While Netflix and Disney+ burned billions chasing subscriber growth, Fox Corporation quietly built a different kind of streaming empire — one powered by free, ad-supported, long-form video and live sports. The numbers from its FY2026 second quarter are hard to ignore: Tubi up 27% in total view time, ad revenue up 19%, profitable for two consecutive quarters, and Fox stock the lone winner in a media landscape where every major peer has lost between 30% and 70% of its value over five years. This is the story of how that happened, why the timing matters now, and what it means for the global content industry.

Tubi CEO Anjali Sud speaking at Fast Company interview, 2026. Source: Fast Company YouTube / youtube.com/watch?v=1-RLqZUfqMI

01 The Structural Case for AVOD

The paid streaming era is entering its plateau. Netflix, Disney+, Max, and Peacock have all introduced or expanded advertising tiers — a tacit acknowledgment that the all-subscription model has limits. Meanwhile, the consumers who fueled streaming's first decade of explosive growth are now fragmented across dozens of platforms, suffering from subscription fatigue, and canceling more than they keep. Into this gap steps the ad-supported model, with Tubi as its leading proof of concept.

Jung Han

Jung Han

Two structural forces are simultaneously working in AVOD's favor. On the demand side, advertisers are discovering that AVOD reaches audiences that have simply vanished from linear television. More than 70% of Tubi's user base are cord-cutters or cord-nevers — viewers who have left the traditional cable bundle permanently or never joined it. These are the hard-to-reach, high-value audiences that major brands are willing to pay premium CPMs to access. Fox's Q2 results make this concrete: eight of its top ten advertising categories posted significant growth, led by financial services and insurance.

On the supply side, the economics of free content distribution are increasingly favorable for rights holders. Rather than negotiating one-time SVOD licensing fees, content owners on AVOD platforms participate in ongoing ad revenue sharing — a model that can generate compounding returns as viewership grows. The AVOD flywheel, once it turns fast enough, is difficult to stop.

Tubi reached critical mass in mid-2025, surpassing 100 million monthly active users and posting its first-ever EBITDA profit that fall. By Q2 FY2026, it had recorded its most-streamed quarter in company history, with over 95% of all consumption happening in on-demand — not linear — mode. Annual revenue now exceeds $1.1 billion.

02 Fox’s Contrarian Bet, Now Vindicated

When Fox Corporation divested its entertainment studio to Walt Disney in 2019, the Wall Street consensus was skeptical. The company that remained — built around Fox News, Fox Sports, and a collection of local broadcast stations — lacked an obvious streaming strategy at a moment when streaming was everything.

Fox's answer was methodical and, in retrospect, prescient. In 2020 it acquired Tubi for $440 million — a fraction of what Netflix spends on content in a single quarter — and committed to building a free, ad-supported streaming business rather than launching a competing SVOD service. It kept its live sports and news brands as the anchors of a portfolio built for real-time, appointment viewing. And it watched.

What it watched was competitors spend themselves into structural difficulty. Warner Bros. Discovery, Comcast, Disney, and Paramount all invested heavily in subscription streaming, accumulated massive content costs, and struggled to reach profitability. Their stock prices reflect the journey: every one of them is significantly below its 2021 level.

Fox's FY2026 Q2 results tell a different story. Total company revenue reached $5.18 billion, up 2% year-over-year. Cable — Fox News and Fox Business — delivered $687 million in EBITDA on 7% ad revenue growth and 5% distribution revenue growth. Fox News scatter pricing surged 46 to 47 percent year-over-year. Two hundred new advertisers joined the Fox News platform in a single half. The ad market for live news and live sports, it turns out, was not the sunset business many assumed.

Fox One, the company's new subscription streaming service focused on live sports, launched five months ago and is already exceeding subscriber expectations. About two-thirds of its viewers come for sports; one-third come for news. News viewers watch nearly three times as many minutes per week and engage twice as many days per week compared to non-news viewers — a stickiness metric that augurs well for long-term retention.

03 What Tubi Is — and Isn’t

Understanding Tubi's model requires distinguishing it from two categories it is frequently lumped with: FAST platforms and YouTube.

Tubi vs. FAST

Free Ad-Supported Streaming TV platforms — Pluto TV, Samsung TV Plus, LG Channels — are primarily organized around linearly programmed channels. They are, in essence, digital cable without the subscription. Tubi is built differently. More than 95% of its consumption happens on-demand: viewers actively choose a title, queue it, and watch it start to finish. Tubi CEO Anjali Sud calls this “intentional viewing” and argues that it fundamentally changes the advertising value proposition. A viewer who chooses to watch a specific show is more engaged, more attentive, and more receptive to advertising than one who left a channel on in the background. That difference shows up in CPM rates.

Tubi vs. YouTube

Scale is where the comparison to YouTube is most apt — both are free, ad-supported, and reaching hundreds of millions of users. But Tubi does not allow user-generated content and has stated that policy will not change. Every title on the platform has been curated: professionally produced content from Hollywood studios, or creator-originated content that has been selected and, in some cases, developed specifically for the platform. The result is a brand-safe programming environment that advertisers trust and that justifies premium rates.

Tubi's current library exceeds 300,000 movie and TV titles, including nearly 400 originals. It has produced those originals not with Netflix-scale budgets but with a discipline that keeps unit economics healthy — “about 400 original movies” at a cost structure that works.

The short-form question

Tubi has drawn a firm line against short-form content feeds. Its recent TikTok partnership is specifically designed not to import short clips into the platform but to identify TikTok creators capable of making the transition to long-form — full-length series, produced to premium TV standards. “We are not getting into shorts. We are committed to long-form,” Sud said at a Paley Center event in New York last week.

This is the kind of decision that is easy to second-guess in a content environment where short-form is everywhere. It is also the kind of decision that, if it holds, will define Tubi's positioning for the next decade. Sud acknowledged as much in her Fast Company interview: the least popular decisions are often the ones a leader has to make.

FOX + TUBI | KEY METRICS SNAPSHOT | FY2026 Q2

Sources: Fox Corporation FY2026 Q2 Earnings Call, Feb. 4, 2026 · StreamTV Insider, Mar. 30, 2026 · Axios

04 Building a Creator Economy — Without the Hype Cycle

Fox has not entirely avoided the creator economy. It has just approached it differently from the platforms that have thrown money at influencer deals with little strategic logic.

Tubi began its creator content push roughly eight months ago. It now hosts more than 16,000 creator episodes and counts about 10% of its viewers consuming that content. The strategy is not to turn Tubi into a YouTube alternative — it is to bring the best storytellers from the creator world into long-form, premium TV formats. Tubi selects and, in some cases, develops creator-originated content. It signs deals with established production companies, including Kevin Hart's Hartbeat, and works with platforms like TikTok to identify creators who have the storytelling depth to translate from short-form social video to 30-or-60-minute narratives.

Red Seat Ventures, acquired by Fox roughly a year ago, runs the inverse operation. While Tubi brings digital-native creators into Hollywood-style production, Red Seat helps established television personalities — former Fox News anchors, cable TV hosts — build creator-economy businesses: video podcasts, live events, subscriber communities, DTC media brands. Clients include Megyn Kelly and Bill O'Reilly, among others.

The two efforts create an ecosystem that covers both ends of the creator spectrum, with Tubi's 100 million monthly users as the distribution layer underneath. The early evidence of cross-platform synergy: Crime Junkie, a Red Seat Ventures podcast client that is now one of the most listened-to true crime shows in the country, has been made available on Tubi — extending its reach into the connected TV environment where Tubi's audience lives.

05 Wall Street’s Verdict

The stock chart says what the strategy documents only imply.

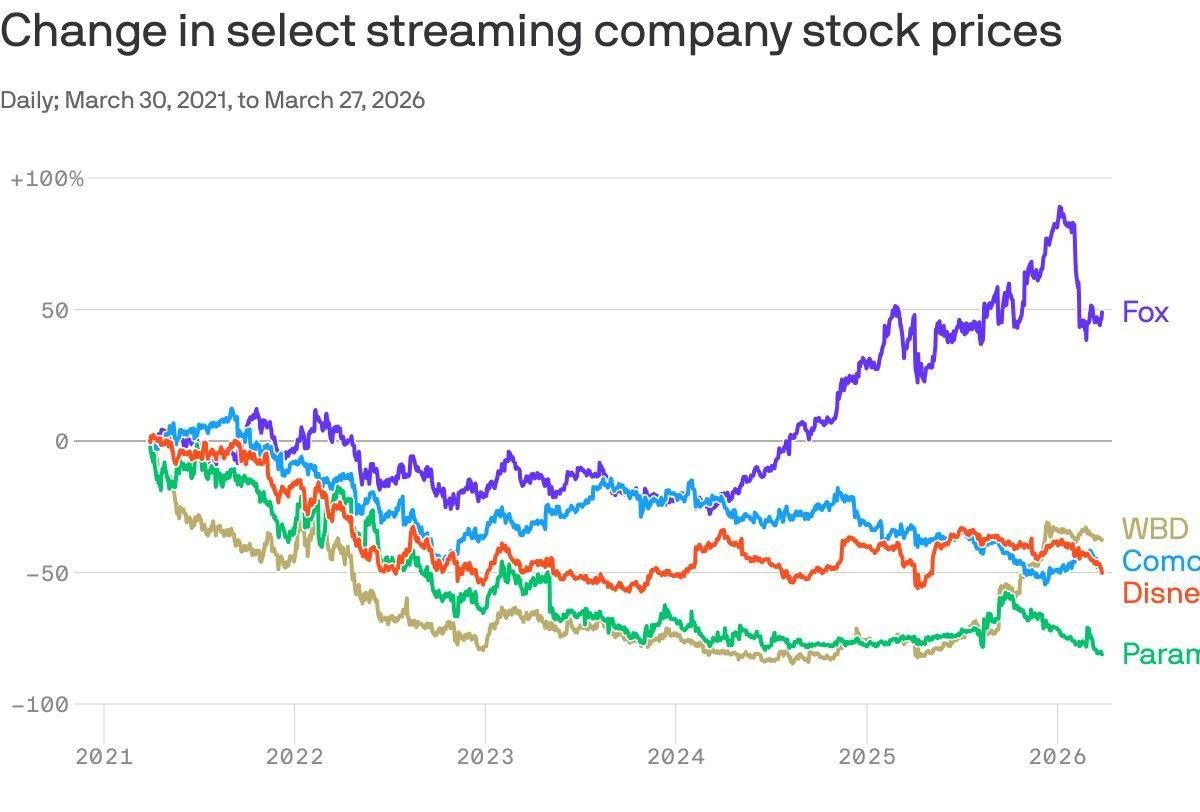

Streaming company stock price change, daily, March 30, 2021 to March 27, 2026. Source: Financial Modeling Prep / Chart: Axios

Over the past five years, Warner Bros. Discovery, Comcast, Disney, and Paramount have each lost between 30% and 75% of their market value. Fox has gained more than 50%. The divergence is not a coincidence — it is the market pricing in the structural difference between a business model built for the next phase of media and one still adjusting to the last phase.

The underlying financial data supports the read. While peers collectively declined at roughly a 4% compound annual rate in advertising revenue over the past four to five years, Fox grew at approximately 8% per year — including streaming. Fox News alone achieved its highest advertising revenue in company history in the first half of FY2026. Tubi set records for quarterly, weekly, and daily ad revenue simultaneously. Fox Sports set records for NFL regular season, postseason, and college football advertising.

Capital allocation tells the same story. Since launching its buyback program in 2019, Fox has returned $8.4 billion to shareholders — approximately 35% of all shares outstanding — through repurchases, with an additional $1.5 billion accelerated share repurchase currently underway. Total shareholder returns including dividends have now crossed $10.4 billion since the company's establishment.

06 Risks Worth Watching

The Fox model is not without structural vulnerabilities, and the investment community has begun pricing in some of them.

NFL Rights Dependency

NFL programming is the gravitational center of Fox Sports, driving record advertising revenue and delivering the live event reach that premium brands pay to access. But the NFL's current rights agreement includes an option to renegotiate, and any renewal is expected to carry a significant cost increase. Murdoch acknowledged the variable without offering specifics, noting that Fox views its sports portfolio holistically and will rebalance as needed. The company's FanDuel option and Flutter stake — worth a combined $2.8 billion at current buy-side valuations — provide one form of hedge, as growing sports betting and prediction market advertising revenue could offset higher rights costs.

Political Ad Cycle Volatility

Fox's local station group is the primary beneficiary of political advertising, and political ad cycles are inherently lumpy. The current midterm cycle should be a tailwind, but the concentration of political revenue in off-years introduces quarterly volatility. Nationally, Fox News is positioning to capture an increasing share of national political advertising — particularly given Murdoch's claim that Fox News now leads in viewership among Republican, Democratic, and Independent audiences alike — but local remains the bigger variable.

Fox One Subscriber Seasonality

Fox One launched on the strength of an NFL season. As the league's schedule concludes, management has acknowledged potential subscriber softness and is actively promoting upcoming sports events — Daytona 500, Indy 500, the start of MLB season, and FIFA World Cup — to retain subscribers through the spring. Whether the platform's news audience alone is sufficient to hold subscribers in the sports off-season remains an open question.

07 Why Now — The Optimal Entry Window

Three converging structural factors make 2026 the most compelling entry point the AVOD market has offered — for content partners, distributors, and international players looking to establish a foothold in the U.S. streaming ecosystem.

Implications for Korean Content Companies

The Fox-Tubi model has specific and actionable implications for Korean content companies seeking to expand their presence in the U.S. market. Three strategic priorities stand out.

First, AVOD content partnerships generate superior advertising value compared to FAST channel distribution. The distinction Anjali Sud draws between intentional on-demand viewing and passive FAST channel consumption maps directly to CPM premium — and Korean content's defining characteristic is exactly the kind of passionate, genre-specific fandom that AVOD platforms are engineered to serve. K-drama, K-horror, K-crime thriller, and K-romance already overlap with Tubi's highest-performing genre categories. The strategic recommendation is not to open a FAST channel — it is to negotiate a content supply agreement or, better, a co-development arrangement on the AVOD side, where ongoing ad revenue sharing and deeper audience data flow back to the Korean content partner.

Second, the long-form creator pipeline is a direct and underutilized onramp for Korean creators with established social media audiences. Tubi's TikTok partnership is a replicable framework: the platform identifies creators with proven audience engagement on short-form platforms, then develops long-form original series with them. Korean creators with millions of followers on YouTube or TikTok — especially those whose content indexes on K-culture, language learning, food, travel, or entertainment commentary — are exactly the profiles Tubi is looking for. The entry barrier is lower than at any traditional network, and the upside is a long-form original credit on a platform with 100 million monthly users.

Third, Korean broadcasters and content distributors need to structurally shift from one-time SVOD licensing fees toward ongoing AVOD revenue share arrangements. The flat-fee model undervalues content whose audience compounds over time. Networks including YTN and MBN, and entertainment companies including CJ ENM, JTBC, and KBS Media, should be negotiating multi-title supply agreements with Tubi, Peacock, Pluto TV, and Samsung TV Plus that include revenue participation, audience data sharing, and — in the most ambitious cases — co-original production commitments. The K-content times Tubi original format represents the frontier of what this partnership model can produce.

The Bottom Line

Fox Corporation did not win the streaming wars. It declined to enter them. What it built instead — a free, ad-supported, long-form streaming platform engineered around intentional viewing and fandom discovery, anchored by live sports and news, now expanding into the creator economy — is turning out to be the more durable business model.

Tubi's flywheel has crossed into genuine profitability and scale. Fox One has added a live subscription layer that extends the portfolio without cannibalizing the core. The advertising market for Fox's properties is the strongest in the company's history. And the stock price, relative to every major peer, has made the argument that Wall Street has noticed.

The least popular decision, as Anjali Sud reminded her Fast Company audience, is often the one the leader has to make. Ten years of unglamorous execution on a “very unexciting” strategy just produced the media industry's most interesting stock chart. The window it created for international content partners — Korean content companies above all — will not stay open indefinitely.

Sources: Fox Corporation FY2026 Q2 Earnings Call Transcript (Feb. 4, 2026) · StreamTV Insider (Mar. 30, 2026) · Axios · Fast Company YouTube interview with Anjali Sud · Stock data: Financial Modeling Prep · Nielsen Gauge U.S. tracker

This report was prepared by K-EnterTech Hub for informational and educational purposes. It does not constitute investment advice.