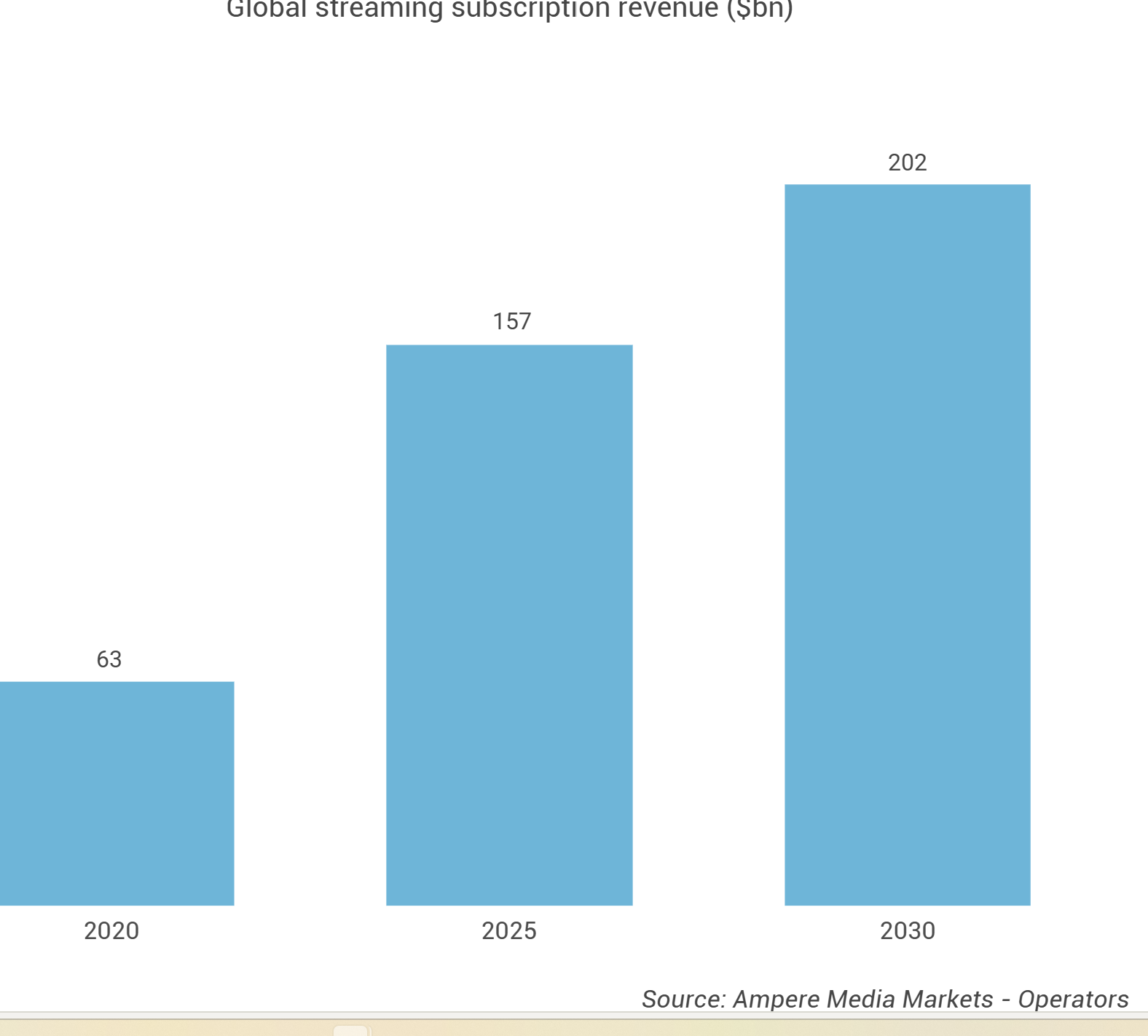

2025 global subscription revenue $157bn · Including advertising $177bn · 2030 subscription forecast $202bn | As subscriber growth plateaus, platforms pivot to monetizing existing users

April 2, 2026 | Sources: Ampere Analysis · WSJ · LA Times · Deloitte

Global Streaming Subscription Revenue ($bn) — Ampere Analysis

Source: Ampere Analysis (2026)

The Subscriber Race Is Over

The data from Ampere Analysis reflects exactly where the streaming industry now stands. Global streaming subscription revenue grew 14% year-on-year in 2025, reaching $157bn. That is 2.5 times the $63bn recorded in 2020. By 2030 the figure is forecast to exceed $202bn.

Jung Han

Jung Han

But the numbers tell a subtler story than they appear. Two or three years ago, the streaming industry's defining metric was monthly active subscribers (MAU). Whether Netflix crossed 200 million, or was heading toward 300 million, shaped stock prices and investor sentiment. That calculus has changed.

"As the streaming market matures, the emphasis is no longer on pure subscriber growth but on extracting greater value from existing audiences. This growth is particularly pronounced in the most competitive markets."— Lauren Liversedge, Senior Analyst, Ampere Analysis

'The most competitive markets' means, above all, the United States. The U.S. accounted for 50% of global streaming subscription revenue in 2025. A single country claiming half the world's total is itself a measure of how deeply mature this market has become.

The explosion of ad-supported subscription tiers is the defining structural indicator of this shift. In the U.S. and Western Europe, the revenue share coming from ad-inclusive plans surged from under 5% in 2020 to 28% in 2025. Cost-conscious consumers moved to cheaper ad-supported options — and platforms converted that migration into a dual-revenue structure, collecting subscription fees and advertising dollars simultaneously. Ampere Analysis notes that this cost-sensitive behavior is no longer confined to North America: it has spread broadly across Western Europe.

By 2030: $202bn in Subscriptions, $42bn in Ads, $244bn Total

Ampere Analysis forecasts that global streaming subscription revenue will surpass $202bn by 2030 — a further 29% growth from 2025 levels. Advertising alone is projected to contribute an additional $42bn per year. Combined, total addressable revenue exceeds $244bn.

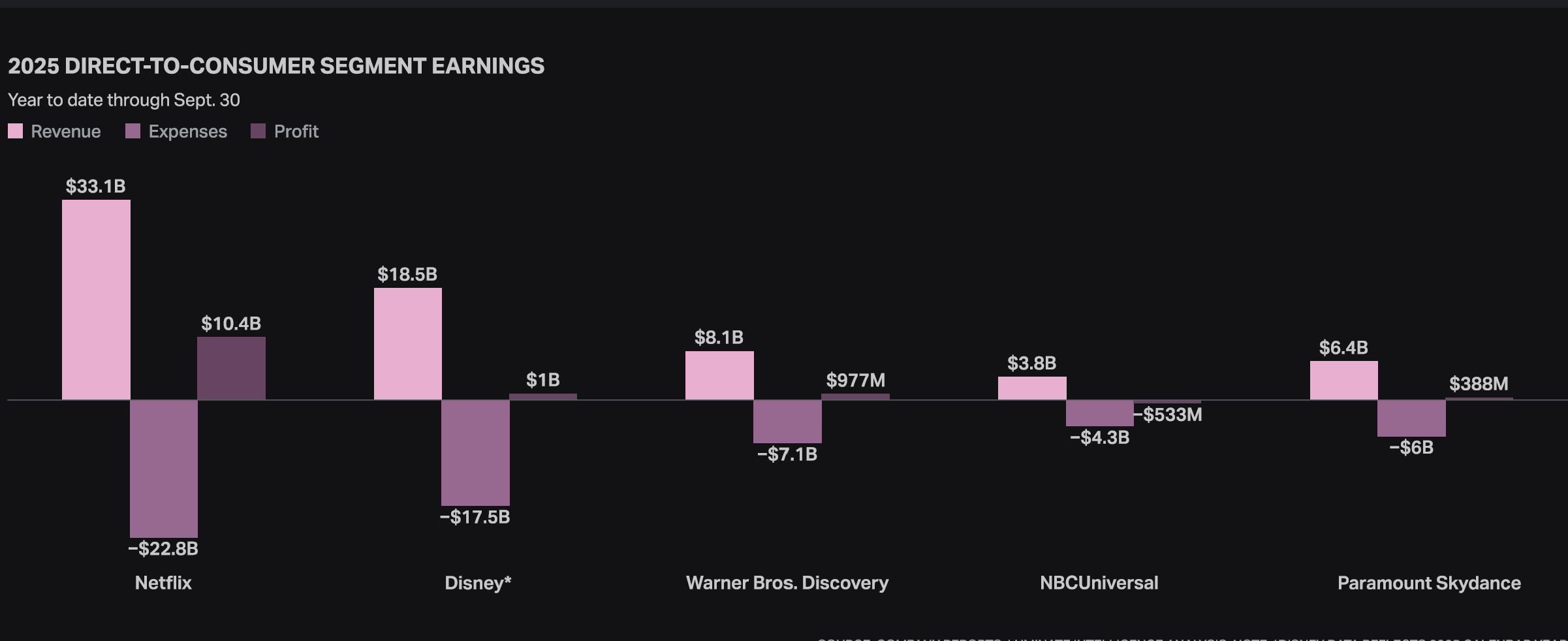

Netflix's competitive position in this market is defined by three numbers. 325 million — the largest subscriber base of any streaming platform. 28% — the share of revenue already flowing from ad-supported tiers, the foundation of its advertising business. 2 minutes per hour — current ad load, the lowest among major streamers, representing substantial room to grow. These three levers — pricing, ad monetization, and live sports inventory — are the architecture of Netflix's play in a $244bn market.

The era of chasing subscriber counts is over. The era of monetizing the subscriber base you already have has begun. Netflix did not invent this transition. It moved faster than anyone else to build the infrastructure for it.

Why Netflix Raised Prices Again

Netflix raised subscription prices again last month — the second increase in just over a year. On the surface it looks like a routine rate adjustment. Look at the structure of the increases, and a precise strategy emerges.

The ad-supported Standard plan rose by just $1. The ad-free Standard and Premium plans each went up $2. Premium now sits at $26.99 per month. The larger increases on higher-priced tiers are deliberate: widening the price gap between ad-supported and premium plans nudges subscribers who balk at the cost to downgrade to ad-supported options rather than cancel — keeping them on the platform while simultaneously building the advertising business.

Netflix offered a measured official response:

"Our approach remains the same: we continue offering a range of prices and plans to meet a variety of needs, and as we deliver more value to our members we are updating our prices to enable us to reinvest in quality entertainment and improve their experience."— Netflix spokesperson, official statement

Netflix is not acting alone. Disney+, HBO Max, and Apple TV+ all made similar pricing moves last year. Price increases combined with the simultaneous rollout of ad tiers is now a platform-wide structural pattern, not an outlier move.

Deloitte data puts the consumer response in context: the average U.S. streaming household spends $69 per month — unchanged from a year ago. Subscribers are holding their total spend flat by trading down to cheaper plans or dropping services entirely. The consequence: more than two-thirds of streaming subscribers now choose ad-supported plans, a 20% increase versus 2024. Netflix is not fighting this trend. It is monetizing it.

Michael Smith, professor of information technology and public policy at Carnegie Mellon University, frames the shift plainly in a media interview: "Streaming platforms can observe consumers' price responses in real time. The era of gut-feeling price decisions made with limited data is over." Netflix's pricing decisions are now an algorithmic exercise, calibrated against behavioral data from 325 million subscribers.

One additional lever remains largely undeployed: ad load. Netflix currently runs approximately two minutes of advertising per viewing hour — the lowest of any major streamer, per Ampere Analysis. The room to increase ad density is substantial. It means Netflix's advertising revenue upside has not yet fully surfaced.

Sports Are Not About Subscribers. They Are About Ad Inventory.

Reading Netflix's aggressive push into live sports rights purely as a subscriber retention play misses half the picture. The real value of live sports is advertising inventory. Tens of millions of viewers watching the same moment simultaneously is almost the only content format where advertisers willingly pay premium CPMs — and Netflix is building that capability systematically.

Netflix currently holds a package of two NFL Christmas Day games, paying roughly $75 million per game. That three-year deal is in its final season. According to the Wall Street Journal, Netflix is now in active negotiations to double its NFL footprint to four games. The two additional targets are a newly created Thanksgiving Eve game and an international game during opening week — rights that the NFL reclaimed when it sold NFL Network to ESPN as part of a deal that also gave the league a minority stake in ESPN itself.

Competition for these rights is multi-party. YouTube, which already holds NFL Sunday Ticket and carried an international game last season, has expressed interest in additional inventory. Amazon, which owns Thursday Night Football, is also open to more. Legacy broadcasters CBS, NBC, and Fox remain potential bidders.

Last week's MLB Opening Day stream was as much a live data exercise as a broadcast event. Netflix was measuring concurrent viewership scale, advertiser response, and how much premium ad pricing the market will absorb for live sport — tested in real time against an audience of 325 million subscribers. With ad load currently at just two minutes per hour, the growth potential is significant.

Streaming Is Rewriting the Sports Rights Landscape

Netflix's sports expansion is not happening in isolation — it is part of a structural reordering of broadcast rights that is forcing every major network to reconsider its footing.

The NFL is already using opt-out clauses in its deals with CBS, NBC, and Fox — operable after the 2029–30 season — to pursue renegotiations, emboldened by the large new rights agreements the NBA recently secured with ESPN and NBC. New deals covering the CBS/Fox/Amazon package (expiring 2033) and the ESPN package (expiring 2034) are already on the horizon.

A significant variable has emerged. The acquisition of CBS parent company Paramount by Skydance Media triggered a change-of-ownership clause in the NFL's deal with Paramount, giving the league the right to renegotiate a contract worth approximately $2.1 billion per year. The dynamic is complicated further by the NFL's own minority stake in Paramount, acquired as part of the ESPN/NFL Network transaction. Skydance CEO David Ellison has signaled his intent to preserve the NFL partnership, but the negotiating leverage sits firmly with the league.

The broader implication is structural: as streaming platforms outbid traditional broadcasters for live sports rights, the incumbent networks' grip on premium live content is loosening. The question is no longer whether streaming will claim a larger share of live sports. It is how quickly — and at what price.

Strategic Implications for the K-Content Industry

The structural shift now underway in global streaming — from subscriber expansion to revenue intensification per user — carries direct consequences for the Korean content ecosystem. Critically, as advertising's share of streaming value rises, products and media capable of carrying ad inventory (particularly FAST channels) are becoming more strategically significant. Ad-supported content requires programming that can persuade a broader, more diverse pool of advertisers. The diversity and range of K-content — spanning drama, variety, reality, documentary, and music — gives it an inherent advantage in that advertising marketplace.

Sources: Ampere Analysis, 'Global Streaming Revenue Report 2025' | Wall Street Journal (March 30, 2026) | Los Angeles Times (March 26 & 30, 2026) | Deloitte, 'Digital Media Trends 2026'