations and move faster to capture the technology's potential.

Scale is the only defense. Bigger broadcast groups can demand better terms from cable companies, extract more favorable deals from networks, and invest in next-generation technologies. The math is unforgiving: consolidate or decline.

The Rise of FAST and ATSC 3.0

As traditional broadcast economics erode, two technological developments are reshaping the distribution landscape—and creating new openings for international content.

FAST channels have exploded in popularity. These free, ad-supported streaming services—think Pluto TV, Tubi, and Samsung TV Plus—offer linear programming without subscription fees. For viewers cutting the cord, FAST provides a familiar lean-back experience. For content owners, it offers a new revenue stream and audience reach.

U.S. broadcasters are jumping in. Major station groups are launching their own FAST channels, repurposing local content and seeking programming to fill schedules. Korean content, with its proven global appeal and extensive library depth, fits naturally into this ecosystem.

ATSC 3.0 represents an even more significant shift. Unlike the current broadcast standard, NextGen TV is IP-based, enabling broadcasters to deliver internet-like services over the airwaves—including targeted advertising, on-demand content, and datacasting. Crucially, it can reach mobile devices without requiring cellular data.

For Korean content providers, ATSC 3.0 opens intriguing possibilities. The standard's hybrid broadcast-broadband architecture could enable Korean channels or content packages to reach American viewers through local broadcast infrastructure—a distribution model that bypasses traditional gatekeepers.

Several major U.S. broadcast groups are actively seeking content partnerships to populate their ATSC 3.0 multicasts. As these groups consolidate and gain scale, their appetite for differentiated programming—including international content—is likely to grow.

The K-Content Opportunity

The turbulence in American broadcasting isn't just a challenge to navigate. It's a landscape being reshaped in ways that could favor Korean content providers willing to move strategically.

FAST as the new frontier. Korean dramas, variety shows, and films have already gained traction on FAST platforms. As U.S. broadcasters launch their own FAST services to compensate for linear declines, demand for proven content libraries will increase. Korean suppliers with extensive catalogs and competitive pricing are well-positioned.

ATSC 3.0 partnerships. The next-generation broadcast standard creates opportunities for Korean channels to establish direct-to-viewer presence in the U.S. market through partnerships with local broadcast groups. This could prove particularly valuable for Korean content seeking to reach audiences beyond the coastal metros where K-content awareness is already high.

Consolidation cuts both ways. Yes, larger broadcast groups will have more negotiating leverage. But they'll also have more channels to fill, more FAST services to program, and more ATSC 3.0 multicasts to populate. Scale creates appetite for content volume.

Political risk requires monitoring. The Trump administration has made clear that media policy is inseparable from political considerations. Korean firms should track regulatory developments and factor uncertainty into long-term commitments. Flexibility and optionality have value.

First-mover advantages are available. The ATSC 3.0 rollout is still in relatively early stages. Korean broadcasters and content companies that establish partnerships now—while U.S. station groups are actively seeking programming—may secure more favorable terms than latecomers.

Looking Ahead

Trump's intervention has complicated what was already a difficult regulatory process. FCC Chairman Carr's vision of empowered local broadcasters now collides with the president's hostility toward major networks and the survival anxieties of smaller conservative outlets.

But the underlying forces driving consolidation aren't going anywhere. Streaming has permanently altered viewing habits. Digital platforms continue to capture advertising dollars. Local broadcasters must get bigger or risk irrelevance.

At the same time, the technologies reshaping American broadcasting—FAST and ATSC 3.0—are creating distribution pathways that didn't exist five years ago. For international content providers, these represent genuine opportunities to reach U.S. audiences in new ways.

The restructuring of American television is underway, and it won't wait for Washington to sort out its politics. For Korean media companies, the moment calls for both caution and opportunism: careful monitoring of regulatory flux, combined with proactive engagement on emerging platforms.

The broadcast landscape is being redrawn. Those who understand the new map will be best positioned to navigate it.

미국 방송 대재편 정치경제학: 트럼프 개입으로 FCC 규제 완화 '안갯속'

스트리밍 전환에 생존 위기 맞은 美 지역방송, 대형화로 돌파구 모색 | 넥스타-테그나 62억弗 합병, 싱클레어-스크립스 M&A 추진 속 39% 시청가구 상한 규제가 핵심 변수로 | 트럼프 "ABC·NBC 확장 안 돼, 더 작게 만들어라" 직접 개입에 보수 진영 내 이해충돌 노출 | 뉴스맥스·OAN vs NAB, 같은 보수인데 왜 다른 목소리? | 정치와 규제, 미디어 산업의 삼각구도가 만드는 불확실성…K-콘텐츠 미국 진출 전략에도 함의

미국 방송 TV 산업이 역사적 전환점에 서 있다. 스트리밍 서비스의 급부상으로 케이블TV 가입자가 급감하면서 지역 방송국들의 수익 기반이 흔들리고, 이에 대응한 업계의 대형 M&A가 연쇄적으로 추진되고 있다. 그러나 도널드 트럼프 대통령이 연방통신위원회(FCC)의 소유 규제 완화에 제동을 거는 발언을 내놓으면서, 미국 방송 산업의 구조 재편은 정치적 변수까지 더해진 복잡한 방정식이 됐다.

이 과정에서 드러난 보수 진영 내부의 이해충돌, 대형 방송 그룹과 소규모 케이블 채널 간의 갈등, 그리고 규제 당국과 백악관의 엇갈린 시그널은 미디어 산업에서 정치와 비즈니스가 어떻게 교차하는지를 보여주는 전형적 사례다. 한국 미디어 기업들의 미국 시장 진출 전략에도 중요한 시사점을 던진다.

트럼프, "급진 좌파 TV 네트워크 확장 절대 안 돼"

트럼프 대통령은 24일(현지시간) 자신의 소셜미디어 트루스소셜(Truth Social)을 통해 디즈니 소유의 ABC와 컴캐스트 소유의 NBC를 직접 거명하며 강도 높은 비판을 쏟아냈다.

"만약 이것이 급진 좌파 네트워크들의 '확장'도 허용한다면, 나는 기쁘지 않을 것이다. 특히 ABC와 NBC는 재앙이다 - 사실상 민주당의 한 부서다. 그들은 급진 좌파를 위한 불법 선거운동으로 간주되어야 한다. 가짜 뉴스 네트워크의 확장은 절대 안 된다. 굳이 하려면, 더 작게 만들어라! 도널드 J. 트럼프 대통령"

"If this would also allow the Radical Left Networks to 'enlarge,' I would not be happy. ABC & NBC, in particular, are a disaster - A VIRTUAL ARM OF THE DEMOCRAT PARTY. They should be viewed as an illegal campaign to the Radical Left. NO EXPANSION OF THE FAKE NEWS NETWORKS. If anything, make them SMALLER! President DJT"

트럼프의 발언은 뉴스맥스(Newsmax) CEO 크리스 러디의 입장을 사실상 지지한 것으로, 브렌던 카 FCC 위원장이 추진해온 규제 현대화 작업에 찬물을 끼얹는 형국이다. 지난주 백악관에서 ABC뉴스 기자 메리 브루스와 대면한 자리에서도 트럼프는 디즈니/ABC를 "형편없는 회사(crappy company)"라고 지칭하며 "뉴스가 너무 가짜여서 방송 면허를 취소해야 한다"고 언급했고, "우리의 훌륭한 FCC 위원장 브렌던 카가 이를 검토해야 한다"고 압박한 바 있다.

| 그룹 | 시장 수 | 실제 커버리지(%) | FCC 커버리지(%) | 2024년 광고 수익(백만달러) | 2024년 재송신 수익(백만달러) | 총수익(백만달러) |

|---|---|---|---|---|---|---|

| Nexstar | 114 | 70.0 | 39.1 | 2,415 | 2,928 | 5,407 |

| Gray | 121 | 37.4 | 25.2 | 1,987 | 1,482 | 3,469 |

| Sinclair | 79 | 36.6 | 23.0 | 1,543 | 1,557 | 3,100 |

| Tegna | 52 | 38.7 | 31.9 | 1,600 | 1,456 | 3,056 |

| NBC (Comcast) | 30 | 37.9 | 20.0 | 1,503 | 1,553 | 3,056 |

| Fox | 18 | 38.5 | 26.2 | 1,625 | 1,219 | 2,845 |

| CBS (Paramount) | 18 | 37.1 | 24.1 | 1,562 | 1,038 | 2,600 |

| ABC (Disney) | 8 | 21.8 | 20.1 | 1,078 | 669 | 1,747 |

39% 규제의 본질: 지역 방송 vs 네트워크의 권력 구도

논쟁의 핵심인 '39% 상한선'은 단일 방송사가 도달할 수 있는 전국 TV 시청가구 비율의 상한을 규정한다. 이 규제는 특정 방송 그룹의 과도한 시장 지배력을 방지하기 위해 도입됐으나, 스트리밍 시대에 그 실효성과 적정 수준에 대한 논쟁이 재점화됐다.

카 FCC 위원장은 이 규제의 현대화를 추진하며, 목적이 지역 TV 방송국들에게 뉴욕과 할리우드의 네트워크 경영진이 지시하는 프로그래밍 결정에 저항할 수 있는 권한을 부여하는 것이라고 설명해왔다. 즉, 지역 방송국의 자율성 강화가 명분이다.

BIA 어드바이저리 서비스에 따르면, 현재 4대 네트워크의 시청가구 도달률은 NBC 20%, ABC 20.1%, CBS 24.1%, Fox 26.2%로 모두 상한선에 상당한 여유가 있다. 트럼프가 우려하는 네트워크 확장이 당장 현실화될 가능성은 높지 않은 셈이다.

문제는 지역 방송 그룹들이다. 미국 최대 TV 방송사 넥스타 미디어 그룹은 이미 39.1%로 상한선을 넘어선 상태에서 지난 11월 18일 테그나(TEGNA)와의 합병 신청서를 FCC에 제출했다. 합병이 성사되면 시청가구 도달률은 56.4%에 달해 현행 규정을 크게 초과하게 되며, 넥스타는 규정 면제를 신청한 상황이다.

보수 진영의 균열: 뉴스맥스 vs NAB

이번 논쟁이 흥미로운 이유는 보수 진영 내부의 이해충돌을 적나라하게 드러내기 때문이다.

뉴스맥스 CEO 크리스 러디는 규제 완화가 "보수 진영에 재앙"이 될 것이라고 주장하며 반대 캠페인을 주도하고 있다. 원아메리카뉴스네트워크(OAN) CEO 찰스 헤링도 러디의 입장에 동조한다.

러디의 우려는 이중적이다. 첫째, 4대 네트워크의 영향력 확대 가능성. 둘째, 더 실질적인 문제로, 넥스타-테그나 같은 거대 방송 그룹(합병 시 265개 방송국 보유)이 컴캐스트, 디렉TV 등 유료TV 사업자들이 지급하는 송출료(carriage fee)의 대부분을 가져가면, 뉴스맥스 같은 소규모 케이블 뉴스 채널에는 "부스러기조차 남지 않을 것"이라는 계산이다.

이에 대해 전미방송협회(NAB)는 정면 반박에 나섰다. NAB 커뮤니케이션 수석부사장 알렉스 시실리아노는 "소유 규정 현대화는 전국 네트워크를 더 크게 만드는 것이 아니라, 지역사회에 신뢰할 수 있는 뉴스와 재난 정보, 지역 저널리즘을 제공하는 지역 방송사들에게 권한을 부여하는 것"이라고 강조했다. 그는 "이 구시대적 규정은 네트워크를 제한하는 게 아니라 생존하려는 지역 방송국을 제한한다"며 "크리스 러디의 오해를 유발하는 캠페인은 자신의 방송국처럼 이미 전국 100%에 도달하는 채널과 같은 경쟁의 장에 서려는 지역 방송사들을 막으려는 것"이라고 지적했다.

NAB 수석법률책임자 릭 카플란은 더 직설적이었다. "뉴스맥스는 지역 저널리즘이 아니라 경쟁을 걱정하는 것이다. 더 강력한 방송 산업은 더 큰 청중을 가진 보수 목소리를 의미할 수 있고, 뉴스맥스는 그들과 실제로 경쟁해야 할 것을 두려워한다."

싱클레어-스크립스: M&A 도미노의 다음 타자

규제 논쟁이 진행되는 와중에도 업계 재편은 멈추지 않고 있다. 싱클레어 브로드캐스트 그룹이 E.W. 스크립스에 비요청(unsolicited) 인수 제안을 한 것이 24일 확인됐다.

싱클레어는 지난주 스크립스 지분 약 8%를 확보했다고 공시하며 양사 간 "건설적인 협의"가 있었다고 밝힌 바 있다. 스크립스는 "제안을 신중히 검토하고 평가할 것"이라면서도 "싱클레어나 누구든 기회주의적 행동으로부터 회사와 주주를 보호하기 위해 적절한 모든 조치를 취할 것"이라고 경고했다.

시장은 일단 긍정적으로 반응했다. 스크립스 주가는 8.5% 상승한 4.47달러를 기록했고, 싱클레어는 0.8% 하락한 15.53달러에 마감했다. 월스트리트저널에 따르면 싱클레어는 지난 8월 테그나 인수도 모색했으나 넥스타에 밀린 바 있어, 이번 스크립스 인수전은 재도전의 성격을 띤다.

왜 대형화인가: 스트리밍 시대의 생존 방정식

미국 지상파 방송 TV 업계의 통합 움직임은 구조적 압박의 산물이다. 케이블TV 가입자들이 넷플릭스, 디즈니+, 아마존 프라임 등 스트리밍 서비스로 지속 이동하면서, 지역 방송국들은 이중의 수익 압박에 시달리고 있다.

첫째, 광고 수익 감소. 시청자 이탈은 곧 광고 단가 하락으로 이어진다. 둘째, 재송신료(retransmission fee) 축소. 케이블·위성 사업자들이 가입자 감소를 이유로 방송국에 지급하는 재송신료 인상을 거부하거나 삭감을 요구하고 있다. UBS는 2025년 케이블 ISP들이 170만 명의 브로드밴드 가입자를 잃을 것으로 전망했다.

업계의 대응 논리는 명확하다. 대형화를 통해 협상력을 확보하자는 것이다. 같은 시장 내 더 많은 방송국을 보유하면 케이블 사업자와의 재송신료 협상에서 유리한 고지를 점할 수 있고, 4대 네트워크와의 프로그램 수급 협상에서도 더 나은 조건을 이끌어낼 수 있다.

넥스타가 테그나를 62억 달러에 인수하기로 한 것도, 싱클레어가 스크립스에 손을 뻗은 것도 모두 이 생존 방정식의 연장선이다.

아울러 최근 스포츠 스트리밍 플랫폼 푸보(Fubo) TV와 NBC간 채널 송출 분쟁(Black out)이 발생한 이유도 방송 시장 구조 개편의 영향이다. 미국 방송 시장에서 지상파 방송의 영향력은 예전 같지 않다. 특히, 일정 규모에 달성하지 못한 방송 그룹은 협상력이 더욱 약화된다. 미국에서 ‘규모 기반 최혜국 대우’라는 말이 나오는 것도 같은 이유다.

푸보TV–NBC 블랙아웃은 한마디로 “규모가 협상 결과를 좌우하는 새 질서”가 만들어낸 사건으로 볼 수 있다. 스포츠 중계권을 쥔 NBC유니버설이 높은 전송료와 채널 번들 조건을 요구하자, 상대적으로 가입자 규모가 작은 스포츠 특화 스트리밍 사업자인 푸보TV가 이를 감당하지 못해 송출 중단(블랙아웃)으로 이어진 것이다.

예전 같으면 지상파 채널이 빠지는 블랙아웃은 가입자 대규모 이탈로 직결될 일대 사건이었지만, 이제 상당수 시청자가 스트리밍·다른 디지털 경로를 통해 콘텐츠를 소비하기 때문에, 플랫폼들도 “더 이상 어떤 가격과 조건에서도 지상파를 붙들 필요는 없다”는 계산을 하기 시작했다. 그 결과, 예전보다 영향력은 줄었지만, 일정 수준 이상 규모를 가진 플레이어에게만 상대적으로 좋은 조건이 돌아가는, 양극화된 협상 구조가 고착되는 방향으로 시장이 재편되고 있다.

한국 미디어 산업에 주는 시사점

미국 방송 시장의 이 같은 격변은 K-콘텐츠의 글로벌 전략에도 중요한 함의를 던진다.

물론 미국 지역 지상파 환경 변화는 현재로서는 K-콘텐츠와 한국계 채널에 직격탄이라기보다, 구조와 규칙을 바꾸는 간접 영향에 가깝다는 전제를 먼저 둘 필요가 있다. 이미 K-콘텐츠의 주요 수익·인지 경로가 넷플릭스, 디즈니+, 아마존 프라임, FAST 등 스트리밍 중심으로 이동해 있기 때문에, 지역 방송 M&A나 39% 규제 논쟁이 단기적으로 편성 물량을 크게 줄이는 방향으로 작동하고 있지는 않다. 대신, 이 논쟁은 향후 어느 주체가 시청·데이터·광고 권력을 쥐게 될지, 그리고 그 권력 구조 위에서 K-콘텐츠가 어떤 포지션을 차지할 수 있을지를 재정의하는 간접 변수로 작동하고 있다.

이 전제를 깔면, 현재 미국 방송 시장 재편이 한국 미디어 산업에 주는 시사점은 ‘직접 시장 축소’가 아니라 ‘협상 구조·기술 인프라·규제 프레임 변화에 따른 전략 재설계’로 정리된다. 즉 미국 방송 시장의 판이 바뀌는 만큼 우리 콘텐츠의 미국 미디어 시장 진출 방법도 다변화되어야 한다.

특히, 지역 방송 그룹의 대형화는 K-콘텐츠 채널과 프로그램이 들어갈 수 있는 지상파·케이블TV 슬롯의 절대량보다, 어떤 플레이어와 어떤 조건으로 딜을 맺게 될지를 바꾸는 쪽에 더 큰 의미가 있다.

동시에 미국 시청의 60% 이상이 이미 스트리밍을 통해 이뤄지고, FAST와 광고형 스트리밍 비중이 빠르게 늘어나는 상황에서, K-콘텐츠는 유료방송·안테나 기반의 전통 지상파보다 스트리밍과 디지털-로컬(스트리밍 기반 지역 뉴스·채널) 환경에 더 깊게 연동되는 구조로 진화하고 있다

이를 위해 다음 전략을 염두에 둘 필요가 있다.

첫째, 유통 채널 재편에 대한 모니터링이 필요하다. 넥스타-테그나, 싱클레어-스크립스 등 대형 방송 그룹의 탄생은 미국 지상파·케이블 유통 협상 구도를 바꿀 수 있다. 협상 상대가 대형화되면 콘텐츠 공급자의 교섭력은 상대적으로 약화될 수 있다.

둘째, 정치 리스크의 상수화다. 트럼프 행정부에서 미디어 정책이 정치적 고려와 긴밀히 연동되는 양상은 한국 기업들이 미국 시장 진출 시 규제 환경의 불확실성을 감안해야 함을 보여준다. FCC 위원장의 정책 방향과 백악관의 정치적 판단이 충돌할 수 있다는 점도 변수다.

셋째, FAST(무료 광고 기반 스트리밍) 채널의 전략적 가치 재평가다. 전통 방송의 수익 기반이 흔들리는 상황에서 FAST 채널은 새로운 유통 경로로 부상하고 있다. 한국 콘텐츠 기업들이 미국 지역 방송국 그룹들과의 FAST 채널 파트너십을 모색할 경우, 이들 그룹의 M&A 결과에 따라 협력 구도가 달라질 수 있다. 수익 모델과 포트폴리오 측면에서는 FAST와 스트리밍, 그리고 ATSC 3.0이 결합된 다층 유통 전략이 핵심 과제로 부상한다.

미국 전통 방송의 광고와 재송신료 기반이 약화되는 상황에서 FAST는 광고 기반 수익과 브랜드 인지도를 동시에 확보할 수 있는 동시에, 지역 방송 그룹 입장에서는 기존 채널 자산을 디지털로 확장하는 교두보 역할을 한다. 한국 콘텐츠 기업이 지역 방송 그룹과 K드라마, K푸드, K컬처를 반영한 FAST 채널 제휴를 추진한다면, 지상파·케이블·FAST·SVOD를 묶은 복합 패키지 설계, 에피소드·시즌별 차별 유통, 데이터 기반 타겟팅 광고와의 연동 등 보다 정교한 수익 분배 구조 설계가 필요하다.

ATSC 3.0은 이 간접 구조를 강화하는 기술적 축으로 이해할 수 있다. 미국 주요 시장에서 상용화가 진행 중인 ATSC 3.0은 지상파를 IP 기반·양방향·데이터캐스팅 가능한 플랫폼으로 전환해, 방송국들이 자체 스트리밍 앱·하이브리드 채널·타깃 광고·부가 데이터 서비스를 결합할 수 있게 한다. 만약 ATSC 3.0을 통해 미국 지역 지상파 방송에 K콘텐츠가 공급될 수 있다면 한국 콘텐츠의 미국 방송 시장 진입은 또 다른 차원에 진입하게 된다.

이는 K-콘텐츠 입장에서 “새로운 전통 채널”이라기보다, 지상파 인프라를 활용한 스트리밍·데이터 서비스의 확장판에 가깝고, 한국 사업자는 프로그램 공급에 더해 ATSC 3.0 기반 전용 채널, 로컬 타깃 광고 연동형 콘텐츠, 데이터캐스팅을 활용한 팬덤·이벤트 연계 서비스 등으로 진출 옵션을 확장할 수 있다

넷째, 규제 프레임의 글로벌 확산 가능성이다. 미국에서 '시청가구 도달률 상한' 같은 소유 규제가 어떻게 진화하는지는 다른 국가들의 미디어 규제 논의에도 참고 사례가 된다. 한국의 방송 소유 규제 논의에서도 스트리밍 시대의 시장 획정, 플랫폼과 콘텐츠의 수직 결합 등 유사한 이슈가 부상할 수 있다.

전망: 불확실성 속의 구조 재편

"트럼프 행정부의 직접 개입으로 FCC의 39% 시청가구 상한 규제 개편은 정치·규제·산업 이해가 중첩된 고차 방정식으로 전환되었다. 브렌던 카 위원장이 제시한 지역 방송국 경쟁력 제고라는 정책 목표와, 트럼프 대통령의 전국 네트워크 견제라는 정치적 동인이 충돌하는 과정에서, 뉴스맥스·OAN·NAB 등 이해당사자 간 갈등 구도가 미국 방송 규제 논의의 핵심 변수로 부상하고 있다.

한편, 스트리밍 중심 시청 행태 확산과 광고·유료TV 시장의 구조적 위축은 규제 방향과 무관하게 방송사의 대형화·통합 압력을 지속적으로 증폭시키고 있다. 넥스타-테그나, 싱클레어-스크립스 사례에서 보듯, 사업자들은 법정 상한선과 면제, 지분투자, 제휴 구조 등을 활용해 사실상 전국 통합에 가까운 스케일을 확보하려는 전략을 가속화하고 있다. 이는 향후 일정 기간 미국 지역 방송 산업의 구조 재편을 상수로 만들 가능성이 크다.

이런 변화는 미국 국내 시장을 넘어 글로벌 미디어 가치사슬과 콘텐츠 유통 질서에 직·간접적 파급효과를 미칠 수 있다.

특히 K-콘텐츠 기업의 경우, 지역 방송 그룹의 대형화로 인한 협상 구조 변화, 정치적 리스크 상수화, FAST 채널 및 스트리밍 기반 파트너십, ATSC3.0 활용 등의 재편 가능성을 전제한 중장기 진출 전략 재설계가 필요하다. 결국 미국 방송 산업의 재편 과정은 단기 이슈를 넘어 향후 10년간 글로벌 콘텐츠 산업의 권력 구조와 시장 접근 전략을 규정하는 핵심 변수로 작동할 것으로 판단된다."