Fox's Red Seat Ventures completes three acquisitions in 14 months to launch an all-in-one monetization platform — setting up a direct confrontation with Spotify and Apple while exposing a structural gap in Korea's $3.8B creator media industry

SUMMARY | The podcast industry's competitive axis has shifted from content to infrastructure — whoever controls distribution, ad monetization, and subscriptions in a single stack wins the creator's revenue. Fox bought that stack.

The podcast industry's competitive dynamics have quietly shifted gears. The debate over monetization models — advertising versus subscriptions — was the first act. The second act is about who controls the infrastructure layer: the stack of distribution, ad tech, analytics, and subscription billing that sits between a creator's microphone and their revenue.

Jung Han

Jung Han

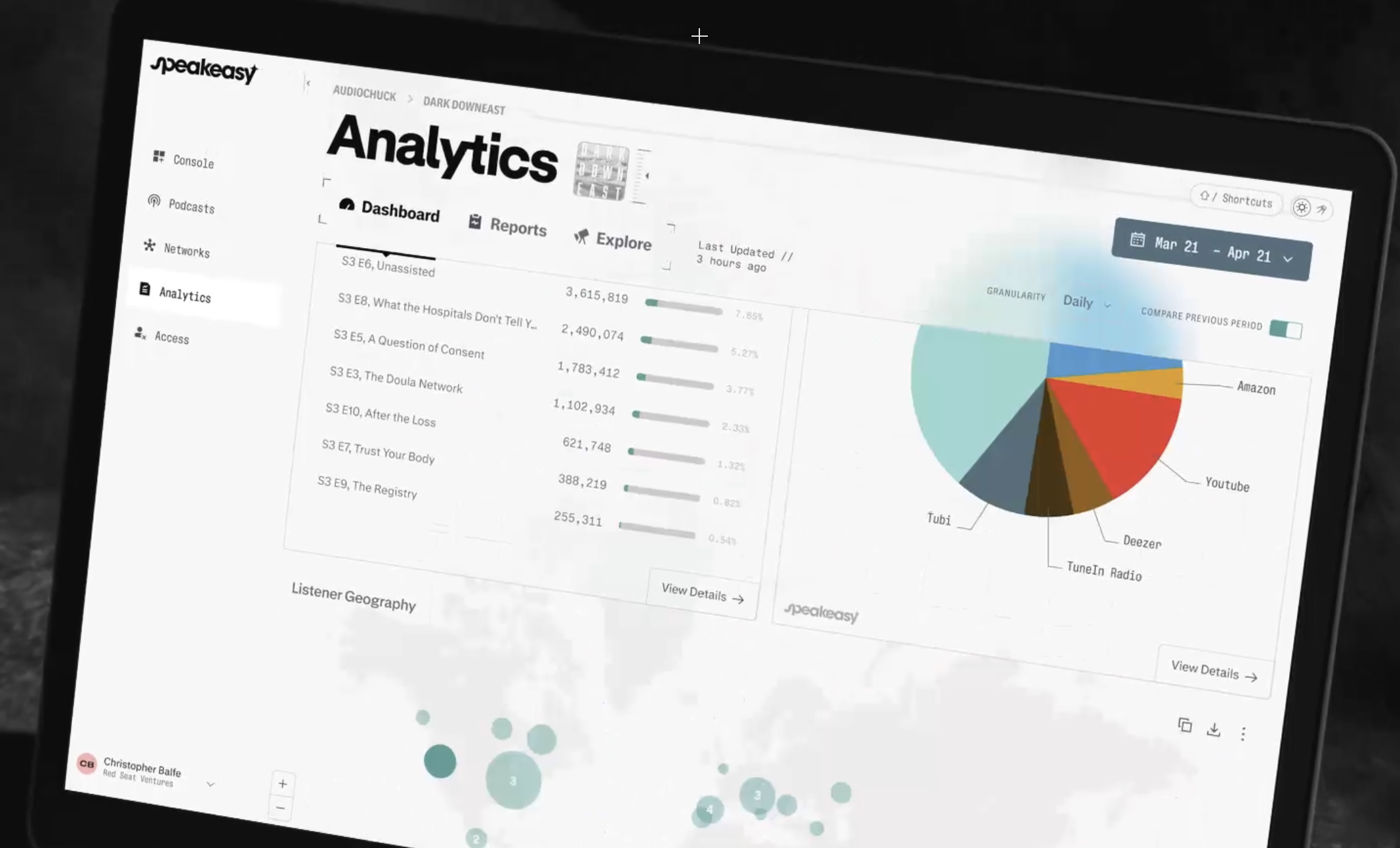

Fox Corporation's Speakeasy — an all-in-one podcast platform combining hosting, ad monetization, AI audience analytics, and paid subscription billing — is Fox's bid to own that stack. It is not a press release moment. It is the visible outcome of a 14-month, three-acquisition strategy that began in February 2025 and has been building toward a single thesis: the company that controls creator infrastructure will capture a disproportionate share of a market growing at 27% annually.

The global podcast market stands at $40.4 billion in 2026, projected to reach $131.1 billion by 2030 at a 27% CAGR. Some 584 million people listen to podcasts worldwide, and global creator economy ad spending hit $37 billion in 2025 — growing at four times the rate of the broader media industry. The money is there. The question is which platform collects the toll.

■ Market Snapshot (2026)

Sources: [1] Grand View Research / Research Nester [2] Edison Research / PodcastAtistics 2026 [3] Edison Research Infinite Dial 2025 [4] Nielsen [5] IAB/PwC [6] IAB Creator Economy Ad Spend 2025

Why Infrastructure — The Structural Problem Speakeasy Is Solving

The gap between podcast market growth and creator revenue is not a content problem. It is a structural one. According to Nielsen, only 12–15% of independent podcast creators generate meaningful income. Over 4.52 million podcasts are active, with 487,000 new shows launching every quarter — but advertising dollars remain concentrated at the top.

The underlying cause is fragmentation. To run a podcast business today, creators must separately contract with a hosting provider, an ad network, a subscription platform, an analytics tool, and a video distribution service — each with its own fees, data silos, and negotiating dynamics. One in three U.S. podcast listeners now consumes content on YouTube — meaning RSS-only audio distribution misses a growing share of the available audience entirely.

The IAB framed this precisely in its 2025 Creator Economy report. The ecosystem is 'highly fragmented,' with partnership structures, budget frameworks, and performance measurement varying widely across tools and platforms. 75% of brands plan to use AI in creator marketing within a year, but fragmented infrastructure limits what that AI can actually do. Integrated platforms that consolidate creator discovery, ad matching, and revenue management are, per IAB, the industry's most urgent structural need.

Speakeasy is Fox's answer to that need — built not from scratch, but assembled through acquisition.

The Acquisition Logic: Three Deals, One Stack

Fox acquired Red Seat Ventures in February 2025. At the time, RSV operated 17 creator-led programs generating over 200 million monthly views and ranked among the top 10 U.S. podcast networks by scale. The portfolio includes Tucker Carlson, Megyn Kelly, Bill O'Reilly, and Piers Morgan — established audiences across news, opinion, and true crime. What Fox acquired was not just the creators. It was the ad sales infrastructure and the verified audience sitting behind them.

Later that year, RSV acquired Backtracks, a podcast ad-tech company. Dynamic ad insertion, audience measurement, ad inventory management — the engineering layer under Speakeasy's monetization capabilities comes from here.

In February 2026, RSV acquired Supercast, a subscription platform serving podcasts including Huberman Lab and This American Life. Supercast's top 10 creators generate a combined $26 million in annual recurring revenue. The acquisition brought the subscription revenue layer in-house.

Map it out: Red Seat = creator network and audience. Backtracks = ad tech engine. Supercast = subscription revenue layer. Speakeasy is what happens when you bolt those three together. Bloomberg's framing of this consolidation — "podcast networks are starting to look like record labels" — captures the direction: vertical integration of distribution, ad sales, subscriptions, and talent management under one roof.

"Speakeasy is the platform we wished all our creators had access to, so we set out to build it. Creators are the new media, and they require an AI-enabled platform that meets the growing needs and opportunities of distributing and monetizing across audio, video and streaming platforms."— Chris Balfe, CEO, Red Seat Ventures

"From the very first conversation, it was clear that we shared the same worldview: that creators can own their audience, control their brand and build significant, sustainable media businesses on their own terms."— Jason Sew Hoy, Founder & CEO, Supercast

Fox vs. Spotify: Two Opposing Theories of Platform Growth

Spotify's podcast strategy — built around the 2019 acquisition of Anchor — was a land-grab. Free hosting, open access, millions of shows. The theory: own the distribution layer at scale, then monetize the audience through ads and subscriptions. It worked for volume. By 2023, Spotify hosted more podcast content than any competitor. But creator churn is high, monetization conversion is low, and the top creators have repeatedly threatened to leave unless economics improve.

Fox is running the opposite theory. Invitation-only access. Explicit targeting of 'top creators and enterprises' rather than the long tail. The bet is that a smaller number of high-value creators, connected to Fox's ad sales network and cross-platform distribution, generate better economics per creator than a mass-market free-hosting model.

The structural advantage Fox is claiming: its existing ad sales infrastructure means Speakeasy creators aren't just hosted — they're plugged into a direct line to large-scale advertisers. No independent hosting platform offers that. The structural risk: if Fox's ad network doesn't measurably lift creator revenue, the platform's core value proposition fails. Two metrics will determine the outcome: average revenue per creator on Speakeasy versus comparable platforms, and the rate at which top-tier creators opt in.

Korea's $3.8 Billion Creator Media Industry — and the Infrastructure Gap

South Korea's digital creator media industry generated KRW 5.31 trillion ($3.8 billion) in revenue in 2023 — a 28.9% year-on-year increase — according to the Ministry of Science and ICT's official industry survey published in December 2024. The sector employs 42,378 people across 13,514 companies. The number of solo media creators filing income tax returns jumped from 4,875 in 2019 to 33,065 in 2020 — nearly sevenfold in a single year — generating a combined annual income of KRW 452.1 billion.

Growth is not the issue. Infrastructure is. Korean creators' primary monetization routes remain YouTube ad revenue sharing, TikTok rewards, and brand sponsorships. An integrated platform supporting podcast and audio-format ad monetization alongside subscription billing — the structure Speakeasy provides — does not exist domestically at scale. Naver Audio Clip and Podbbang operate in the space, but neither connects global distribution with large-scale advertising.

External platform capital is filling the gap on its own terms. TikTok Korea announced a KRW 75 billion ($54M) investment in the Korean market in 2026, with creator rewards for Korean-language content expanding to up to 2× standard rates. Fan commerce platform Panding recorded KRW 65 billion in GMV in 2025 — more than doubling year-on-year for the fourth consecutive year — with the platform's top 100 creators averaging KRW 1 billion in revenue each. Korean creators have the fandom. They do not have the infrastructure layer that converts fandom into diversified, platform-independent revenue.

Asia-Pacific is the fastest-growing podcast region globally. K-content's global reach — Korean-language podcasts, drama-adjacent audio, K-pop creator communities — represents an audience that exists but is systematically under-monetized in audio formats. The infrastructure to capture that revenue simply isn't there.

■ Korea Creator Media Industry Snapshot

Sources: [12] Ministry of Science and ICT, Digital Creator Media Industry Survey 2024 (Dec 2024) [13] RAPA 2021 Solo Media Industry Survey [14] ZDNet Korea / K-Impact Summit 2026 [15] VentureSquare, Jan 2026

The Structural Question for Korean Creator Media

Fox's thesis with Speakeasy is testable and specific: a company that owns both a content consumption platform (Tubi, 74 million MAU) and a creator monetization infrastructure (Speakeasy) has structural advantages in ad matching and subscription conversion that standalone platforms cannot replicate. Whether that thesis holds will be visible in creator revenue metrics within 18 months.

What is not in question is the direction of the broader industry shift. IAB data confirms that creator economy ad spend is growing at four times the rate of total media. The platform that sits between that ad spend and the creator captures a toll on every dollar. Speakeasy is Fox's bid for that position.

For Korea, the implications operate on two levels. The practical level: Korean creators can evaluate whether Speakeasy's infrastructure opens a viable monetization path in global audio markets where they currently have audience but limited revenue capture. The strategic level: Korea's creator media sector — KRW 5.31 trillion and growing at 28.9% — is building on top of distribution platforms owned by others. The fandom is Korean. The infrastructure collecting the toll is not.

The question Speakeasy's launch puts to the Korean creator economy is not whether to pay attention to what Fox built. It is whether something equivalent gets built here.

▶ References

[1] Grand View Research, "Global Podcasting Market Report, 2024–2030"; Research Nester, Podcasting Market Forecast 2026–2035

[2] PodcastAtistics.com, "33 Podcast Statistics 2026", Jan 2026; Edison Research (4.52M+ podcasts, 584M listeners, 487,000 new/quarter)

[3] Edison Research, "The Infinite Dial 2025" (U.S. monthly 55%, weekly 40% — all-time high)

[4] Nielsen, "Podcast Consumer Report 2023"; BusinessResearchInsights, Podcasting Market Report 2024

[5] IAB/PwC, U.S. Podcast Advertising Revenue Study; loopexdigital.com Q1 2026 ($2.56B, +10.5%)

[6] IAB, "2025 Creator Economy Ad Spend Report" (MADTimes, Nov 2025) — $37B, 4× broader media growth rate; 48% 'must buy'; 75% AI adoption

[7] Fox Corporation PR, "Fox Corporation Acquires Red Seat Ventures", Feb 10, 2025; Variety, Apr 2, 2026

[8] Fox Corporation PR, "Red Seat Ventures Acquires Supercast", Feb 10, 2026

[9] Yahoo Finance, "Fox Corp.'s Red Seat Ventures Acquires Supercast", Feb 24, 2026 (top 10 creators ARR $26M)

[10] Bloomberg Soundbite Newsletter, "Red Seat launches podcast hosting service Speakeasy", Apr 2, 2026

[11] Research Nester, Creator Economy Market 2026 — only 1–5% of creators earn meaningful revenue

[12] Ministry of Science and ICT (MSIT), "2024 Digital Creator Media Industry Survey", Dec 2024 (FY2023: KRW 5.31T, +28.9% YoY)

[13] Korea Radio Promotion Association (RAPA), "2021 Solo Media Industry Survey" (2019: 4,875 filers → 2020: 33,065 filers; total income KRW 452.1B)

[14] ZDNet Korea, "TikTok Korea KRW 75B investment, creator rewards expansion" / K-Impact Summit 2026, Apr 2, 2026

[15] VentureSquare, "Panding records KRW 65B GMV in 2025", Jan 19, 2026

K-EnterTech Hub | April 2, 2026