K-FAST 2.0 전략 분석: 자막의 덫에 빠진 K-콘텐츠,미국 거실을 점령하려면 더빙이 답이다

by

2026년 3월 1일

INDUSTRY ANALYSIS | K-Content · FAST · Global OTT Strategy | February 27, 2026

K-FAST 2.0 Strategic Deep Dive Escaping the Subtitle Trap:How K-Content Can Conquer the American Living Room

A 60% channel closure rate, $4 CPMs, and invisible algorithmic walls — this is the autopsy of K-FAST's first era. The prescription for survival: AI dubbing, vertical hero channels, and a YouTube-FAST flywheel that turns fandom into premium revenue.

Source: K-EnterTech Hub Webinar / FASTMaster Intelligence (February 2026) | Published: February 27, 2026

Presenter: Gavin Bridge — Founder, FASTMaster Intelligence; Former Head of FAST Channels, Amazon MGM Studios

■ Source Webinar

※ Screenshot recreated from webinar footage at t=4345s (1:12:25) — K-FAST 2.0 Playbook chapter opening

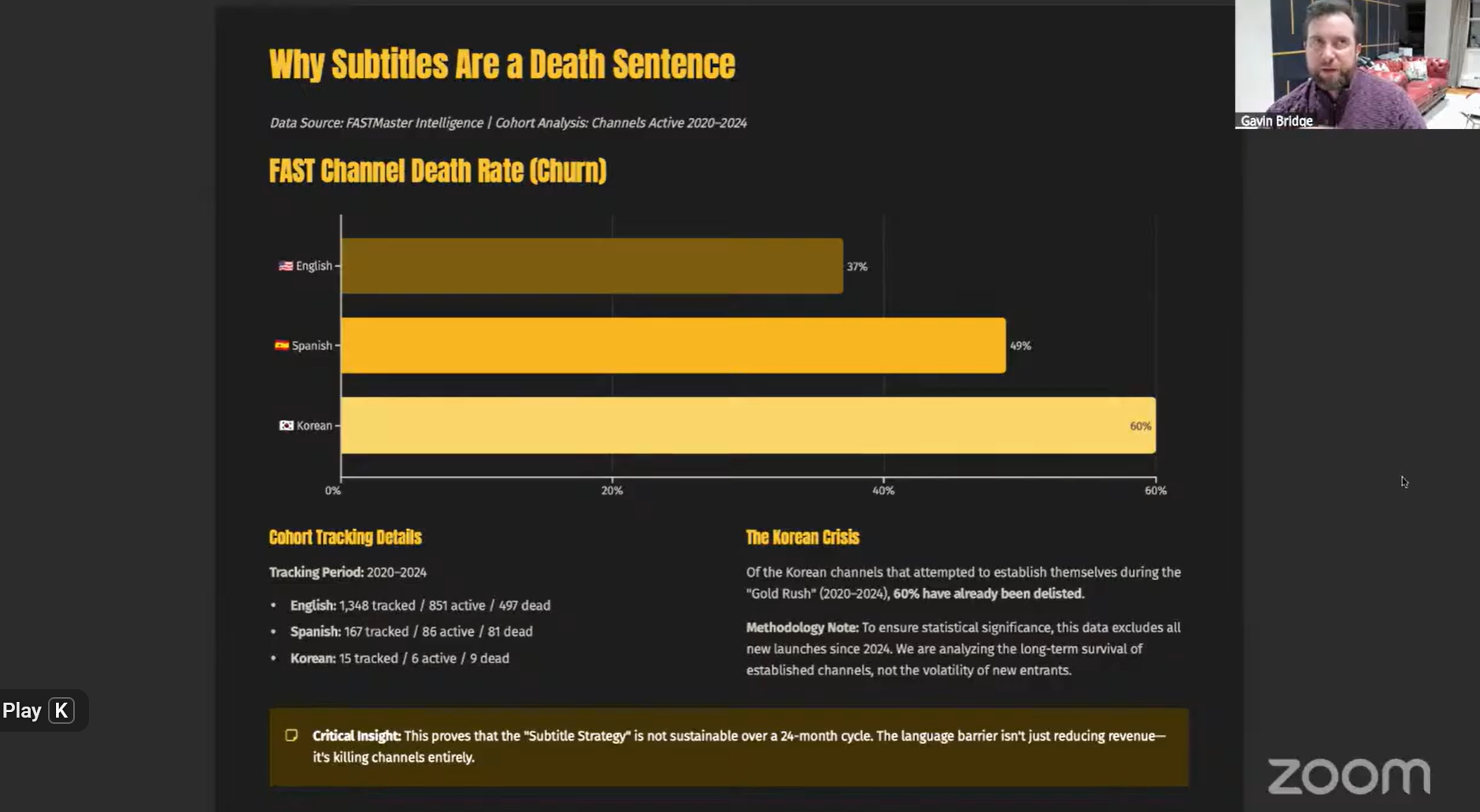

There is an uncomfortable number circulating in the K-content industry right now. Of the 15 Korean-language channels that entered the U.S. FAST (Free Ad-Supported Streaming TV) market between 2020 and 2024, nine — fully 60% — have already been removed from platforms. That is 1.6 times the closure rate of English-language channels (37%) and eleven percentage points higher than Spanish-language channels (49%). In the world's largest Hallyu consumption market, why does K-content fail so consistently on FAST? The answer is not the quality of the content. The answer is the structure of the distribution.

Ad-tech algorithms automatically filter out content tagged with Korean audio from premium ad inventory. The viewer's brain, reclining on a sofa in front of a living room TV, registers reading subtitles as work. The result: CPMs trapped at $4–8, viewing hours that never compound, and channels that become targets for platform purges.

Jung Han

Jung HanGavin Bridge — founder of FASTMaster Intelligence and former Head of FAST Channels at Amazon MGM Studios, arguably the most data-informed analyst working in the global FAST space — delivered the diagnosis and the prescription at K-EnterTech Hub's February 2026 webinar. His solution is a three-part flywheel: break the audio barrier with AI dubbing, concentrate investment on the top 5% of hero IP through vertical channels, and use YouTube as a community laboratory before graduating content to FAST for premium revenue harvest. The era of K-FAST 2.0 has begun.

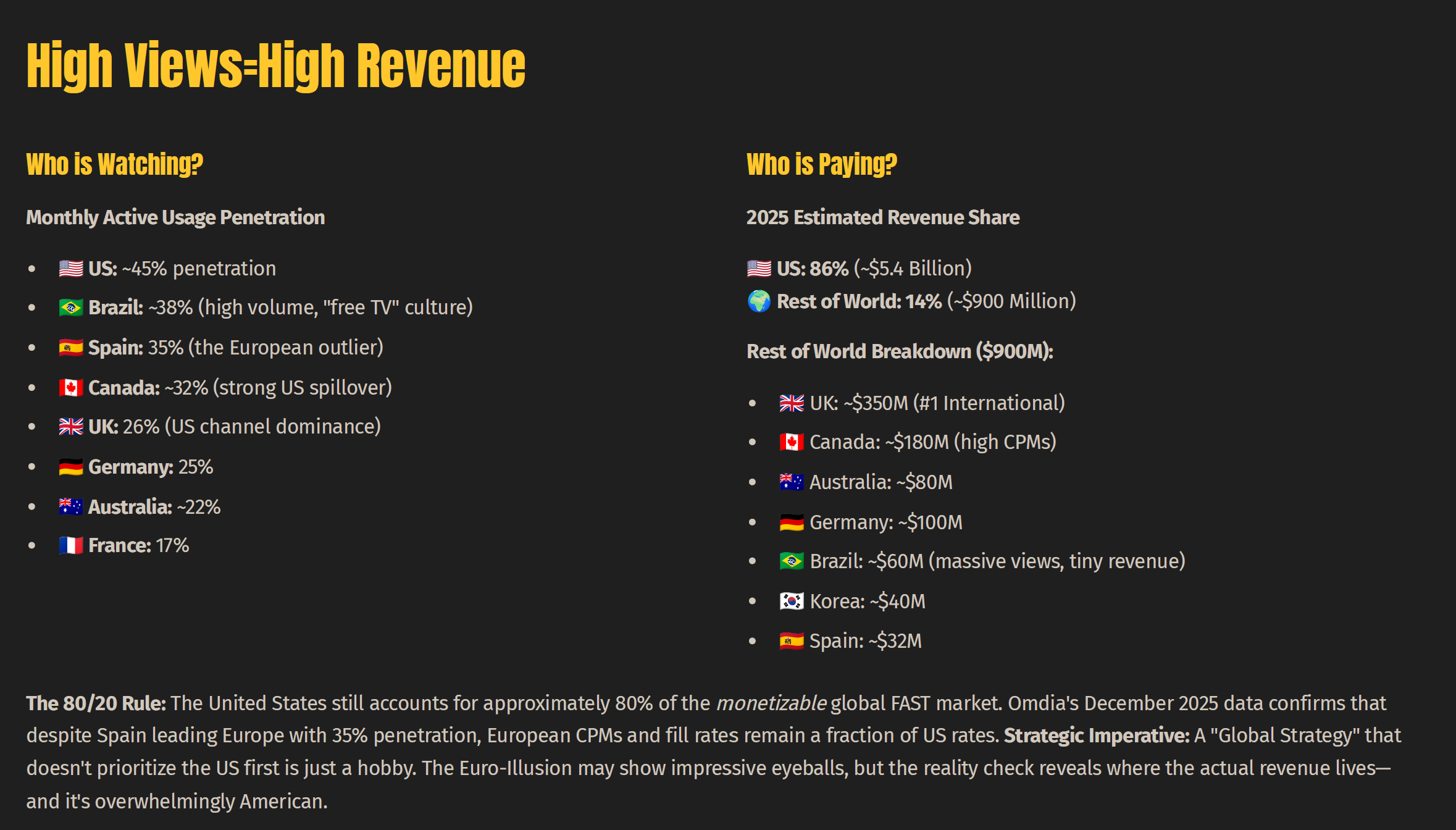

The FAST gold rush of the early 2020s was powered by a simple structural shift: the cord-cutting wave accelerated, and households that left pay TV needed a free alternative. Tubi, Pluto TV, Samsung TV Plus, Peacock, Prime Video FAST, and their peers rushed to fill the vacuum with linear streaming channels available at zero subscription cost. By 2025, roughly 45% of U.S. households, 38% of Brazilian households, and 35% of Spanish households were using at least one major FAST platform. The penetration numbers looked like a global revolution.

The revenue numbers told a different story. Gavin Bridge's reconstruction of the global FAST revenue map — drawing on Omdia's December 2025 data — collapses the narrative down to one blunt conclusion: the United States is the market, and everywhere else is a rounding error.

▶ Table 1. Global FAST Market — Monthly Penetration & 2025 Estimated Revenue

Sources: FASTMaster Intelligence estimates / Omdia December 2025 / Revenue in USD

Brazil is the most vivid illustration of the penetration-revenue disconnect. A population of 250 million, a FAST penetration rate approaching 38% — yet revenue of approximately $60 million, roughly one-ninetieth of the U.S. figure. Spain leads Europe in FAST penetration at 35% but trails Germany and the UK in actual dollars earned. The culprit is CPM (cost per thousand impressions) and ad fill rate: the U.S. advertising market is categorically different from every other geography.

“A global strategy that doesn't prioritize the U.S. first is just a hobby.” — Gavin Bridge, FASTMaster Intelligence Webinar

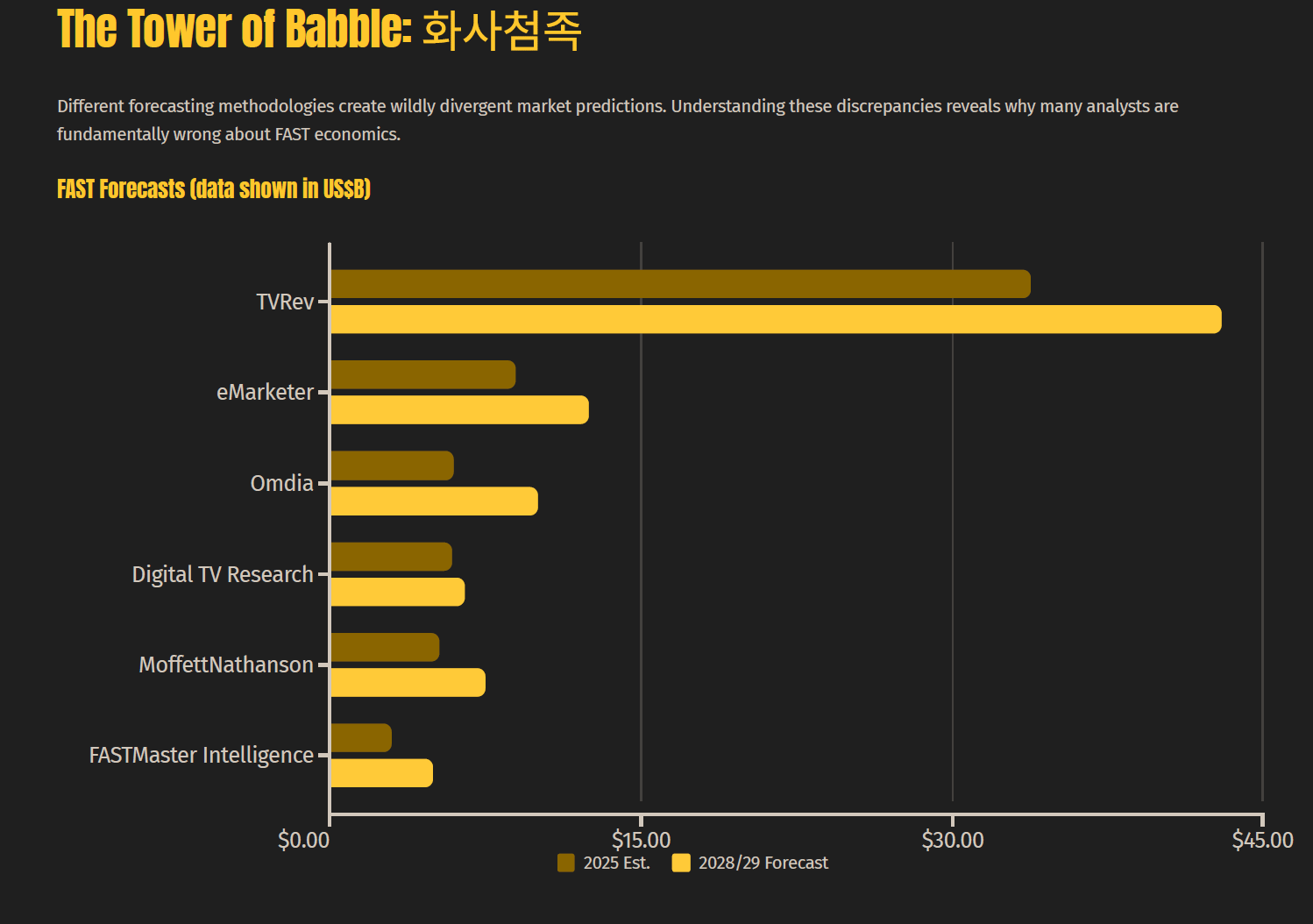

1-1. The Tower of Babel: Reading Market Forecasts Critically

Bridge opened his analysis with a Korean proverb — 화사첨족 (hwasa-cheomjok, "drawing feet on a snake") — applied to the FAST analyst community. A bewildering range of forecasts exists: TVRev and others project the U.S. FAST market reaching $10 billion or more by 2028–29. FASTMaster Intelligence puts the realistic figure at $4.2–6 billion. The gap is not accidental; it reflects a fundamental methodological choice about what gets counted as FAST revenue.

▶ Table 2. FAST Market Size — Bullish Forecasts vs. Unit Economics Reality

Sources: FASTMaster Intelligence / TVRev, Omdia, eMarketer, MoffettNathanson comparative analysis

The unit economics are unforgiving. At a current U.S. FAST average CPM of $14, a 55% ad fill rate, and an eight-minute ad load per hour (16 spots), each viewer-hour generates approximately $0.123 in revenue. Applied to an estimated 35 billion total FAST viewing hours, that yields around $4.2 billion — less than half the most bullish forecast.

To reach $10 billion by 2028 with 35 billion viewing hours, the average CPM would need to reach $33. That is the rate broadcast television charges during Super Bowl primetime. "Bae-boda bae-kkop-i deo keu-ne-yo" — the belly button is bigger than the belly. The optimism is bigger than the reality.

Channel saturation compounds the pressure. The total count of U.S. FAST channels grew from 414 in 2020 to 1,572 by 2026 — a 280% increase. Growth is now decelerating: 95% from 2020 to 2022, falling to just 24% from 2024 to 2026. Platforms are no longer accepting every channel offered; they are actively pruning underperformers. The top 20 channels — roughly 1% of the total — capture 60–70% of all revenue. The bottom thousand starve. This is natural selection, and it is accelerating.

Korea's elevated FAST closure rate cannot be explained by content quality. It is a structural problem. The advertising technology infrastructure that underpins the entire FAST ecosystem is architected, by default, to exclude non-English audio content from premium monetization. Korean channels are not failing despite good content — they are failing because the plumbing of the ad market routes them to the wrong section of inventory before a single viewer has even pressed play.

▶ Table 3. U.S. FAST Channel Closure Rates by Language (2020–2024 Cohort)

Source: FASTMaster Intelligence full cohort analysis / Excludes channels launched after 2024 / Minimum 5-channel threshold for statistical validity

2-1. The Invisible Wall: Three Ways Ad-Tech Blocks Subtitled Content

When major U.S. brands — Ford, P&G, Coca-Cola — set up campaigns inside demand-side platforms like The Trade Desk or Google DV360, their language targeting defaults to English only. That is not a quirk; it is the standard configuration, because the overwhelming majority of U.S. ad inventory is English-language. The ad server reads the audio track metadata tag, not the subtitle file. The subtitle could be perfect, pristine English — it does not matter. The system reads [Audio: Korean] and routes the content out of the premium auction before any human buyer even sees the opportunity.

The consequence of passing through all three filters in the wrong direction is placement in the remnant inventory market — where only direct-response advertisers and low-tier brands compete, at CPMs of $4–8. Dubbed content tagged [Audio: English] bypasses all three filters and competes at Tier 1 rates of $15–22 or higher. The revenue multiplier is not marginal. It is 3 to 5 times.

▶ Table 4. Subtitled vs. Dubbed Content — Ad Revenue Structure Comparison

Source: FASTMaster Intelligence / Amazon MGM Studios FAST operational data (Gavin Bridge, direct testimony)

2-2. Lean-Back Psychology: The Living Room Rejects Subtitles

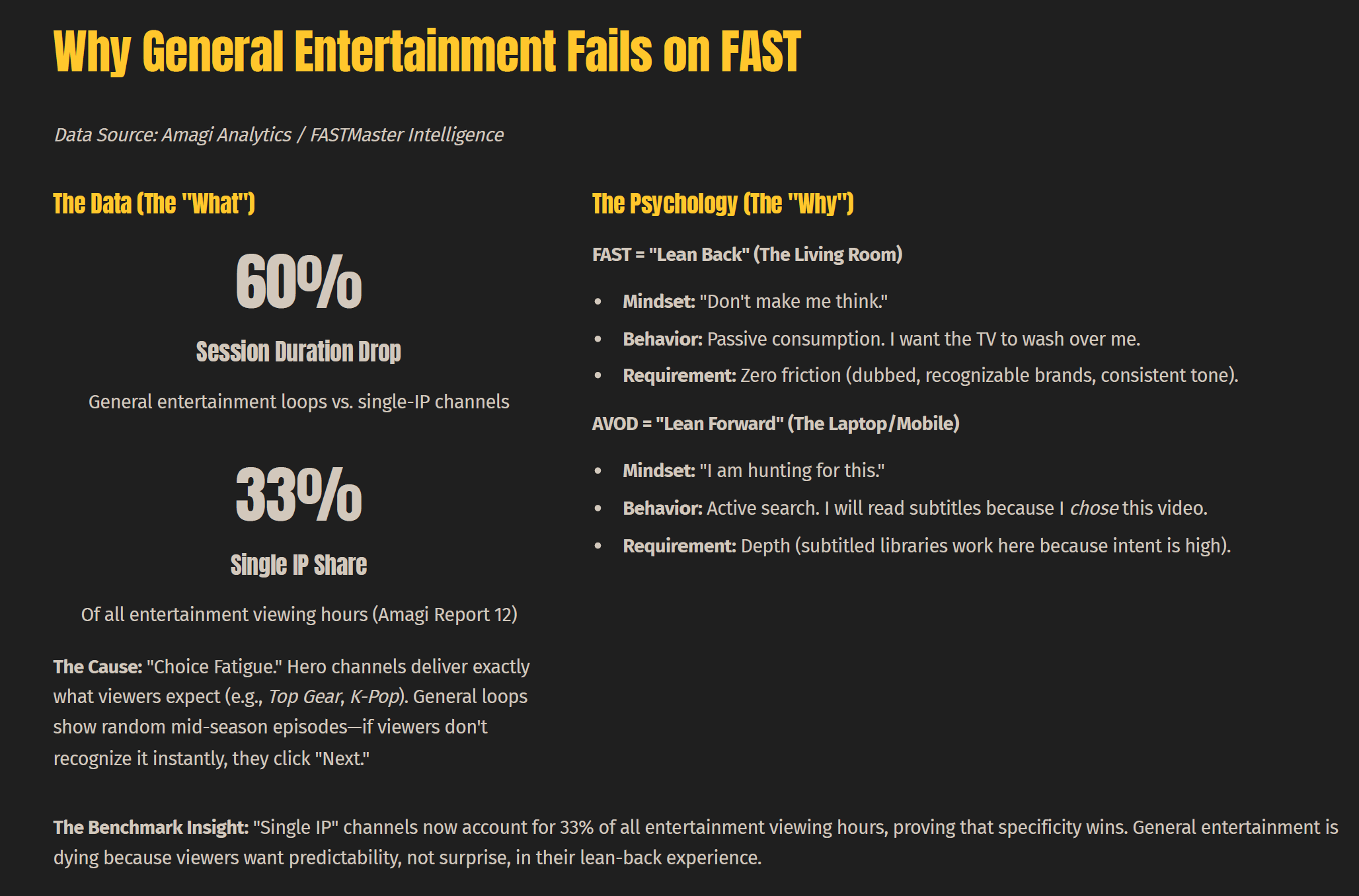

The ad-tech problem is structural, but there is a second and more fundamental barrier: the psychology of the lean-back viewing environment. Amagi's analytics data, covering the full ecosystem of channels they distribute, shows that single-IP channels (dedicated to one property) sustain 60 percentage points more session duration than general entertainment channels, and account for 33% of all entertainment viewing hours — despite comprising far fewer than 33% of available channels. The reason is how people watch TV.

FAST is a lean-back environment. The viewer is on a sofa, remote control in hand, not looking for anything in particular. The inner monologue is: 'Don't make me think. I want the TV to wash over me.' In this state of passive, zero-friction consumption, subtitles represent cognitive work. Linear channels cannot be paused or rewound. Miss a line of dialogue while the subtitles scroll, and the context is gone. The viewer changes the channel. It is that simple.

“I was doing my normal monthly check of the Zumo EPG two weeks ago and I got sucked into watching three episodes of Miami Vice — a show from the mid-eighties I'd never really seen before. I liked one of the cast and it was just on, and it washed over me. That is how FAST is supposed to work. Subtitles break that experience entirely.” — Gavin Bridge, webinar presentation

Bridge documented this empirically during his time running FAST channels at Amazon MGM Studios. His own channel, 'From Asia With Love,' and other Korean-, Japanese-, and Spanish-language subtitle-dependent channels consistently underperformed their dubbed counterparts. When his team switched certain channels to English audio, viewership doubled or tripled. This is not an anecdote; it is a pattern observed across multiple languages, repeated consistently enough to constitute evidence.

2-3. The Fandom Gap: 16.7 Million Fans, Less Than 1% Watch

The most counterintuitive finding in Bridge's data is the relationship between K-fandom scale and actual FAST viewership.

According to KOCCA's 2024 survey data, approximately 16.7 million Americans self-identify as Hallyu fans. The K-pop events market was valued at $8.3 billion in 2025. Searches for 'K-pop concert tickets' reached record highs in January 2026. By any measure, demand for Korean culture in the United States is at an all-time high.

And yet: viewer surveys of K-drama consumption showed that even devoted fans marked 'not interested' for approximately 25% of available dramas.

And the proportion of those 16.7 million fans who convert into regular FAST viewers of a subtitled Korean channel sits below 1%. The critical distinction is between liking something and tolerating friction to access it. K-content fans like Korean culture. They will not tolerate subtitles in a lean-back environment on a FAST channel. Demon Slayer's American success — zero week-over-week audience decline for weeks — is the counterexample: same Hallyu appeal, friction removed through dubbing and animation.

FASTMaster Intelligence tracked every Korean-language FAST channel that entered the U.S. market between 2020 and 2024 — 15 channels in total. The cohort analysis reveals a clear pattern of what kills channels and what keeps them alive. It is not luck. It is strategy.

▶ Table 5. K-FAST Channel Survival & Closure — Full Cohort Autopsy (2020–2024)

Source: FASTMaster Intelligence complete cohort tracking / * 'From Asia With Love' was directly operated by Gavin Bridge at Amazon MGM Studios

3-1. The 2020 Gold Rush Cohort: Total Wipeout and Its Lessons

Every channel that entered the U.S. FAST market in 2020 is gone. KMTV, HallyPop, New K.ID (early iteration), Kocowa Classic — all delisted. The common attributes are revealing. First, all operated with broadly Korean-culture programming rather than a focused vertical identity, leaving viewers unable to form a clear expectation of what the channel would deliver. Second, all relied entirely on subtitles. Third, all employed a library-dumping strategy — hundreds of episodes, minimal curation, maximum volume. The 2020 cohort believed that content abundance was the asset. It was the liability.

3-2. The CJ ENM Lesson: Brand Specificity Determines Survival

CJ ENM's trajectory within the FAST ecosystem is the single most instructive case study in the cohort. 'K-Content by CJ ENM' and 'CJ ENM Picks' — both structured around the studio's brand prestige rather than viewer-facing content identity — were delisted. 'K-Stories by CJ ENM' is active today. The difference is not production quality. The difference is that 'K-Stories' tells a viewer, in two words, what they will experience when they press play. 'Picks' tells a viewer nothing except that CJ ENM chose these shows — irrelevant information in a 1,500-channel EPG where viewer attention is measured in seconds.

“A lot of people think they have a channel. But what they actually have is a slot on a channel. Stop launching 600 channels. Launch one great FAST channel and build a massive YouTube library.” — Gavin Bridge

3-3. The NEW ID Model: Vertical Differentiation as a Survival Strategy

NEW ID's performance represents the clearest proof of concept for vertical strategy in the K-FAST space. By splitting into NEW KMOVIES, NEW KPOP, and NEW KFOOD — three distinct channels each oriented around a single genre — NEW ID gave viewers a simple value proposition: if you want Korean movies, this is your channel. If you want K-pop content, here. All three remain active. This is not coincidental. It directly validates Amagi's finding that single-IP and single-vertical channels sustain dramatically higher session duration than general entertainment programming, because viewers know what they signed up for when they stay in the stream.

4. The YouTube-FAST Flywheel: Redesigning the Distribution Architecture

One of the most consequential strategic reframes in K-FAST 2.0 is the repositioning of YouTube and FAST from competitor or substitute relationships into a complementary, role-differentiated dual structure. Bridge calls it the Two-Speed Strategy. Most Korean content distributors currently treat these platforms as interchangeable — or worse, they treat FAST as the primary destination and YouTube as an afterthought. K-FAST 2.0 inverts both assumptions.

▶ Table 6. YouTube/AVOD vs. FAST Linear — Platform Strategy Comparison

Sources: FASTMaster Intelligence / Amagi Analytics Report 12 / Samsung TV Plus platform data

4-1. The Cardinal Rule: 'If It Isn't Dubbed, It Stays on YouTube. If It's a Hit, It Graduates to FAST.'

The most common and costly mistake Bridge observes among Korean content companies is deploying FAST as a library dump: 500 episodes of legacy drama on a subtitled linear channel, left to generate whatever CPMs the remnant market provides. This strategy fails for the reasons already established — ad-tech exclusion, lean-back friction, and saturation. The K-FAST 2.0 alternative is architecturally simple but requires discipline.

YouTube carries depth: the full subtitled archive, fan-focused content, behind-the-scenes material, and anything that serves the super-fan who is actively searching. The FAST channel carries only the top 1–5% of the IP portfolio, dubbed, curated, and treated as appointment viewing. The mathematics justify the distinction: 1,000 FAST views generate the same advertising revenue as approximately 10,000 YouTube views. The strategic objective is to move the 'whale viewers' — the most engaged audience segment — from the lean-forward laptop experience to the lean-back TV screen, where premium CPMs apply.

4-2. The 24/7 YouTube Livestream: FAST's Secret Growth Engine

Bridge describes YouTube's always-on livestream format as 'the cheat code' — a low-cost, high-leverage mechanism for building the community infrastructure that FAST channels require. Running a 24/7 themed livestream (K-pop lo-fi, drama marathon, Korean cooking) costs approximately $800 per year in automation software. The channel keeps running without manual curation. The YouTube notification algorithm treats live content preferentially, distributing alerts to subscribers and generating recurring community touchpoints at minimal incremental cost.

The strategic value of the livestream extends beyond audience size. It produces data. When the chat fills with 'When is Season 2?' for a specific show, that is a dubbing priority signal. When a particular episode generates a spike in clip sharing to TikTok, that is a FAST programming signal. The livestream functions simultaneously as a marketing funnel ('Watch the dubbed premiere on Samsung TV Plus tonight at 8pm') and an audience research instrument. Both functions are available at a cost that any content company can absorb.

4-3. The Gen Z Imperative: YouTube Isn't Optional

One in three Gen Z consumers in the U.S. never opens an Electronic Program Guide. For this demographic — now aging into the prime 18–34 advertising target — FAST channels that exist only within the EPG effectively do not exist. A Korean content brand that invests exclusively in FAST is invisible to everyone under 30. This is not a marginal concern; it is a structural distribution failure.

YouTube and TikTok/Shorts are not alternatives to FAST — they are the on-ramps. Catch the younger audience where they live, create the relationship through the lean-forward interaction that platform affords, then convert the most engaged fans into the lean-back FAST viewership where the premium advertising economics operate. Each platform plays its role in a coordinated revenue sequence; neither is optional.

5. The AI Advantage: A Dubbing Cost Revolution and the 'Lazarus Strategy'

The most significant structural asymmetry in global content production right now is not about storytelling ability, production values, or distribution relationships. It is about regulatory paralysis. Following the historic SAG-AFTRA and WGA strikes of 2023, the U.S. entertainment industry operates under the most restrictive AI usage framework in the world. Every application of Generative AI to voice, performance, or script requires complex legal clearance, consent negotiations, and residual structures inherited from contracts written before the technology existed. Studio compliance departments are blocking an estimated 90% of AI experimentation to avoid triggering guild disputes or copyright claims.

Korea has none of these constraints. No legacy union agreements. No accumulated case law on AI performance rights. No compliance infrastructure oriented around protecting a pre-AI status quo. Bridge uses two words to describe the difference in posture: the U.S. is in 'Compliance Mode.' Korea is in 'Execution Mode.'

“By the time Hollywood lawyers finish renegotiating the contracts, Korea will already own the global infrastructure for localized content. No legacy debt equals maximum velocity.” — Gavin Bridge, AI trends section

▪ 5-1. The Economics of AI Dubbing: $70 Per Month

The cost barrier that once made professional dubbing prohibitive for mid-tier Korean content companies has effectively collapsed. Current commercial AI dubbing credit pricing runs at approximately $70 per month for four to six hours of dubbed output. This is not broadcast-quality dubbing from a standing start — professional voice actors and human QA layers remain advisable for FAST-bound hero content, where CPM premiums justify the additional investment. But for social media clips, YouTube content, and exploratory dubbing to test audience response, the cost is now negligible.

5-2. The Lazarus Strategy: Don't Just Remaster — Re-Imagine

Bridge coined the term 'Lazarus Strategy' for the AI-enabled revival of content that existing distribution channels have written off as dead inventory. The classic application is 4K AI upscaling of SD-format legacy hits — classics like 'Winter Sonata' or 'Jewel in the Palace' that platforms currently decline because of resolution limitations. AI upscaling restores these assets to platform-eligible condition at a fraction of traditional remastering cost.

The more radical application is Video-to-Video Generative AI transformation: taking a 2000s melodrama and processing it through a cel-shading filter that outputs a webtoon or anime aesthetic. The narrative is unchanged — the acting, the pacing, the emotional architecture that Korean drama writers have refined into one of the most addictive storytelling formats in global television. But the visual register shifts from 'legacy Korean drama that my parents watched' to 'new animated series.' The generational bridge is built without writing a single new line of dialogue.

A third application sits at the intersection of IP management and technology strategy: using the studio's existing content library as training data for proprietary AI models. A studio sitting on 1,000 hours of a particular actor's performances across multiple productions has something of considerable value — ground-truth data for a model that can generate new content featuring that actor's likeness with consent provisions already structured. The studios that begin this work now will have a multi-year head start on those that wait for Hollywood to resolve its regulatory standoff.

In January 2026 alone — a single month — three events signaled that the microdrama format had crossed from emerging trend into structural industry shift. Fox invested $22 million in a Series B round for vertical studio Holywater. TikTok launched 'PineDrama' in the U.S. market. Disney unveiled AI tools designed to convert its library content into vertical format for mobile-first distribution. These are not the actions of companies experimenting at the margins. These are mainstreaming moves by major studios betting on a format change that has already demonstrated its commercial logic.

The economics are compelling at every level. Production cost for a localized microdrama series: $100,000–$150,000, compared with millions for traditional K-drama production. Production timeline: 10–14 days. Revenue potential: the 'coin model' common in Chinese microdrama platforms — where viewers pay micro-transactions per episode to continue watching — generates ARPU of up to $4.70 per download in the U.S. market, exceeding subscription streaming margins on comparable content. FASTMaster Intelligence projects the U.S. microdrama market reaching $9 billion by 2028, which would make it larger than the pure FAST market — though the comparison is imperfect since microdrama revenue skews toward subscription and micro-transaction rather than advertising.

6-1. Global Casting: The Cultural Hack That Removes the Foreign Barrier

For K-content companies, the most strategically significant feature of microdrama economics is not the cost reduction — it is the format's compatibility with global casting from Day 1. Bridge describes the old production model as: shoot in Korea, add subtitles, hope Americans watch. The new model is simultaneous global production: Korean scripts and directors, but a cast assembled as an international ensemble.

A Korean lead paired with a Black Canadian co-lead. A Korean female protagonist with a European male love interest. The K-drama addiction mechanics — the destined-lovers construction, the slow-burn emotional tension, the cathartic confrontation — remain fully intact. But the face the viewer sees is not categorically foreign. The content is native to multiple audiences from the moment of release, without requiring translation to feel accessible. The success of Netflix's Bridgerton — a mixed-ethnicity cast placed in a historically implausible Regency England — with younger demographics is Bridge's reference case: cultural specificity plus casting universality equals breakout reach.

“A 10-year-old watching Minecraft will not read subtitles. If you want to crack the U.S., it has to be dubbed. MrBeast dubs his content into 30-plus languages. He knows that to go global, you have to sound local.” — Gavin Bridge

The playbook Bridge presented is not a theoretical framework. Every element was developed from hands-on channel operations at Amazon MGM Studios and subsequent consulting work across the FAST ecosystem. The three phases are sequential and self-financing: each phase generates the data and revenue that funds the next.

▶ Table 7. K-FAST 2.0 Three-Phase Execution Roadmap

Source: FASTMaster Intelligence K-FAST 2.0 Playbook (Gavin Bridge, February 2026)

Phase 1: Audit and Upgrade — Find the Heroes, Don't Dub the Library

The most expensive mistake a Korean content company can make entering FAST is trying to dub its entire catalog. The math does not work, the timeline is unmanageable, and most of the content will not generate sufficient viewership to justify the investment. Phase 1 is about surgical identification: use YouTube channel analytics — view counts, watch-through rates, comment sentiment, clip-sharing frequency — to identify the top 5% of the portfolio by audience engagement. These are the heroes. Everything else stays on YouTube, subtitled, serving the super-fans who will seek it out.

The heroes go through AI plus human QA hybrid dubbing, targeting a four-week turnaround. Simultaneously, the SD-format library hits with proven audience attachment — the equivalent of 'Winter Sonata' or 'Jewel in the Palace' — go through AI 4K remastering to restore their platform eligibility. The output of Phase 1 is a slate of content that can be submitted to FAST platforms with [Audio: English] metadata correctly tagged, making it eligible for the $15–22+ CPM tier on Day 1 of distribution.

Phase 2: The Community Engine — Let the Data Tell You What to Dub Next

Phase 2 is a patience play. The 24/7 YouTube livestream goes live: K-pop, gaming, drama marathon, or whatever vertical the brand identity supports. TikTok and Shorts receive a consistent flow of vertical clips — existing content clipped to the short-form format, or purpose-built content designed to drive algorithmic discovery. The community builds.

The critical discipline in Phase 2 is treating the community as a data source rather than just an audience. Which clips get reshared? Which comments ask for more of a specific show? What does the livestream chat say at 11pm on a Tuesday? This intelligence directly informs Phase 3 programming decisions. 'If they ask for Season 2 in the chat, you dub Season 2' is the operational principle Bridge describes — remarkably simple, and genuinely effective as a capital allocation heuristic. The livestream simultaneously functions as a marketing channel: 'Watch the 4K dubbed version on Samsung TV Plus tonight' embedded as on-screen text during live programming.

Phase 3: The Premium Launch — Make It an Event, Not a Test

FAST channel launches that are framed as experiments tend to produce experimental results: minimal promotion, cautious programming, limited platform support. K-FAST 2.0 Phase 3 treats the launch as the main event. The hero content is dubbed and ready. The community is built and primed. The metadata — particularly the [Audio: English] tag — is verified across every platform submission. This single tag is what unlocks the premium CPM tier; its absence relegates the channel back to the remnant market regardless of content quality.

Samsung TV Plus, Tubi, Pluto TV, and equivalent tier-one platforms receive simultaneous channel submissions. Where exclusivity deals or curated tile arrangements are available, they are pursued actively. And alongside the hero channel launch, Phase 3 includes the greenlight of a single global-cast microdrama pilot: one episode, purpose-built to prove the production model, at a cost of $100,000 or less. The pilot is both a product and a signal — to platforms, to partners, and to the broader industry — that the brand is operating in the future format, not the past one.

▪ Q: AI dubbing sounds expensive. Where do small and mid-size Korean content companies even begin?

Bridge's answer was deliberately grounding: 'Start with $70 a month in AI dubbing credits and clips for social media. You don't need to dub the whole library. You need one clip that gets picked up by the algorithm.' The strategic entry point for smaller companies is not the FAST channel at all — it is the YouTube Shorts clip, dubbed, that proves audience response exists before any meaningful capital is deployed. The platform-agnostic principle is that viral community content precedes premium distribution investment; the technology now makes that sequencing affordable for companies at virtually every scale.

Key takeaway: Start with precision, not scale. Social clip dubbing → YouTube response validation → hero IP identification is the low-risk sequencing that minimizes early-stage capital exposure.

▪ Q: We have strong K-drama IP and millions of YouTube viewers, but almost no FAST revenue. Should we just focus on YouTube?

Bridge referenced WWE as a parallel case: a company with such dominant YouTube economics that FAST initially seemed redundant. His answer was not either/or. 'If you can create a premium version of your YouTube channel that justifies the FAST treatment — dubbed, curated, appointment-viewing — then yes, absolutely pursue it. But if you're generating strong YouTube numbers on subtitled content, the question is whether your hero IP can be dubbed for FAST specifically, because the CPM multiple is real.' The option he flagged as potentially most lucrative for companies with deep subtitled libraries is content licensing: curated K-drama tiles within existing AVOD platforms, where the volume of available inventory creates a discovery mechanism that a standalone channel cannot.

Key takeaway: YouTube and FAST are not competitors. YouTube is the lab; FAST is the bank. The prerequisite for FAST entry remains English dubbing and hero IP selection — without these, the premium tier is inaccessible regardless of YouTube success.

▪ Q: What global AI infrastructure opportunity can Korea realistically capture through the dubbing advantage?

Bridge's answer extended the strategic horizon significantly. He estimated that 10–20% of the global population has an active interest in Korean content, and that this audience skews younger and more valuable to advertisers. The company or country that builds the AI dubbing and localization pipeline first does not just serve K-content — it becomes the infrastructure provider for all content requiring Korean-to-English, English-to-Spanish, English-to-Portuguese localization at scale. Korea's existing strength in high-quality video production, combined with AI dubbing capability developed and refined through K-content applications, positions it to offer localization-as-a-service to content companies globally. 'The dubbing capability unlocks so much more than K-drama,' Bridge noted. 'True crime, food, documentary — every genre that has voracious appetite in specific markets benefits from the same technology.'

Conclusion: The World Is Waiting — But It Is Waiting in English

Gavin Bridge closed the webinar with a sentence that functions as both summary and challenge: 'The world is waiting for K-content. They're just waiting in English. And Spanish. And Portuguese. They're waiting in their local languages.' This is not a criticism of Korean storytelling. It is a precise diagnosis of the distribution problem. The stories are wanted. The format in which they arrive is not working.

The gold rush of 2020 is over. In a market of 1,572 channels where the top 20 capture 70% of revenue, 'more channels' is not a strategy. 'Better channels' is only a partial strategy. The complete strategy — the K-FAST 2.0 strategy — is channels that reach the audience in the language their advertising ecosystem can monetize, through a distribution architecture that meets Gen Z on YouTube before graduating them to the living room TV, with content curated to the lean-back consumption context that FAST is actually designed to serve.

Korea stands at a historically specific moment of advantage. Hollywood is paralyzed by regulatory constraints it cannot resolve quickly. The studios that will own the global localization infrastructure of the next decade are the ones building it now, unencumbered by legacy union agreements and AI use restrictions. Korean production capability is world-class. Korean technology infrastructure is world-class. The only gap between where K-content is and where it could be is the audio tag: [Audio: Korean] to [Audio: English]. That is the subtitle trap. That is K-FAST 2.0.

Let's stop building libraries for the past. Let's build a brand for the future.Dub your heroes. Launch your community engine. Graduate to FAST. The blueprint is complete. — Gavin Bridge

■ Sources & References

※ This article is an editorial reconstruction and analysis of the K-EnterTech Hub webinar presentation delivered by Gavin Bridge of FASTMaster Intelligence. Market figures and revenue estimates reflect the presenter's proprietary calculations and cited third-party sources; they should not be taken as official industry statistics without independent verification. This content does not constitute investment or business advice.

![[보고서]전통 언론사의 크리에이터 전략 대전환](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/02/0nwc9z_202602100212.png)