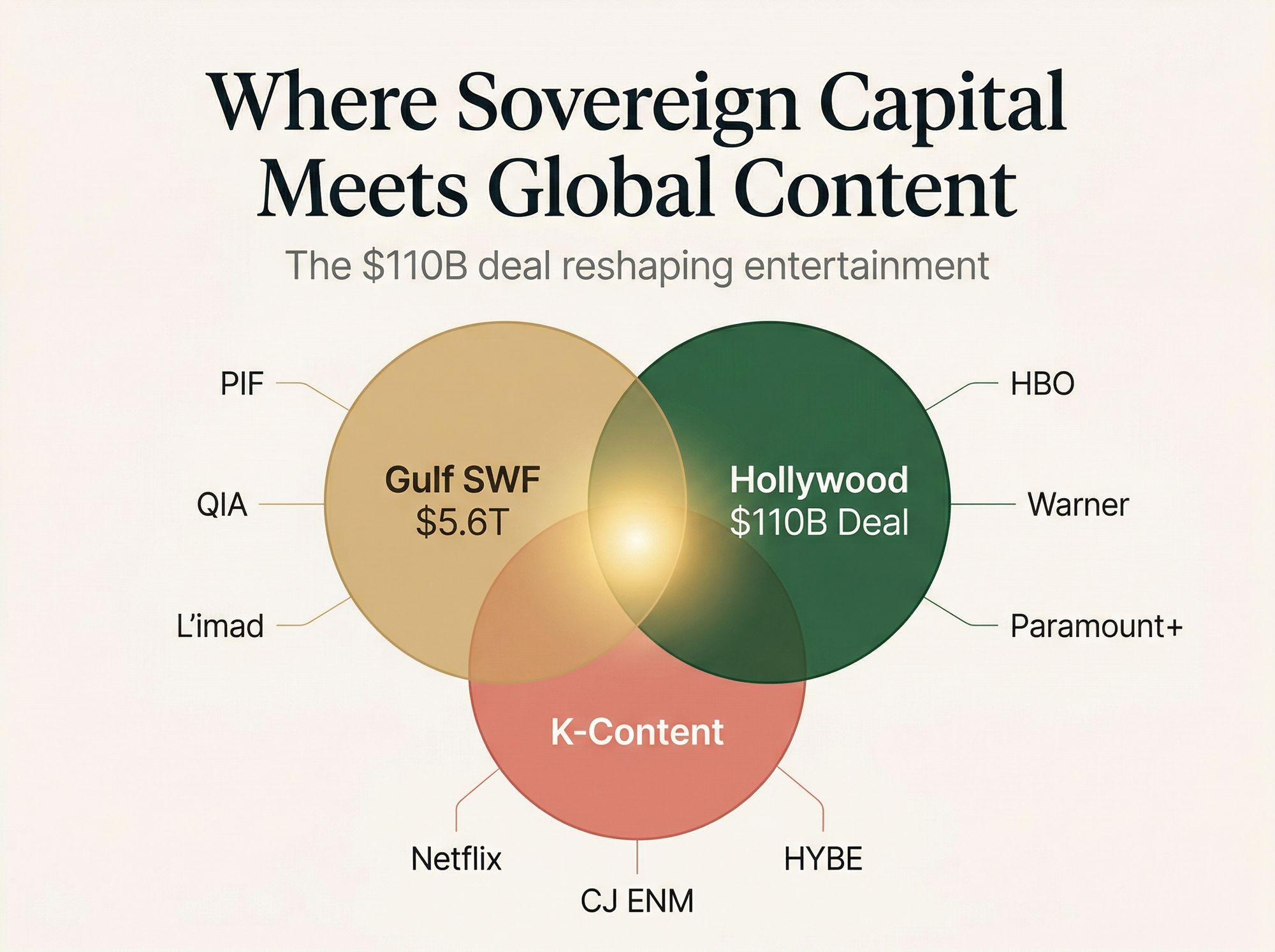

Sovereign Wealth Funds (SWF), the Paramount–WBD Merger, Gulf Capital in Hollywood, and What It All Means for Korean Content

Saudi PIF · Qatar QIA · Abu Dhabi L'imad signed $24B in equity commitments on April 6, 2026 — $110B total, the largest media merger in Hollywood history; K-content faces a fundamentally restructured global landscape

The global media industry has been fundamentally reordered. As Paramount Skydance moves to acquire Warner Bros. Discovery (WBD) with the backing of three Gulf sovereign wealth funds (SWFs) — Saudi Arabia's Public Investment Fund (PIF), Qatar Investment Authority (QIA), and Abu Dhabi's L'imad Holding Co. — totaling nearly $24 billion in signed equity commitments, the largest media merger in Hollywood history is entering its final stretch.

Jung Han

Jung Han

Combined with $54 billion in debt financing, the total deal value reaches $110 billion. Once closed, HBO, CNN, Warner Bros., Paramount+, Harry Potter IP, MTV, and Showtime will sit under one roof — with the national treasuries of the Gulf underwriting the deal. The tremors of this transaction reach all the way to Seoul.

Before the Iran conflict erupted, the Middle East had become the single most reliable backstop for Wall Street mega-deals. Gulf SWFs pumped billions into OpenAI's funding rounds, the $28.8 billion Electronic Arts buyout, and now WBD — all fueled by the global AI boom and sovereign mandates to deploy decades of accumulated oil wealth before the fossil fuel era ends (WSJ, April 3, 2026).

Their shared strategic objective: transform hydrocarbon-dependent national economies into diversified engines of technology, entertainment, and soft power. Hollywood was the most coveted prize in that strategy, and these funds have now claimed a major stake in it.

■ Deal at a Glance (April 6, 2026)

The Deal: Competitive Backdrop, Capital Stack, and Regulatory Architecture

Paramount Skydance CEO David Ellison — son of Oracle co-founder and billionaire Larry Ellison — launched a hostile bid for WBD after the company had opted to enter sale negotiations with Netflix. After months of competitive escalation, Paramount sweetened its offer and prevailed, securing HBO, CNN, the Harry Potter franchise, and the Warner Bros. studio lot.

The final capital structure is: $24 billion in Gulf SWF non-voting equity (PIF ~$10B; QIA and L'imad ~$14B combined) + $54 billion in debt (Bank of America, Citigroup, and Apollo Global Management, currently being syndicated) + direct equity from RedBird Capital Partners and the Ellison family, who formally backstop any equity shortfall.

Chinese tech conglomerate Tencent exited the deal amid concerns its involvement would trigger a mandatory CFIUS national security review; Affinity Partners (the private equity firm of Jared Kushner, President Trump's son-in-law) withdrew separately.

The regulatory architecture reflects careful legal engineering. Under the U.S. Communications Act, foreign entities may not hold more than 25% equity or voting interest in a U.S. broadcast licensee without FCC approval.

Paramount's three-pillar defense: (1) each Gulf fund holds far less than 25% of the combined entity; (2) all three investors hold only non-voting equity, formally documented in SEC filings as foregoing 'any governance rights, including board representation'; and (3) the transaction involves no transfer of broadcast station licenses, limiting FCC jurisdiction — a position confirmed publicly by FCC Chairman Brendan Carr.

Seven Democratic senators sent an open letter demanding a 'full and independent review,' and DOJ acting antitrust chief Omeed Assefi stated the deal will 'absolutely not' receive political fast-tracking. CFIUS mandatory review is not expected. The legal structure is sound; political noise is real but structurally contained. The remaining gates are the April 23, 2026 WBD special shareholder vote and European Commission regulatory clearance.

With the regulatory picture largely settled structurally, the market's attention now turns to the nature of the capital itself — what kind of money is backing this deal, and what it signals for the future of global media. To understand the strategic implications of the Paramount-WBD transaction, one must first understand the sovereign wealth funds that are making it possible.

Source: WSJ, Global SWF | 2025-2026 ※ Wall Street Journal original reporting

IThe Capital Behind the Deal: What Is a Sovereign Wealth Fund (SWF)?

A sovereign wealth fund (SWF) is a state-owned investment vehicle that manages a nation's surplus wealth — typically accumulated through commodity exports (most commonly oil and gas), current account surpluses, or fiscal reserves. The key distinction from private asset managers or pension funds is ownership: the state is the sole proprietor. SWFs have no private shareholders, no quarterly earnings calls, and — in most cases — no legal obligation to disclose their holdings publicly. This opacity is both their structural advantage and the enduring source of Western governments' concern about their strategic intentions.

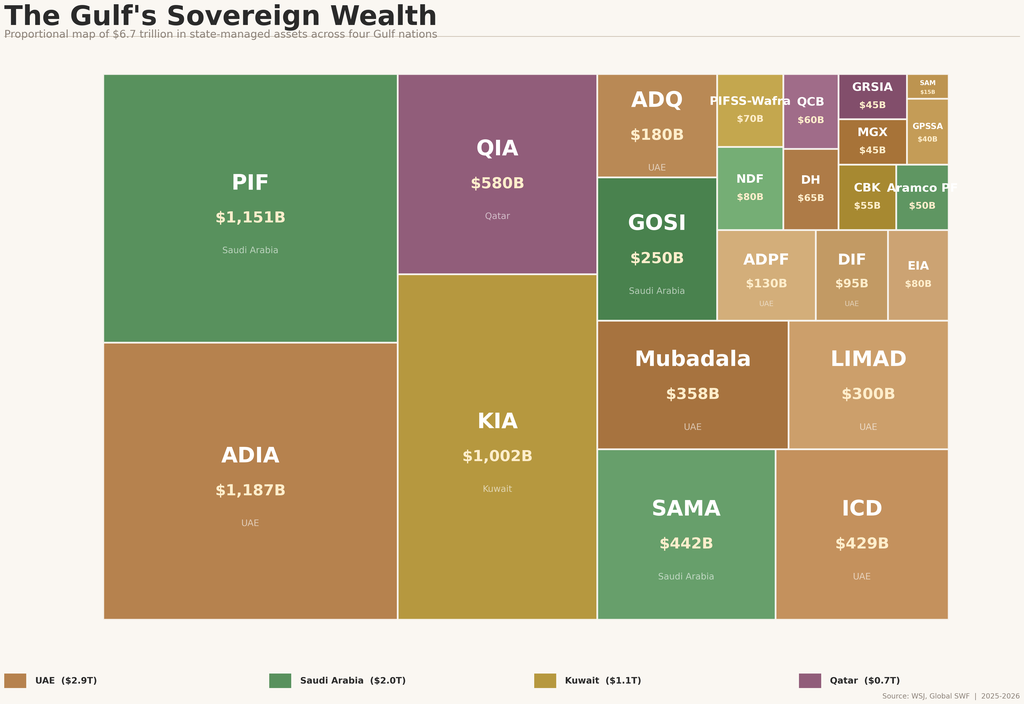

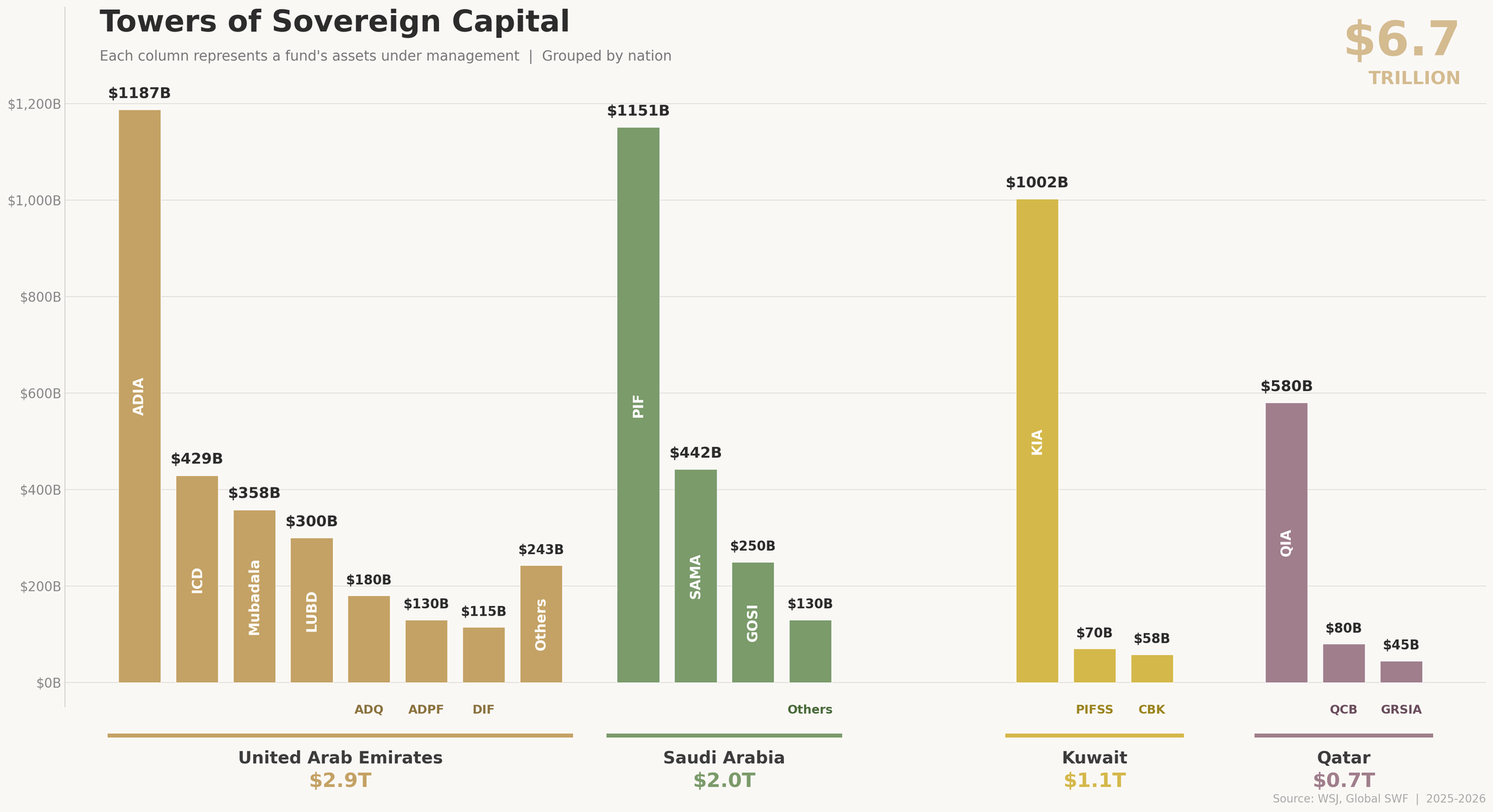

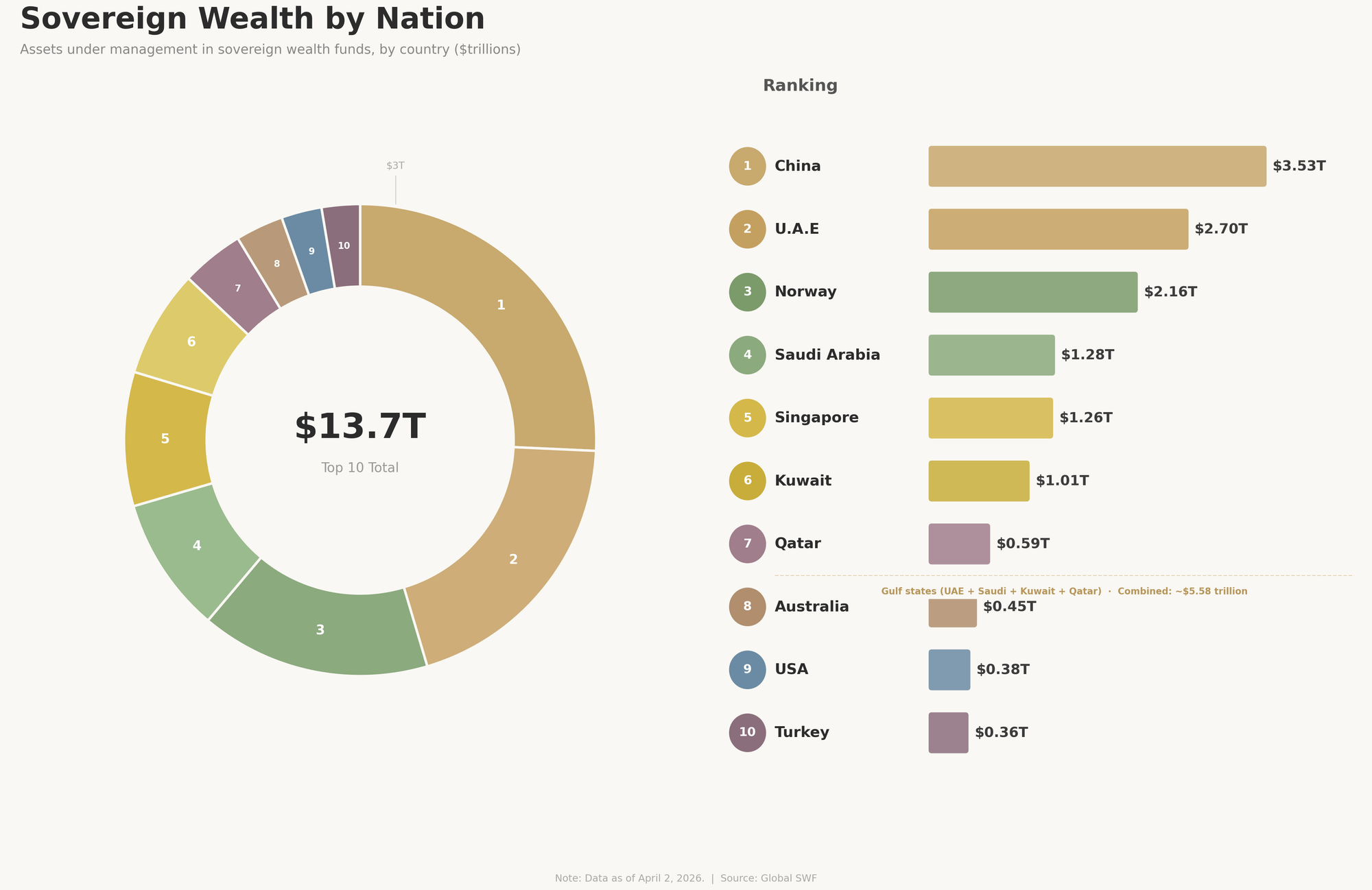

The concept was first institutionalized in 1953, when Kuwait established the Kuwait Investment Authority (KIA) to manage growing petroleum revenues for future generations — making it the world's first sovereign wealth fund. Norway followed with the Government Pension Fund Global (GPFG) in 1990, funded by North Sea oil revenues. Singapore built two distinct vehicles: GIC (est. 1981, managing foreign reserves) and Temasek (1974, managing state-owned enterprise stakes). Abu Dhabi established ADIA in 1976. Qatar's QIA was created in 2005. As of April 2, 2026, the top 10 SWF nations hold a combined $13.7 trillion in assets under management (Global SWF). Of that total, the four Gulf states — UAE ($2.70T), Saudi Arabia ($1.28T), Kuwait ($1.01T), and Qatar ($0.59T) — account for approximately $5.58 trillion, or roughly 41% of the global top-10 total.

Three characteristics fundamentally distinguish SWFs from all other institutional investors. First: permanent capital. Private equity firms must return capital to investors after a defined fund life (typically 7–10 years), forcing asset liquidation on a timeline. SWFs hold capital indefinitely on behalf of the state — long-term value preservation and intergenerational wealth transfer take precedence over short-term return maximization. Second: dual mandate.

Most SWFs pursue both financial returns and national strategic objectives simultaneously. Norway's GPFG is the notable exception — it operates as a pure financial investor with no domestic exposure and strict ethical exclusion screens. Gulf SWFs, by contrast, are explicitly 'strategic-type' funds: their investment decisions serve national economic diversification, job creation, technology transfer, and soft power amplification alongside return targets.

Third: opacity and political connectivity. Decision-making processes within Gulf SWFs are rarely transparent. Personnel overlap between fund leadership and national political leadership is the norm, not the exception — PIF governor Yasir Al-Rumayyan simultaneously chairs Saudi Aramco's board as a close MBS ally; Sheikh Tahnoon bin Zayed chairs ADIA while serving as UAE national security adviser.

This structural connectivity is precisely what Western regulators scrutinize under foreign investment review frameworks like CFIUS — and why Paramount's non-voting equity structure for the Gulf funds is such a deliberate piece of legal engineering.

The Santiago Principles (formally, the Generally Accepted Principles and Practices for Sovereign Wealth Funds) represent the international community's attempt to impose governance standards without binding regulatory authority.

Developed in 2008 under IMF facilitation — after Gulf SWFs drew criticism for acquiring large stakes in distressed Western financial institutions during the global financial crisis — the Principles call for transparency, sound governance, and a commitment to purely commercial investment objectives. ADIA, QIA, Mubadala, and PIF have all formally endorsed them.

However, as voluntary self-regulatory standards, their practical enforcement power is limited. The non-voting equity structure Paramount negotiated — explicitly foregoing any governance rights including board representation — is precisely the structural safeguard designed to address Santiago Principles concerns and pre-empt regulatory challenges from CFIUS and the FCC.

Investment strategy among Gulf SWFs has evolved across three distinct generational waves. The first generation (ADIA, KIA, est. 1970s) followed a conservative, passive, globally diversified portfolio approach — equities and fixed income across major markets, minimal domestic exposure, deliberately low public profile.

Wealth preservation for future generations was the primary mandate. The second generation (QIA, Mubadala, emerging 2000s–2010s) began making direct investments in trophy assets and strategic sectors, introducing the concept of 'influence investment' — acquiring assets that confer prestige, market access, or geopolitical leverage alongside financial returns.

The third and current generation (PIF under Vision 2030, L'imad, UAE's MGX) functions explicitly as an active development finance institution: deploying capital to reshape national industrial structure, attract foreign technology and talent, and accelerate post-hydrocarbon economic transformation.

This is why PIF's single largest investment category remains domestic Saudi Arabia — NEOM, Red Sea Global resorts, Riyadh Air — while its international investments increasingly target strategic partnerships over passive stakes. The Paramount-WBD deal represents this third generation's formal arrival in the global entertainment and media ecosystem.

Gulf SWFs in Hollywood: Soft Power as Investment Thesis

Gulf SWF investment in entertainment and sports is not primarily a financial calculation — it is soft power strategy executed through capital allocation. The pattern is most visible in Saudi Arabia. Following severe international reputational damage from the murder of journalist Jamal Khashoggi and sustained human rights criticism, Saudi Arabia under MBS has systematically pursued what critics term 'sportswashing' — deploying sports and entertainment investment as instruments of national image rehabilitation.

The creation of LIV Golf (a direct challenge to the PGA Tour's century-old dominance), the acquisition of Newcastle United FC in England's Premier League, boxing and UFC event hosting, Formula 1 race deals, the Riyadh Season mega-entertainment festival series, and now the ~$28.8 billion EA buyout — all executed through PIF as a unified national brand repositioning platform.

Qatar's model is more established and arguably more strategically coherent. The 2022 FIFA World Cup was Qatar's proof of concept: a nation of three million people successfully hosting the world's most-watched sporting event and projecting itself onto the global stage as a credible international actor. QIA's ownership of Paris Saint-Germain (PSG) is not merely a football investment — it is Qatar's membership card in Europe's elite cultural, fashion, and entertainment ecosystem.

Owning The Shard, Canary Wharf, and Harrods physically inscribes Qatar's presence in London, the world's financial and cultural capital. The UAE has built the most multidimensional soft power strategy of the three: Louvre Abu Dhabi (art and culture), NYU Abu Dhabi (education and research), Formula 1 Abu Dhabi Grand Prix (sports and luxury tourism), and now MGX's AI investment drive under Sheikh Tahnoon (technology leadership). Tahnoon's vision — transforming Abu Dhabi from an oil emirate into 'the AI capital of the Middle East' — is the Gulf soft power thesis for the 2030s.

In this analytical frame, the Gulf SWFs' participation in the Paramount-WBD deal is not a departure from their soft power playbook — it is its logical culmination. HBO's global premium drama brand, CNN's international news reach, Warner Bros.' century of film and television IP, and Paramount's franchise depth collectively constitute the single largest concentration of globally resonant cultural assets ever assembled in one transaction.

PIF had historically been reluctant to invest in Hollywood studios, citing streaming competition risks. That hesitation has now given way to conviction. The EA buyout (~$28.8B) made PIF one of the world's largest digital entertainment investors; the Paramount-WBD commitment makes it a cornerstone financier of the new Hollywood media architecture.

■ Gulf SWF Overview (Global SWF / WSJ, April 2, 2026)

Key Funds Decoded: People, Assets, and Strategy

Saudi Arabia's Public Investment Fund (PIF, est. 1971, $1.151 trillion, world #4) was transformed by Crown Prince Mohammed bin Salman from a low-profile domestic vehicle into a global investment juggernaut under Vision 2030. Governor Yasir Al-Rumayyan is simultaneously Aramco's board chairman and one of the Crown Prince's closest allies — frequently photographed alongside Donald Trump on golf courses. PIF deployed $36.2 billion in 2025 (+81% year-on-year), making it the world's most active SWF by investment volume.

Key international assets: LIV Golf, Selfridges (40% stake), London Heathrow Airport (15% stake), Uber, EA (~$28.8B buyout), and new national airline Riyadh Air. Including SAMA ($442B, Saudi Central Bank foreign reserves) and GOSI ($250B, Social Insurance), Saudi Arabia's total sovereign asset base approaches $2 trillion.

The UAE ($2.70 trillion, world #2) is the Gulf's dominant SWF power, concentrated in Abu Dhabi. The key figure across this entire capital complex is Sheikh Tahnoon bin Zayed Al Nahyan — UAE president's brother, Abu Dhabi deputy ruler, national security adviser, ADIA chairman, and MGX (AI investment fund) head. An avid MMA practitioner, his funds purchased 49% of the Trump family's cryptocurrency venture for $500 million in January 2025, days before the inauguration — emblematic of the deepened U.S.-Gulf political alignment.

ADIA (est. 1976, $1.187T) is the world's most sophisticated passive global diversifier, holding Deutsche Bank Center, Marriott Edition Hotels across New York/Miami/London, and the U.S. Häagen-Dazs manufacturer. Mubadala ($358B) was 2024's most active SWF by deal count globally (300+ transactions in five years), with major recent acquisitions including Germany's Techem ($7.84B) and Apleona ($4.18B). L'imad ($300B), which emerged as a significant force in late 2025, controls ADQ (whose assets include Etihad Airways) and is the Abu Dhabi vehicle designated for the Paramount-WBD deal, overseen by the Crown Prince.

Qatar Investment Authority (QIA, est. 2005, $580B, world #7) is the preeminent 'trophy asset' sovereign investor globally: The Shard, Canary Wharf, Harrods, the Empire State Building's landlord, PSG, and major stakes in Volkswagen. Governor Sheikh Bandar bin Mohammed Al-Thani doubles as Qatar Central Bank governor.

QIA is executing a rapid strategic pivot from real estate to 'new economy' assets — $13 billion into Anthropic and a $25 billion Goldman Sachs technology partnership in 2025 signal the direction of travel. Kuwait Investment Authority (KIA, est. 1953, $1.002T, world #6) is the world's oldest SWF, crossing the trillion-dollar threshold in 2025. Core holdings include Mercedes-Benz, BP, and BlackRock. Chair Abdulaziz AlMarzooq is expanding into AI data center funds alongside Brookfield, departing from KIA's traditionally conservative blue-chip investment posture.

Geopolitical Context: Capital Committed Amid Regional Conflict

These equity commitments arrived against one of the most volatile regional security backdrops in decades. The U.S.-Israeli war on Iran has struck Gulf airports, energy infrastructure, and financial districts — including drone strikes on the Ras Tanura refinery complex, Saudi Arabia's largest petroleum export terminal.

In March 2026, Reuters reported that Saudi Arabia, Qatar, and the UAE were reviewing their SWF portfolios in anticipation of offsetting economic shocks from the conflict, weighing potential divestments and a re-evaluation of global sponsorship commitments.

That three sovereign funds nonetheless signed a $24 billion U.S. entertainment deal in this context reflects three simultaneous forces: the structural durability of long-horizon SWF investment mandates in the face of short-term geopolitical turbulence; the perceived resilience of U.S. entertainment assets as stores of durable strategic and financial value; and the deepened political-economic alignment between Gulf capitals and the Trump administration, under which Gulf states have pledged trillions in future U.S. investments.

Sheikh Tahnoon's $500 million purchase of 49% of the Trump family's crypto venture, completed days before the inauguration in January 2025, is the clearest recent illustration of this alignment.

What This Means for the Korean Content Industry

The Paramount-WBD merger and the Gulf SWFs' entry into Hollywood entertainment create two simultaneous axes of structural change for the Korean content industry: a platform consolidation axis and a capital reallocation axis — and both carry threats and opportunities in equal measure. On the platform side, the merger absorbs HBO Max and Paramount+ into a single integrated entity, collapsing the separate negotiating structures that Korean studios like CJ ENM, Studio Dragon, and NEW currently use to maximize leverage across multiple buyers. Post-merger, they will face a single counterparty commanding HBO's premium drama brand, Warner Bros.' global distribution infrastructure, and Paramount+'s subscriber base simultaneously — a far more powerful gatekeeper than any they have previously negotiated with.

Yet the very actor that lost the WBD bid — Netflix — becomes a paradoxical structural beneficiary for the Korean content industry. Facing a newly formidable HBO-anchored competitor, Netflix has every strategic incentive to dramatically accelerate its K-content original investment. 'Squid Game' remains Netflix's most-watched series in history; the Netflix-Sony animated co-production 'K-Pop Demon Hunters' and a consistent pipeline of global K-drama hits have further established Korean content as one of the platform's most reliable audience-acquisition assets. When a new media giant housing HBO enters the field, Netflix's most immediate counterweapon is more investment in the content that Netflix alone controls — and Korean originals sit at the top of that list. The paradox is sharp: the stronger the new Paramount-WBD entity becomes, the more aggressively Netflix will compete for Korean IP.

From the sovereign capital perspective, the shift is even more direct. Saudi Arabia's PIF co-invested with Singapore's GIC in Kakao Entertainment for approximately $966 million — establishing a clear precedent that Gulf sovereign capital has already identified Korean IP platforms as strategic assets, not merely financial bets.

The same capital that is now underwriting HBO, CNN, and Warner Bros. has already taken a position in a Korean content holding company. BTS's stadium concert at Riyadh's King Fahd International Stadium and BLACKPINK's Abu Dhabi performance sold out at scale, demonstrating that K-pop commands genuine mass-market reach across Gulf audiences — not niche fandom. Korean dramas consistently rank among the top-consumed content categories on Saudi, UAE, and Qatari OTT platforms. This cultural penetration creates the conditions for Gulf SWFs to make direct investment approaches — equity stakes, co-production frameworks, licensing deals — to HYBE, CJ ENM, Studio Dragon, and similar companies. The Riyadh Season entertainment events, Expo 2030, and the NEOM project all represent large-scale programming and content platforms where Korean entertainment IP would be a natural and commercially valuable fit. This is not a speculative future scenario; it is the logical extension of investments already underway.

On the FAST (Free Ad-Supported Streaming TV) front, the combined Paramount-WBD content library will intensify competition across major CTV platforms — Samsung TV Plus, LG Channels, Roku, Pluto TV — as the new entity pursues secondary revenue maximization through its enormous archive. The immediate effect is grid oversupply: hundreds of new channels competing for advertising budgets and viewer attention across platforms that are already near saturation.

However, this creates a structural opening for Korean content. Platforms seeking differentiation from a library dominated by Hollywood output will have stronger incentive to feature cost-competitive, high-engagement international content in dedicated channels — precisely the lane where K-dramas, K-variety, and K-film already have proven global audience traction. The licensing economics of Korean content relative to comparable Hollywood premium content remain a structural advantage. K-content's genre and format diversity — romance, thriller, fantasy, historical drama, variety entertainment — maps well against the platform demand for content that serves distinct audience segments without cannibalizing each other.

The strategic imperative for the Korean content industry is clear: this is not a moment for passive observation. The consolidation of global platform power, the realignment of streaming competitive dynamics, and the acceleration of Gulf SWF entertainment investment all point in the same direction — toward a restructured global market where scale partnerships and proactive capital relationships will determine which content industries thrive.

Korean producers, distributors, platforms, and government bodies — KOCCA, the Ministry of Culture, and Korea Eximbank — need to move in coordinated fashion: consolidating negotiating leverage for the new Paramount-WBD relationship, building proactive channels toward Gulf SWF co-investment and co-production, and preparing K-content FAST packages specifically engineered for the new CTV grid environment. The window is open. The question is whether the industry acts with the strategic urgency the moment demands.

Sources

[1] WSJ — Deal Coverage https://www.wsj.com/business/deals/three-gulf-funds-agree-to-back-paramounts-81-billion-takeover-of-warner-04eda364 — Jessica Toonkel, Lauren Thomas | WSJ, April 6, 2026

[2] Deadline https://deadline.com/2026/04/paramount-wbd-merger-foreign-backing-gulf-funds-deal-1236780058/ — Natalie Oganesyan, Jill Goldsmith | Deadline, April 6, 2026

[3] WSJ — Gulf SWF Guide (Chart source) https://www.wsj.com/finance/a-guide-to-the-gulfs-trillions-of-dollars-of-sovereign-wealth-c17b505e — Natasha Dangoor, Eliot Brown, Drew An-Pham | WSJ, April 3, 2026

[4] Variety https://variety.com/2026/tv/news/paramount-skydance-funding-saudi-arabia-qatar-abu-dhabi-funds-warner-bros-deal-1236709251/ — Variety, April 6, 2026

[5] Global SWF / Gulf News https://gulfnews.com/world/gulf/saudi/saudi-arabias-public-investment-fund-named-worlds-most-active-swf-in-2025-1.500399307 — PIF 2025 Activity Data, January 2026

[6] Reuters https://money.usnews.com/investing/news/articles/2026-03-11/some-gulf-states-reviewing-sovereign-investments-to-offset-economic-shock-of-iran-war-official-says — Gulf SWFs Review Portfolios Amid Iran War, March 11, 2026