The Storm Is Coming. Are You Ready? Amy Webb kills the 19-year-old trend report — and launches the age of Convergence

by

2026년 3월 15일

Approved in 121 Days — The Triple Political Force of FCC, DOJ & the Trump White House

Eight State AGs & DirecTV File Antitrust Suits / Structural Shock to K-Content Global Distribution Strategy

Jung Han

Jung Han

The Nexstar–TEGNA merger traces its formal regulatory timeline to November 18, 2025, when Nexstar submitted its acquisition application to the FCC. Exactly 121 days later, on March 19, 2026, the FCC Media Bureau issued its approval order — and Nexstar closed the transaction the same afternoon, before opponents could mount a legal challenge. No U.S. television merger of this scale has ever moved this fast.

The speed becomes legible only when set against its political context. The Biden-era FCC, under Chair Jessica Rosenworcel, spent 309 days reviewing Standard General CEO Soo Kim's competing bid for TEGNA before effectively killing it with procedural delays. Rosenworcel's commission demanded extensive public interest showings and invoked processing concerns that industry observers widely characterized as manufactured obstacles. Brendan Carr's FCC ran the opposite playbook, completing review in less than half that time.

The most remarkable aspect of this approval, however, is what happened in the political theater surrounding it. On February 7, 2026, President Donald Trump posted directly on social media: 'Get that deal done!' — arguing that a combined Nexstar–TEGNA would 'knock out' ABC News and NBC News, which he called 'Fake News National TV Networks.' FCC Chairman Brendan Carr publicly echoed the sentiment within hours: 'Let's get it done.' A sitting president openly pressing for the approval of a specific private-sector M&A deal represents an extraordinary departure from regulatory norms.

There was internal friction even within Trump's circle. Newsmax CEO Chris Ruddy — a close Trump ally — strongly opposed the merger, citing fears that a dominant Nexstar would squeeze Newsmax's own distribution and advertising, given that Nexstar operates the competing CW Network. Ruddy reportedly threatened legal action. That Trump nonetheless sided with Nexstar CEO Perry Sook over his longtime friend signals just how politically calculated this approval was. Washington and Wall Street analysts suggest the president's public endorsement served as a crucial political shield that kept the DOJ and FCC on an accelerated track.

For Korean media companies watching from Seoul, the implications run deep. The speed and political character of this approval means that the U.S. local broadcast market's regulatory environment is now openly tied to the political cycle in a way it has not been in decades. Any future partnership or licensing deal with a major U.S. broadcaster must be evaluated not just on commercial terms, but on the political durability of the regulatory framework underpinning it.

■ 1-1. The 39% Ownership Cap: Agency Rule or Statutory Limit?

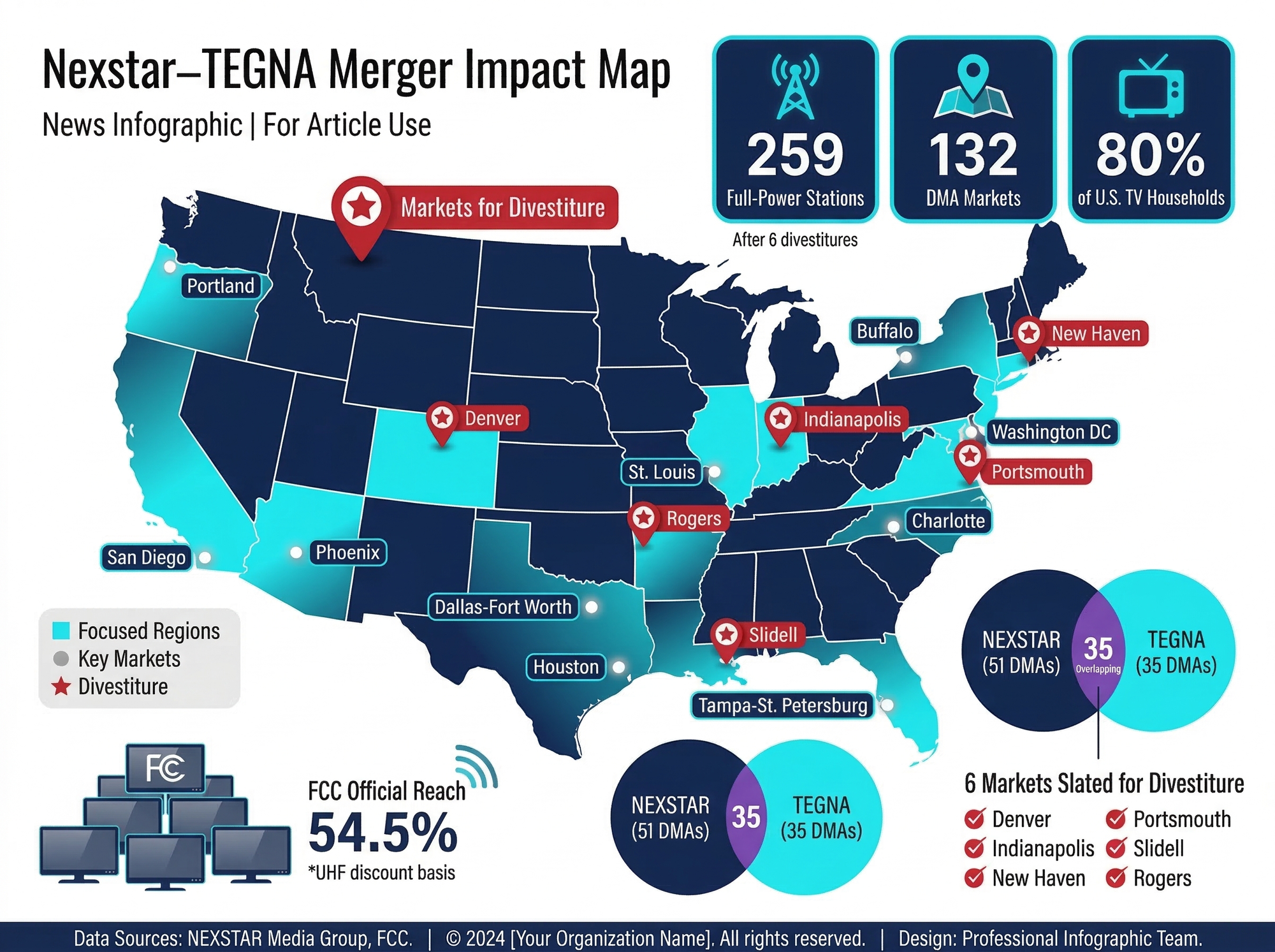

The central legal dispute surrounding the merger concerns the nature of the FCC's 39% national TV household reach cap — a rule that prohibits any single broadcaster from owning stations that collectively reach more than 39% of U.S. TV households. Congress introduced this cap in 2004 precisely to prevent the kind of concentration this merger now creates. The combined Nexstar–TEGNA reaches 80% — more than double the cap.

Opponents of the merger argued the 39% cap was a statutory limit set by Congress, beyond the FCC's authority to waive. Chairman Carr rejected this interpretation outright, citing a D.C. Circuit Court ruling that characterized the cap as an agency rule rather than a firm statutory limit — a distinction that gives the FCC authority to grant waivers on a case-by-case basis. Democratic Commissioner Anna Gomez dissented sharply, arguing the commission had effectively nullified a Congressional mandate. In a 3-to-2 vote, she was outvoted.

The precedent set here extends far beyond this single deal. If the 39% cap is an agency rule, then any future FCC — regardless of political stripe — can grant the same waiver to the next mega-merger candidate. More immediately, if Carr moves to formally repeal or raise the cap during his tenure, Nexstar's obligation to divest six stations within two years could become moot: there would be no ownership rule left to justify the divestitures.

The FCC's approval order already permits Nexstar to operate triopolies (three stations in a single market) in 23 markets pending the divestitures, stating that 'competition will not be unduly harmed during the period of common ownership.'

■ 1-2. The Combined Entity: Scale by the Numbers

■ 1-3. The Six Required Divestitures — And Why They May Never Happen

The FCC conditioned approval on Nexstar divesting six stations within two years. The most politically significant of these is WTHR, an NBC affiliate in Indianapolis — a concession Carr granted after Circle City Broadcasting CEO DuJuan McCoy, an African American broadcaster, petitioned the FCC to block Nexstar from owning the CBS, Fox, and NBC affiliates in the 25th-largest U.S. market simultaneously. Carr framed this as consistent with his goal of strengthening minority-owned broadcasters.

These divestitures, however, carry a major asterisk. If the FCC under Carr moves to formally repeal the 39% cap or to allow three-station ownership in all 210 U.S. markets without restriction, Nexstar would have no legal obligation to sell any of the six stations.

As Policyband noted, 'in the end, [Nexstar] might not need to [sell] if the FCC allows the ownership of three TV stations in all 210 TV markets without restriction during the interval.' The divestitures are, in practice, a conditional obligation tied to the durability of rules that may themselves be dismantled.

By the time Nexstar declared the deal closed on March 19, the opposition had already mobilized. The previous evening — March 18 — attorneys general from California, New York, Colorado, Illinois, Oregon, North Carolina, Connecticut, and Virginia filed a federal antitrust lawsuit in the Eastern District of California, seeking to block the merger. DirecTV filed a separate suit the same day in Sacramento federal court.

Nexstar's response was to ignore both. Court filings from the states reveal that plaintiffs sent written notice to Nexstar's lawyers requesting that the company refrain from closing the transaction until after a final judgment. Nexstar did not acknowledge the request. Hours after the FCC and DOJ simultaneously announced approval, Nexstar declared the deal closed. The states argue this was not merely impolite — it was a deliberate strategy to commingle assets and operations so rapidly that judicial unwinding would become practically impossible, regardless of the legal outcome.

On March 20, the eight states filed an emergency motion for a Temporary Restraining Order (TRO), demanding that a federal court order Nexstar to 'hold separate' the acquired TEGNA assets — preventing integration until the underlying antitrust case is resolved. The legal battle remains active as of publication.

■ 2-1. The Eight States' Core Antitrust Claims

Led by California Attorney General Rob Bonta, the eight-state coalition — all with Democratic AGs — invokes Section 7 of the Clayton Act, which prohibits acquisitions that substantially lessen competition or tend toward monopoly. Bonta called the merger 'illegal, plain and simple.' The coalition's central allegations include:

● Unprecedented concentration of broadcast programming production and distribution in the hands of a single entity, degrading content diversity

● Already-documented layoffs of veteran journalists and consolidation of newsrooms at Nexstar- and TEGNA-affiliated stations in Los Angeles, Chicago, and New York

● Near-certain consumer price increases as Nexstar leverages its retransmission consent power to raise fees passed on through cable, satellite, and fiber-optic TV

● Loss of viewpoint diversity in local news where Nexstar will simultaneously control multiple Big Four affiliates (ABC, CBS, NBC, FOX)

● Elimination of meaningful competition in local advertising markets, severely limiting options for small and mid-sized advertisers

■ 2-2. DirecTV's Standalone Suit: The 'Retransmission Bomb' Warning

DirecTV's complaint focuses less on public interest theory and more on raw market economics. As a multichannel video programming distributor (MVPD) that must annually renegotiate retransmission consent agreements with local broadcasters, DirecTV faces a direct and imminent financial threat from the merger. Its filing documents a striking historical trend: local broadcast retransmission consent fees have increased approximately 5,000% — from roughly $214 million in 2006 to an estimated $11.9 billion in 2025.

DirecTV argues that Nexstar's new scale — 228 stations, 132 markets, 80% of U.S. TV households — will increase concentration in more than a dozen local markets by more than ten times the amount that is 'presumptively unlawful' under antitrust law. The suit warns that the combined entity's ability to threaten blackouts of NFL games, NCAA sports, and network programming during retransmission negotiations will be dramatically amplified in overlap markets including Austin, Denver, Charlotte, Cleveland, Columbus, New Orleans, Portland, San Diego, St. Louis, and Tampa.

DirecTV's complaint contains a formulation that may become the defining slogan of the anti-merger campaign: 'This acquisition will deliver the opposite of what competition is supposed to deliver — higher prices and lower quality. DirecTV and its subscribers will end up paying more to get less.'

Washington-based media policy publication Policyband issued its 'Winners and Losers' scorecard in the immediate aftermath of the deal's closing. The scorecard is worth examining not merely as a summary of outcomes, but as a map of how power and leverage shifted across the U.S. broadcast ecosystem in a single transaction.

The most striking entry in the Winners column is its final line: 'millions of American viewers who continue to rely on free TV.' The FCC and Nexstar both argue the merger strengthens the financial viability of free over-the-air broadcasting, protecting access for cord-cutters and low-income households who depend on antenna-based reception.

The eight state AGs and DirecTV argue the exact opposite — that rising retransmission fees lead inevitably to higher cable bills, diminished local newsrooms, and fewer programming choices. That the same merger generates irreconcilably opposing forecasts from regulators, litigants, and analysts is itself the most accurate measure of how consequential and contested this deal truly is.

The Losers column tells a coherent political story. Its entries share a common thread: every entity that argued for viewpoint diversity, minority community representation, consumer protection, or competitive markets finds itself on the losing side.

The Winners column is anchored by the Trump White House, Carr's FCC, and the capital interests of Nexstar and TEGNA shareholders. This is not a coincidental alignment — it is a direct reflection of how political power in 2026 America translates into regulatory outcomes in media markets.

At first glance, a consolidation among American local TV station groups might seem irrelevant to Seoul. It is not. The U.S. local broadcast ecosystem is the layer of the American media market where Korean broadcasters have been quietly, persistently building infrastructure — through retransmission agreements, subchannel licensing, ATSC 3.0 partnerships, and FAST channel distribution. The Nexstar–TEGNA merger restructures every one of those relationships simultaneously.

The timing is particularly acute. South Korea is at an inflection point in its U.S. market strategy. SBS has signed a strategic partnership with Sinclair to launch K82, a dedicated Korean content channel delivered via NextGen TV (ATSC 3.0) infrastructure — the first K-content channel ever to be broadcast on U.S. over-the-air television, targeting tens of millions of households in major U.S. cities. Separately, Korea's Ministry of Science and ICT has selected 20 official K-FAST channels and is AI-dubbing over 4,400 K-content titles into English, Spanish, and Portuguese for delivery to Samsung TV Plus, LG Channels, and other global FAST platforms. This is explicitly framed as Korea's 'Act 2' for U.S. market entry — moving beyond Netflix dependency into direct-to-consumer distribution. The Nexstar–TEGNA merger lands precisely at this strategic moment, reordering the counterparty landscape Korean players must navigate.

■ 4-1. The Collapse of Bilateral Leverage: Buyer Power Concentrates

The most immediate and concrete change is in the structure of retransmission and licensing negotiations. Until now, Korean broadcasters and K-content distributors operating in the U.S. have been able to negotiate with multiple competing counterparties — Nexstar, TEGNA, Sinclair, Gray Television, and others — in parallel. When one negotiation stalls, there is an alternative. Competition among station group buyers provides a floor under licensing rates and contract terms.

After the merger, that competitive structure is gone. A single entity controlling 80% of U.S. TV household reach across 132 markets becomes, in economic terms, a monopsonist — a dominant buyer with no credible competition. For K-content suppliers, the operational consequences are stark:

● Downward pressure on licensing rates: With no competing buyers, price discovery shifts entirely in Nexstar's favor

● Exclusivity demands: A dominant buyer can credibly demand first-window or exclusive supply rights, blocking parallel deals with other MVPDs and FAST platforms

● Standardized take-it-or-leave-it contracts: The bespoke, market-by-market negotiation model gives way to a centralized master agreement with standardized terms

● Single point of failure: If the relationship with Nexstar sours, access to the entire U.S. local broadcast layer is foreclosed simultaneously

● December 2026 pressure: After the retransmission rate freeze expires, Nexstar's after-acquired clause activates, creating a renegotiation cycle that could simultaneously pressure K-content licensing terms

■ 4-2. KBS SBS: The Partnership Model Must Be Rebuilt

Korean broadcasters’ current U.S. operations were built for a fragmented local‑station market, not for a Nexstar‑style national super‑buyer. KBS America distributes Korean‑language channels through cable and satellite (Comcast, Spectrum, DirecTV) and over‑the‑air subchannels in core Korean‑American markets, while SBS is in parallel pushing the terrestrial K‑Channel 82 rollout with Sinclair on NextGen TV infrastructure. Streaming‑only plays like KOCOWA and OnDemandKorea cover the OTT layer, completing a patchwork portfolio of relationships assembled station‑by‑station and platform‑by‑platform over the past decade.

That model depended on having multiple mid‑sized groups and independent stations with comparable bargaining power in each DMA; Korean broadcasters could always walk across the street to a rival owner if talks stalled. In a Nexstar‑dominated landscape, that exit option erodes: the real decision‑makers Korean players must reach are no longer scattered among local GMs in Los Angeles, New York, or Dallas, but concentrated at corporate headquarters in Irving, Texas. Practically, every Korean broadcaster with a U.S. footprint now needs to: audit existing agreements with former Tegna affiliates, check assignment and change‑of‑control clauses, map which Tegna executives are being retained inside Nexstar and which are exiting, and stand up direct, senior‑level lines into Nexstar’s content, distribution, and strategic partnerships teams. Relationship capital accumulated over years with local station managers can disappear overnight when ownership and reporting lines flip; in the Nexstar–Tegna era, the partnership model itself has to be rebuilt around a small number of national gatekeepers rather than dozens of local doors.

■ 4-3. FAST Strategy: Crisis and Opportunity Are the Same Thing

The global FAST business is forecast to expand from roughly 6 billion dollars of revenue in 2025 to around 11 billion by 2030, with the U.S. alone expected to generate close to 80% of that total — by far the world’s largest single FAST market. Omdia’s work on Netflix and FAST viewing shows Korean series as the most consistently watched non‑English titles on global SVOD, positioning K‑content as the natural premium import for ad‑supported streaming as well.

Nexstar is already behaving like a FAST‑native broadcaster rather than a pure linear group: NewsNation is carried across all major cable, satellite, and vMVPD bundles (YouTube TV, Hulu Live, DirecTV Stream, FuboTV) and also lives as a standalone CTV app, while the CW Network is being repositioned around low‑cost sports and reality franchises aimed at streaming‑first younger audiences; inside Nexstar, executives openly describe the core broadcast ad business as “a melting ice cube” that must be replaced with digital and CTV revenue, making FAST the primary candidate to absorb that pressure rather than a side experiment.

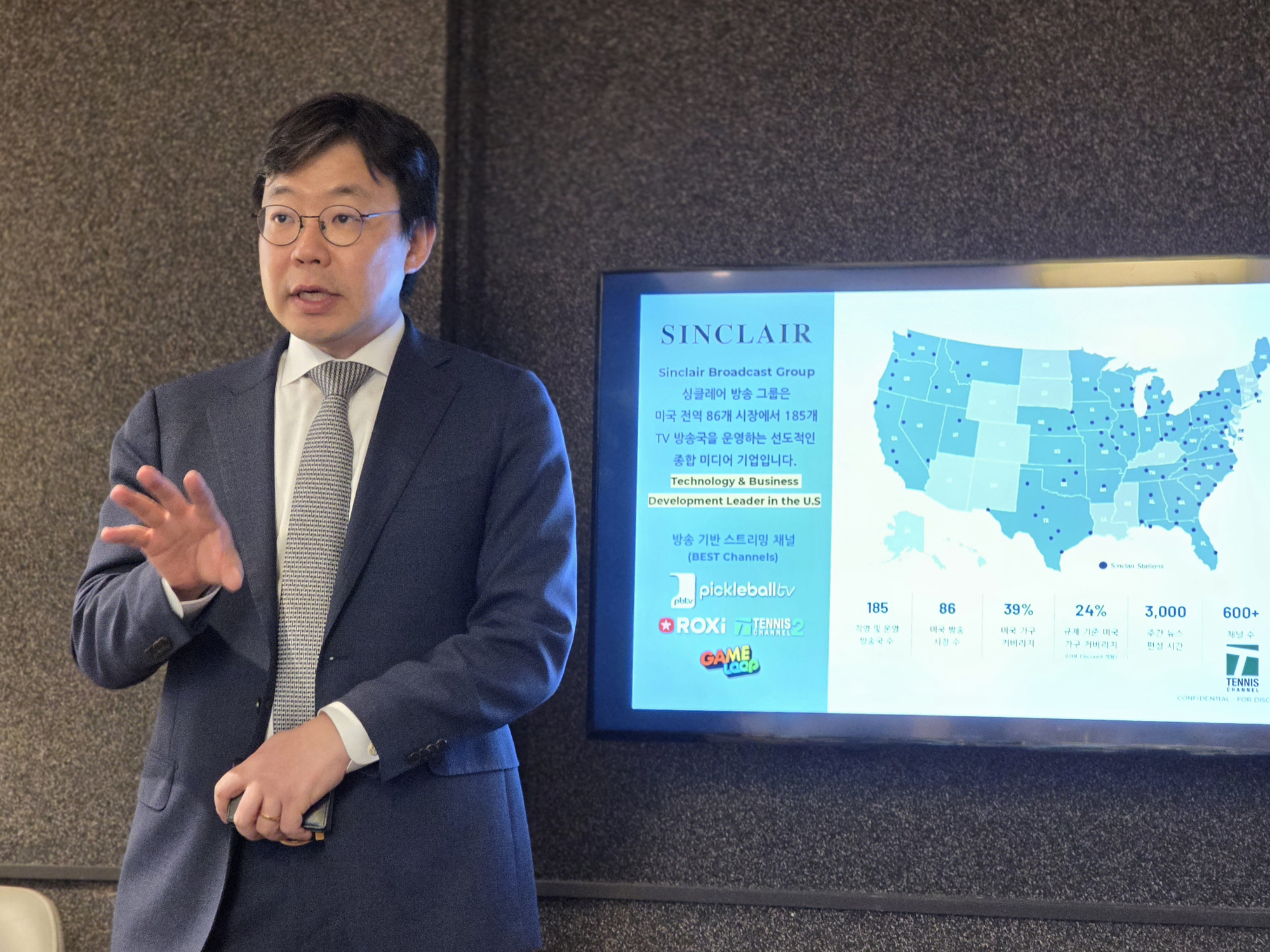

At the same time, Sinclair is moving in parallel from a different angle: its ATSC 3.0/NextGen TV footprint and the K‑Channel 82 partnership give Korean content a terrestrial and hybrid‑OTT on‑ramp into millions of U.S. TV households, with KBS programming K‑Channel 82 and exporting its disaster‑alert technology, SBS feeding K‑drama and variety blocks into Sinclair’s 185‑station networkand MBN opening an additional news‑and‑current‑affairs lane into the same infrastructure — effectively turning Sinclair into a second national‑scale gatekeeper for K‑FAST and K‑linear experiments, with K82 as a showcase for how Korean drama and entertainment can drive incremental reach, time‑spent, and targeted ad formats over broadcast‑IP rails.

In this combined landscape, K‑content stops being “nice‑to‑have” filler and starts to look like a strategic lever for both Nexstar and Sinclair: Nexstar’s core strengths remain local news, weather, and live sports, and Sinclair’s portfolio is similarly weighted toward local, sports, and data‑driven NextGen services, leaving both groups with limited international catalogs, constrained scripted drama pipelines at scale, and relatively little youth‑skewing entertainment beyond the CW; Korean drama, variety, and K‑pop‑adjacent formats — already over‑indexing on Netflix and other global platforms — can plug those gaps at a more efficient cost than commissioning U.S. originals while bringing built‑in fandom and strong repeat‑viewing behavior, so the joint pitch to Nexstar and Sinclair is not simply “license our shows” but “let K‑content become your audience‑diversification and revenue‑replacement engine across FAST, CTV apps, and NextGen TV channels,” with K82 as proof‑of‑concept on the Sinclair side and Nexstar’s NewsNation/CW rails as the scalable counterpart.

If you zoom out, that same structure can also be turned into a demand‑side platform for Korean advertisers rather than only a supply‑side play for Korean content: KBS is South Korea’s public broadcaster, with a dedicated U.S. arm (KBS America) and the global KBS World channel already reaching Korean‑speaking audiences across North America; SBS is a major nationwide commercial network and one of Korea’s primary sources of hit dramas and variety shows; and MBN is a national cable news and general programming channel with a strong position in business and current‑affairs coverage, and all three are now plugging into Sinclair’s NextGen TV and multicast footprint via K‑Channel 82 and related agreements, turning Sinclair into a de facto U.S. hub for Korean news, drama, and entertainment windows. On the advertising side, Korea Broadcasting Advertising Promotion Corporation (kobaco) functions as the government‑backed media representative for Korea’s major terrestrial broadcasters and operates programs and funds explicitly aimed at helping Korean brands use advertising to expand overseas, so instead of KBS, SBS, and MBN each selling a handful of spots around imported shows on their own, kobaco can aggregate inventory across their U.S. outlets — K‑Channel 82 on Sinclair, Korean‑language blocks on other local stations, and any K‑FAST or connected‑TV channels — and package it as a single, measurable buy that reaches both Korean‑American households and broader K‑culture fans across U.S. terrestrial, NextGen, and CTV environments.

The logical next step is to take that “K‑platform” from a Sinclair‑only construct to something that also speaks to a post‑merger Nexstar: Nexstar controls the largest local‑TV footprint in the U.S. and is under intense pressure to grow digital and FAST revenue, while Sinclair controls a leading NextGen TV network that is already experimenting with K‑Channel 82, so if KBS, SBS, and MBN can align their U.S. rights, windowing, and format strategies on one side and kobaco can serve as the single point of contact for Korean advertiser demand on the other, the pitch to both Nexstar and Sinclair becomes one coordinated Korean content and advertising bundle that fills specific programming gaps (scripted, youth‑skewing, international) while also bringing new export‑oriented ad budgets onto their FAST, CTV, and NextGen rails

■ 4-4. Korean-American Communities: Cord-Cutting as Structural Demand Shift

DirecTV’s lawsuit explicitly warns that a merged Nexstar–TEGNA will use its expanded leverage to raise retransmission consent fees, which will in turn push up cable and satellite bills nationwide. For Korean-American communities clustered in metros like Los Angeles, New York, Chicago, Washington D.C., and Dallas — all top‑ten Korean-American population centers where pay‑TV already eats into constrained household budgets — even modest price hikes can accelerate cord‑cutting decisions from “someday” to “now.”

Paradoxically, that structural shock creates a tailwind for Korean FAST and AVOD services rather than a headwind. As Korean-American households drop cable and satellite, their demand for free or low-cost, internet-delivered Korean news, drama, and variety will rise, and channels like KBS World (via linear and Streaming), MBC and SBS’s FAST offerings, and community-focused brands such as Channel K are well positioned to absorb those “displaced” viewers.

If Nexstar’s centralized programming and newsroom consolidation ultimately reduce or homogenize Korean-language blocks on former TEGNA stations in Koreatown-heavy markets, that local linear gap will push even more community media consumption onto digital platforms — precisely the layer where Korean broadcasters, K‑FAST operators, and K82 are now investing as their primary growth path

Appendix: How Korea’s Major Broadcasters and kobaco Fit Together

South Korea’s television market is anchored by three nationwide networks — KBS, MBC, and SBS — plus a newer national cable news and general channel, MBN, with kobaco acting as the central advertising gatekeeper for most terrestrial inventory.

KBS (Korean Broadcasting System)

MBC (Munhwa Broadcasting Corporation)

SBS (Seoul Broadcasting System)

MBN (Maeil Broadcasting Network)

Kobaco (Korea Broadcast Advertising Promotion Corporation)

The merger’s final legal form is not fixed; it is in motion, sitting at the intersection of federal approval and active litigation. Eight state attorneys general are asking a federal court for an emergency restraining order to “hold separate” the former TEGNA assets, DirecTV has filed a standalone federal antitrust suit focused on retransmission fees, and judges retain the power to impose structural remedies or even unwind pieces of the deal despite the FCC and DOJ approvals already in hand.

For Korean media stakeholders, this means strategy cannot be built on a single outcome; it has to be designed to survive several different legal futures while still exploiting the one constant in the picture — a U.S. market where local broadcast power has already collapsed into a small number of super‑groups and where FAST/CTV is the only real growth engine left.

At the same time, the upside window for K‑content has never been larger. Omdia’s data show the U.S. commanding around 80% of global FAST revenue by 2030 and Korean shows leading global non‑English viewing on Netflix, making K‑FAST in America a multi‑billion‑dollar opportunity in its own right. The Nexstar–TEGNA merger, the DirecTV litigation, and the state AGs’ lawsuit are all part of the same story: U.S. infrastructure is concentrating while U.S. demand for differentiated, high‑engagement international IP is rising.

The question for Korea is not whether this is “good” or “bad,” but how to build a K‑content strategy that works under four very different legal scenarios — from a fully unconstrained Nexstar to a partially dismantled one — without waiting years for the courts to finish their work

■ 5-1. Four Scenarios and Their K-Content Implications

The Nexstar–TEGNA merger delivers one unambiguous message: U.S. broadcast concentration is no longer a future risk — it has arrived. Two hundred fifty-nine stations. Eighty percent of American TV households. One company. The physical and commercial channels through which K‑content reaches American audiences have just narrowed dramatically.

Policyband’s “melting ice cube” metaphor applies beyond Nexstar alone: the entire broadcast and pay‑TV ecosystem is structurally eroding under pressure from platforms like Netflix, YouTube, Amazon, and other Big Tech players whose combined market value dwarfs the whole U.S. TV industry. K‑content has ridden this disruption better than most — topping Netflix’s non‑English viewing and, in Omdia’s data, emerging as the most in‑demand non‑English catalog for FAST — but thriving in the gaps of a fragmented market is a very different game from negotiating with a handful of dominant gatekeepers that sit on both local distribution and CTV growth.

In the next phase of the U.S. market, those gatekeepers have names: Nexstar on the consolidated local‑TV and NewsNation/CW side, and Sinclair on the NextGen TV and K‑Channel 82 side. Together, they control much of the spectrum, infrastructure, and product experimentation that will determine how free, ad‑supported television looks in the U.S. over the next decade. For Korean media, the right question is no longer “Is this merger good or bad?” but “Where does K‑content sit on the combined Nexstar–Sinclair rails — and on what terms?”

The answer requires three simultaneous moves: rebuilding negotiation models around super‑groups like Nexstar and Sinclair (plus the major vMVPDs) instead of dozens of local station managers; accelerating K‑FAST and direct‑to‑consumer channels so that Korean IP rides on Samsung TV Plus, LG Channels, Pluto, Tubi and other CTV platforms as a core growth engine, not merely as a by‑product; and treating U.S. regulatory and platform shifts as a shared, industry‑level agenda for KBS, MBC, SBS, MBN, K‑FAST operators, and kobaco, instead of a series of isolated bilateral deals.

For K‑content, “waiting for the dust to settle” is itself the riskiest possible move. By the time Nexstar has fully integrated TEGNA, Sinclair has finished scaling K‑Channel 82, the December 2026 retransmission renegotiation wave has passed, and a new FCC equilibrium has formed, most of the prime windows for influence will have closed — fewer open slots on linear and FAST, tougher standard terms, and far less room to shape how Korean channels and brands are positioned.

The window that matters is the one open now: while Nexstar is still deciding how aggressively to lean into FAST, while Sinclair is using K‑Channel 82 to test what K‑content can do for NextGen TV, and while U.S. platforms are actively searching for high‑engagement, non‑English IP, K‑content has a rare chance not just to “fit into” the restructured U.S. system, but to hard‑wire itself into the core growth story of both Nexstar’s and Sinclair’s next decade.

■ Sources

① Todd Spangler, "Nexstar Claims Its $6.2 Billion Deal for Tegna Has Closed Following DOJ and FCC Approvals — After Eight States, DirecTV Sued to Block It", Variety, March 19, 2026

② Todd Spangler, "Nexstar-Tegna Deal: Eight States File Emergency Motion to Halt 'Disastrous' Merger of Local TV Broadcasters", Variety, March 20, 2026

③ Raquel Calhoun, "DirecTV Files Antitrust Lawsuit to Block $6.2 Billion Nexstar-Tegna Merger", TheWrap, March 19, 2026

④ Ted Hearn, "D.C. Memo: Nexstar-TEGNA Deal Sails Through Carr's FCC in a Speedy 121 Days", Policyband, March 20, 2026

⑤ Jung Han, "미국 방송 지형의 대전환: 넥스타–테그나 62억 달러 합병, 한국 미디어에도 직격탄", K-EnterTech Hub, March 21, 2026 [kentertechhub.com/jemogeobseum-120/]

![[투비]The Stream 2026: When Intention Becomes Attention](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/03/6h3xe4_202603220154.png)

![[SXSW2026]에이미 웹 트렌드 리포트(Convergence

Outlook 2026)](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/03/kty3s8_202603152312.png)

![[보고서]전통 언론사의 크리에이터 전략 대전환](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/02/0nwc9z_202602100212.png)