$187 billion of deals in motion, led by Paramount-WBD ($110B) — but the leverage on stage has shifted from media moguls to tech chiefs. Buyer consolidation redraws the negotiating map for K-content.

Global media's realignment is converging on a Big Tech Entertainment order. The Sun Valley conference opened July 7 with roughly $187 billion of transactions in motion at once — Paramount's $110 billion merger with Warner Bros. Discovery (WBD), Fox's $22 billion acquisition of Roku, and the $55 billion buyout of Electronic Arts — while Comcast's planned spin-off of NBCUniversal and Sky adds two fresh for-sale assets to the board.

Jung Han

Jung Han

Yet the power to design the board has shifted away from the companies that make content, toward the tech players holding the distribution gateways, the AI infrastructure and the capital. Korea's content industry is a direct stakeholder in this realignment: the number and identity of the global buyers of K-drama and K-variety rights will change in the order these deals close.

The consolidation is structural. With subscriber growth stalled and content costs still rising, the scale threshold for standalone survival has climbed, and as FAST/AVOD advertising and AI production capability become the industry's new profit engines, operators lacking both scale and technology are pushed onto the target list.

Sun Valley, Idaho. Photo: Sun Valley Resort

The Sun Valley conference is an invitation-only retreat that Allen & Co., a family-owned boutique investment bank in New York, has hosted every July at Idaho's Sun Valley Resort since 1983. What began with 35 guests and a single speaker has grown into the 'billionaires' summer camp' — hundreds of chiefs across media, tech, finance and sports, with no public sessions, no official guest list and minimal press access — where the Disney-ABC merger (1995) and Jeff Bezos's purchase of the Washington Post (2013) were hatched on hiking trails and at dinner tables.

This year's edition runs July 7–11. Fortune notes that the event, born as a media-finance gathering, has seen its center of gravity shift after four decades from media moguls to tech leaders: the media chiefs are still in the room, but the leverage belongs to the people building the technology that is remaking their industry.

Sun Valley sits in the mountains of central Idaho, near the Sawtooth National Forest. Map: Google Maps

The event's scale shows up first on the tarmac. Per Business Insider, Friedman Memorial Airport expects 300–350 aircraft movements a day during the conference — more than four times the norm. Airport director Tim Burke says the field can park roughly 100 to 125 business jets; beyond that, arriving aircraft drop passengers and reposition to other airports.

For one week, global capital converges on a resort town of fewer than 1,800 full-time residents. Charter and fractional operators such as NetJets, Flexjet and Vista dominate the ramp, a pattern attributed to privacy concerns over jet tracking.

Private jets on approach to Sun Valley's Friedman Memorial Airport. Source: flight-tracking service

Who Is Allen & Co.: Relationship Banking Born of Columbia Pictures

The host, Allen & Company, is a privately held boutique investment bank at 711 Fifth Avenue, New York, founded in 1922 by Charles Robert Allen, Jr. and soon joined by his brothers Herbert A. Allen, Sr. and Harold Allen. The firm specializes in real estate, technology, media and entertainment, and keeps an extreme low profile: no website, no press releases. Since 2002 it has been run by Herbert Allen III, the founder's grandnephew. Its entertainment ties trace to a 1973 stake in Columbia Pictures, sold to Coca-Cola in 1982 at a significant profit, after which Herbert Allen, Jr. joined Coca-Cola's board.

The reason the conference exists flows from the same business model. The firm's stated aim is long-term, lucrative relationships with a small circle of exclusive clients, and Sun Valley was designed as the device that binds the bank to the moguls running America's newspapers, studios and broadcast networks.

Those relationships have converted into mandates: a spot in the Google IPO underwriting syndicate (2004), sole advisor on Activision's $18 billion merger with Vivendi Games (2007), Twitter IPO underwriter (2013), advisor to Facebook on its $19 billion WhatsApp acquisition (2014), advisor on the $80 billion Time Warner Cable-Charter merger (2015), and lead advisor to Time Warner on its $108 billion acquisition by AT&T (2016). Allen also advised on Verizon's purchases of AOL (2015) and Yahoo (2016) — meaning the advisory fees on the very transactions Lang cites as failures went to Allen as well.

Deal Board: Paramount-WBD Races a Sept. 30 Clock

Per TheWrap, Variety and Forbes, this year's roster includes Meta's Mark Zuckerberg, Amazon's Jeff Bezos, new Disney CEO Josh D'Amaro, Paramount's David Ellison, Comcast's Brian Roberts, OpenAI's Sam Altman and Greg Brockman, Apple's Tim Cook and incoming CEO John Ternus, Palantir's Alex Karp and Bill Gates.

Fox's Lachlan Murdoch is joined on the list by his father Rupert Murdoch, and Anthropic CEO Dario Amodei is reported to be on this year's guest list. On the sports and entertainment side, NFL commissioner Roger Goodell, Live Nation CEO Michael Rapino and Mattel CEO Ynon Kreiz were also confirmed on site. Notably absent from this year's list: longtime regulars Warren Buffett and successor Greg Abel, Elon Musk, Nvidia's Jensen Huang, Larry Ellison and Shari Redstone.

Meta CEO Mark Zuckerberg. Photo: Meta

From Korea, Samsung Electronics Chairman Lee Jae-yong (이재용) entered the Sun Valley Resort on opening day, July 7, accompanied by Han Jin-man (한진만), president of Samsung's Foundry Business Division, per the Chosun Ilbo. Bringing the foundry chief reads as a play for AI-chip demand and contract-manufacturing relationships with the Big Tech leaders assembled on site — Apple, Amazon and OpenAI among them — and the timing is pointed, coming just as Apple sealed its $30 billion US-made chip agreement with Broadcom.

Bloomberg's 'Emerging' podcast, released July 9, frames AI as the new measure of global power, built on chips and the infrastructure that runs them — and examines India's sovereignty dilemma as a country with talent and data but without frontier models or large-scale compute. By that yardstick, Korea's grip on semiconductor manufacturing puts it in a comparatively strong position. Worth noting, though: Korea's Sun Valley presence this year runs through the semiconductor-infrastructure axis. No Korean content or media company has a seat at this deal table yet.

The scenery around the venue follows the annual pattern. Invited journalists — Gayle King, Anderson Cooper, Andrew Ross Sorkin, Bret Baier, Thomas Friedman — attend not to report but to moderate the morning sessions. Elder statesmen such as former Disney CEO Michael Eisner and former Meta COO Sheryl Sandberg remain fixtures. Outside the resort perimeter, local activists staged rallies framed around economic inequality and corporate accountability — the other annual ritual of a week in which global capital converges on a town of fewer than 1,800 residents.

The headline transaction, Paramount-WBD, targets a close by the end of Q3. WBD CEO David Zaslav and CFO Gunnar Wiedenfels — who fielded bids from Comcast, Netflix and Paramount — held court on site again this year.

Regulatory review remains open in Europe and the UK, and Oregon AG Dan Rayfield said Tuesday he will seek a court order delaying the deal at least 60 days pending a records dispute. Under the deal terms, WBD shareholders collect a 25-cent-per-share quarterly ticking fee if the transaction is not closed by September 30; a regulatory collapse triggers a $7 billion termination fee payable by Paramount. If the merger closes, CNN is widely expected to pass to the Ellison family.

Warner Bros. Discovery CEO David Zaslav. Photo: WBD

Paramount chairman and CEO David Ellison (left) with Tom Cruise. Photo: Paramount

Comcast co-CEOs Brian Roberts and Mike Cavanagh arrived days after announcing the NBCUniversal-Sky spin-off. Both deny the split is a prelude to selling NBCUniversal, emphasizing they will 'build and invest for growth' — but with Comcast retaining at most a 19.9% stake for at least one year after separation, Wall Street's sale speculation persists. The NBCU spin-off is Comcast's second restructuring this year, following January's separation of cable networks (USA, CNBC, MSNBC and others) and digital assets (Fandango, Rotten Tomatoes) into Versant, led by Mark Lazarus.

Netflix, Fox, Diller: The Follow-On Deal Lineup

Netflix bid $83 billion for WBD's studio and streaming assets before declining to match Paramount's $110 billion. With co-CEOs Ted Sarandos and Greg Peters and CFO Spencer Neumann on site, the Street has floated Lionsgate, Imax and Roku as follow-on targets; the company denies interest in each while conceding the bidding war built out its 'M&A muscle' and leaving the door open to acquisitions aligned with long-term goals.

Co-founder Reed Hastings, who left the board after June's annual meeting, attended separately. In an on-site broadcast panel (July 11), industry reporters framed WBD as the fulcrum asset that moved the whole board: Paramount's win reset the chessboard, the Comcast split effectively hung for-sale signs on both the media and cable units, and Netflix remains on the hunt for a studio asset. With each completed deal, the number of remaining combinations shrinks — a game of musical chairs that raises, rather than relieves, the pressure on every player to move.

Fox CEO Lachlan Murdoch's Roku acquisition is slated to close in H1 2027. Fox previously acquired Red Seat Ventures in 2025 and has expanded into creator subscriptions via Supercast; Roku gives it the distribution backbone for its streaming and advertising businesses. Barry Diller's People Incorporated (formerly IAC), which holds 26.1% of MGM Resorts International, has proposed taking out the remainder at $48.30 per share — an $18 billion transaction. Diller has also been open about his interest in CNN should it ever come up for sale. Michael Ovitz attended just after UMG's board rejected Bill Ackman's Pershing Square-led $64 billion takeover, under which Ovitz would have chaired UMG's board.

Fox Corporation executive chairman and CEO Lachlan Murdoch. Photo: Fox

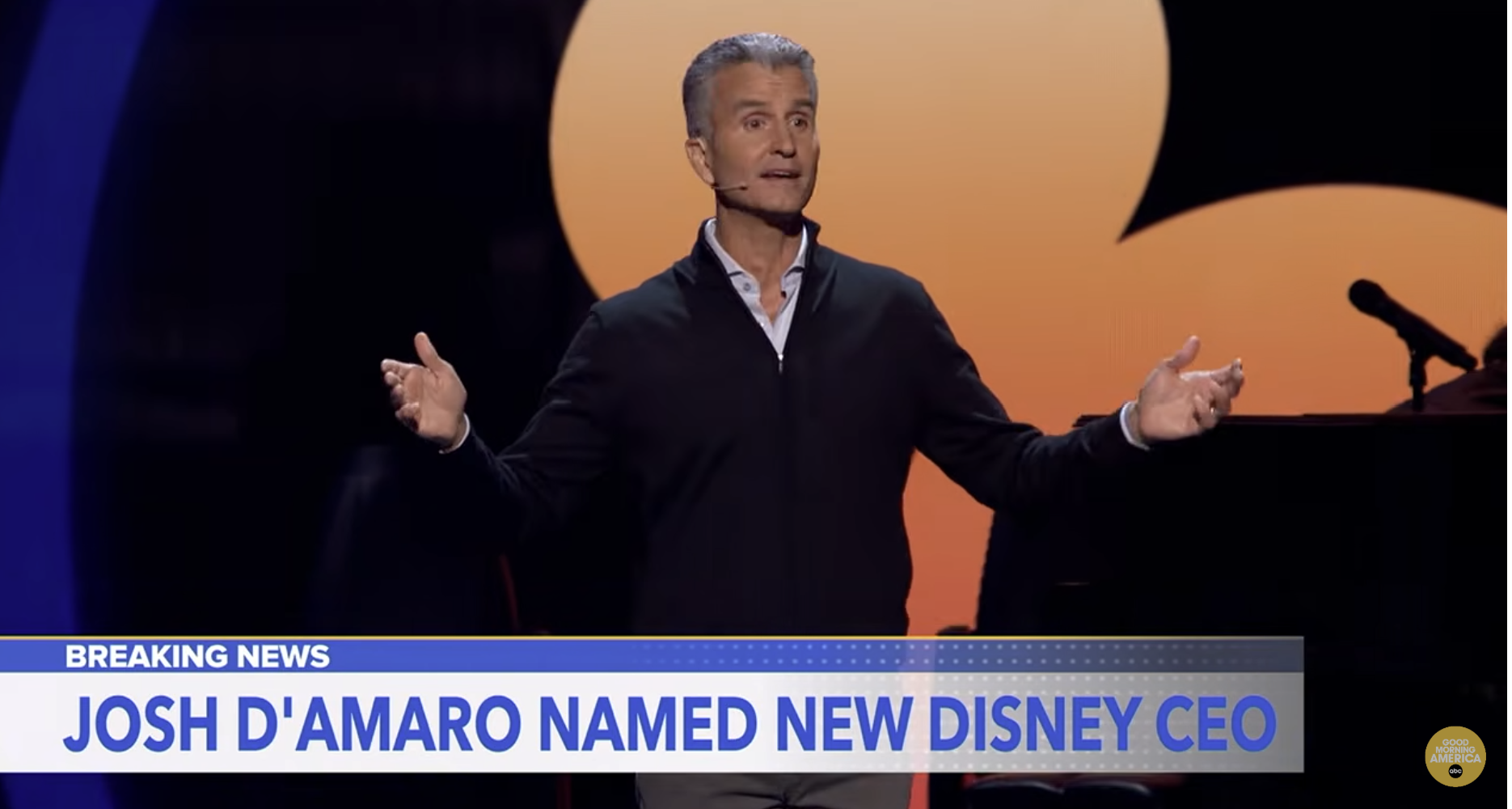

Big Tech and AI: What the $1B Disney-OpenAI Collapse Leaves Behind

Disney's $1 billion Sora character-licensing agreement with OpenAI died with OpenAI's decision to shut the service down. D'Amaro, appearing alongside predecessor Bob Iger, reiterated Disney's position that it will keep engaging AI platforms on terms that respect IP and creators' rights, while CFO Hugh Johnston waved off large-scale M&A, saying the company likes the hand it holds. OpenAI, for its part, acquired Python tooling developer Astral in March and tech talk show TBPN in April, after its roughly $6.5 billion 2025 purchase of Jony Ive's AI devices startup io.

New Disney CEO Josh D'Amaro. Photo: ABC 'Good Morning America'

Netflix took the opposite route on AI, acquiring Ben Affleck's startup InterPositive for up to $600 million to internalize the technology in its production pipeline. Apple's Tim Cook joined the conference less than 24 hours after signing a $30 billion agreement with Broadcom to produce 15 billion US-made chips through 2031; Apple has also bolstered its content-creation stack this year with plugins maker MotionVFX (March) and Israeli AI audio startup Q.ai (January). Amazon closed an $11.57 billion acquisition of GlobalStar to scale Project Kuiper, while Amazon MGM Studios dropped Luca Guadagnino's Sam Altman film 'Artificial,' since picked up by Neon.

Apple CEO Tim Cook. Photo: Apple

On the Stage: Bezos's Space Data Centers, Nadella's AI Appeal

Part of the closed-door morning programming surfaced via Puck's Dylan Byers. Taking the stage Wednesday in conversation with Marc Andreessen, Jeff Bezos laid out a vision of gigawatt-scale data centers in space and on the moon — facilities running on constant solar power, free of terrestrial constraints on electricity, water and real estate, which he framed as the reason he and Elon Musk have poured resources into getting to space. As the physical limits on building data centers and manufacturing GPUs become tangible, Byers observed, the economics of the space business are being repriced. The same morning, Microsoft CEO Satya Nadella closed his AI conversation with Reid Hoffman by appealing to fellow executives to respect the public's fears about the disruptive power of these technologies. If AI dominated every conversation and meeting at last year's retreat — Flowcode CEO Tim Armstrong likened it to a thousand-pound gorilla — this year the chatter is expected to center on AI costs and return on investment.

Meta CEO Mark Zuckerberg (left) and COO Javier Olivan walk the Sun Valley grounds under the banner 'Artificial intelligence dominates this year's private agenda.' Photo: Firstpost America via YouTube

Amazon executive chairman Jeff Bezos. Photo: Amazon

Byers also argued that the very notion of Sun Valley as a media deal summit has grown outdated: the media executives look more subordinate each year to the tech chiefs redefining what media is. On the ground, the Comcast split was shrugged off as an inevitable step in Hollywood's long slide, and chatter about NBCU acquiring studios or game companies was dismissed on affordability grounds. The event's real function is bilateral meetings. Last year, Apple's Tim Cook and Eddy Cue closed out their capture of Formula One rights from ESPN here; this year, Roberts and his new executive team of Michael Angelakis and Cavanagh were expected to make the rounds with prospective partners including Disney and Netflix. Amazon CEO Andy Jassy's dinner in Ketchum with Robert Kraft — Patriots owner and chair of the NFL's media committee — was read as a possible prelude to expanding the Amazon-NFL relationship. Deals are conceived and executed over months, Byers concluded; the conference's value is simply the convenience of having everyone in the same place at the same time.

Platforms, Sports, Gaming: YouTube's TV Grip and the $55B EA Buyout

YouTube CEO Neal Mohan's presence draws attention without any large-scale M&A. The platform continues to lead Nielsen's monthly Gauge measurement of TV viewing time, has added Peacock, HBO Max, Paramount+ and Fox One to Primetime Channels, and has unveiled plans for 10 skinny bundles across sports, news and entertainment. The market is increasingly steered not by whoever buys content, but by whoever controls the distribution gateway.

In gaming, Jared Kushner's Affinity Partners is leading a $55 billion take-private of Electronic Arts with Silver Lake and Saudi Arabia's Public Investment Fund; Affinity was earlier involved in financing Paramount's WBD bid before dropping out. Former Activision Blizzard CEO Bobby Kotick, who steered the $69 billion sale to Microsoft, also attended — as Microsoft's Xbox restructuring cuts 4,800 jobs and moves four gaming studios under new management. In sports, MLB commissioner Rob Manfred arrived having closed three-year rights deals with ESPN, Netflix and NBCUniversal covering 2026–2028, joined by NBA commissioner Adam Silver, who brokered 11-year deals with Disney, NBCUniversal and Amazon, and PGA Tour CEO Brian Rolapp.

NFL commissioner Roger Goodell. Photo: NFL

Sony Pictures Entertainment CEO Ravi Ahuja landed fresh off a $100 million minority investment in immersive entertainment company Cosm. Sony this year moved its home entertainment hardware business into a joint venture with TCL, struck a global pay-1 licensing deal with Netflix, and closed a $457 million majority stake in 'Peanuts.' CBS News editor-in-chief Bari Weiss, now under the Paramount umbrella, was also on site — Ellison's Paramount bought her Free Press for $150 million, in a deal whose first conversation took place at last year's Sun Valley.

The Sun Valley Discount: NBCU, From Acquisition to Spin-Off in 15 Years

Deal heat aside, the track record of Sun Valley-born mergers is poor. In a July 7 column, Variety's Brent Lang noted that transactions incubated here — Time Warner-AOL, Yahoo's sale to Verizon — ended in shareholder-value destruction, and that Comcast's purchase of NBCUniversal, itself a Sun Valley deal, is now being unwound through this month's spin-off announcement, fifteen years on. Allen & Co. collects advisory fees regardless of outcome; the reliable winners in M&A, Lang writes, are the lawyers and the banks. His diagnosis that executives flock to Idaho out of fear of missing the transformative, legacy-cementing merger — and his conclusion that history suggests the best deal may be the one left unmade — collide head-on with a season of $110 billion mergers and $55 billion buyouts. For content suppliers sitting across the table from newly merged buyers, post-close debt loads and integration risk are contract variables, not footnotes.

Korea Impact I: Buyer Consolidation Forces a Rate-Card Recalculation

Once Paramount-WBD closes, the content acquisition organizations behind HBO Max and Paramount+ merge. Two buyers that until now bid against each other for global K-content rights become one — a near-term drag on Korean producers' pricing leverage. The offset: the combined entity needs a proven non-English library at scale to stand up a third pillar against Netflix and Disney, and K-content sits at the top of that category. Volume packaging deals and original co-production slots are likely to expand, not contract.

The risk sits in post-merger finances. As Time Warner-AOL showed, when a merged buyer comes under debt and integration-cost pressure, content budgets are the first line adjusted. Korean sellers should structure deal terms — duration, minimum guarantees — to separate the 12–18 month post-close window for large deals from the cost-cutting phase that can follow. Capital allocation at Netflix, the largest single investor in Korean content, is the other swing factor: a major acquisition could recalibrate regional originals budgets, while a no-deal path would likely keep K-content spend intact. The Sony-Netflix pay-1 arrangement also offers Korean studios a reference model as long-term studio-streamer supply deals proliferate.

Korea Impact II: Roku Under Fox Changes FAST Carriage Math

Fox-Roku confirms that FAST distribution is vertically integrating. Roku has been the gateway platform to the US connected-TV market and a primary on-ramp for Korean FAST channels. Under Fox ownership, channel placement priority, ad-inventory allocation and revenue-share terms can be rebalanced toward Fox-affiliated content — Korean FAST operators should prepare for term changes at carriage renewal. With YouTube consolidating its gateway position through Primetime Channels and skinny bundles, the structural answer is to shift from simple carriage to equity-participation or revenue-sharing partnerships as distribution gateways become house assets of individual media groups.

In Europe, the Comcast spin-off and Sky's $2.1 billion acquisition of ITV's Media & Entertainment unit are combining into an integrated UK/European broadcast-streaming platform. The post-spin NBCU-Sky entity must prove growth as an independent company, and K-content — high viewing performance at comparatively low acquisition cost — is a natural scheduling-expansion candidate. This is the window in which Korea's European distribution can diversify beyond the Netflix-centric route.

Korea Impact III: AI Licensing Clauses Get a Higher Baseline

The Disney-OpenAI collapse is a direct reference case for K-IP holders negotiating with AI platforms. If the world's largest IP company could not secure service continuity and control, contracts covering K-pop, K-drama and webtoon IP will need explicit terms on IP handling at service termination, training-data usage scope and penalty structures as standard. The pattern of platforms and studios buying AI production capability outright — Netflix's InterPositive, Apple's MotionVFX and Q.ai — pulls forward the build-versus-license decision for Korean production companies.

Sony's moves — the Cosm stake, the Peanuts IP purchase, the TCL hardware JV — sketch a model built on IP equity and technology partnerships rather than finished-program sales. It maps onto the direction Korea's content export structure needs to travel.

Outlook

The direction Sun Valley points to is a media industry converging on a Big Tech Entertainment order: those holding the distribution gateways (YouTube, Roku), the AI infrastructure (OpenAI, Microsoft, Apple) and the large-scale capital (Saudi Arabia's PIF, private equity) design the board, while traditional media companies are being repositioned on top of it as IP and content suppliers. Neither the $187 billion deal board nor the on-stage agenda strayed from that direction.

The pace of follow-on dealmaking hinges on whether Paramount-WBD closes on schedule. With the September 30 deadline, the $7 billion break fee and state AG action all in play, an on-time close sets off the next chain — the disposition of CNN and Netflix's next move first among them.

For Korea's content industry, the window before the buyer landscape hardens is the moment to lock in post-consolidation partnership lines; pricing Sun Valley's forty-year deal record — the integration-failure risk — into contract terms is the precondition. As Chairman Lee's attendance shows, Korea's entry point to Sun Valley currently runs through semiconductors and infrastructure. For the content and IP side to reach this deal table, the ticket is a different one: equity and co-production partnerships with the global media groups now consolidating.

Sources

· Lucas Manfredi, “Sun Valley 2026: Which Hollywood and Tech Moguls Made the Retreat?”, TheWrap, July 8, 2026 — attendees and deal facts.

· Brent Lang, “Buyer Beware: Why Sun Valley Has Been a Disaster for the Media Business”, Variety, July 7, 2026 (variety.com/2026/biz/news/sun-valley-conference-destroy-media-business-deals-1236803178) — Sun Valley deal track record; expected attendees.

· Related TheWrap coverage: Sky-ITV $2.1B acquisition / Oregon AG 60-day delay request / Fox-Roku analysis.

· “The billionaires' 'summer camp' that media moguls built is now run by the tech titans trying to replace them”, Fortune, July 8, 2026 — 1983 origins, media-to-tech power shift, absentee list.

· Jim Dobson, “Sun Valley's Billionaire Summer Camp Returns”, Forbes, July 6, 2026 (updated July 10) — Karp, Brockman, Goodell, Rapino, Kreiz confirmed on site / The Hollywood Reporter attendee tally (July 7–11 dates) / BoiseDev, July 7, 2026 — Disney-ABC (1995) and Bezos-Washington Post (2013) deal history.

· The Chosunilbo (English edition), “Samsung Electronics Chairman Lee Jae-yong Attends Sun Valley Conference”, July 9, 2026 — Lee Jae-yong and Han Jin-man attendance confirmed.

· Dylan Byers, “Seen & Being Seen in Sun Valley”, Puck, July 8, 2026 — Bezos-Andreessen and Nadella-Hoffman sessions; Roberts meetings with Disney/Netflix; Jassy-Kraft dinner; Apple's F1 rights history.

· On-site broadcast panel transcript, “Media Industry Deal Analysis”, July 11, 2026 (obtained by the author) — WBD as fulcrum asset; two for-sale signs at Comcast; Netflix's studio hunt.

· Bloomberg podcast “Emerging: Can India Catch Up in the AI Race?”, July 9, 2026 (bloomberg.com/news/videos/2026-07-09/can-india-catch-up-in-the-ai-race-video) — AI as a chips-and-infrastructure measure of national power; India's AI sovereignty dilemma.

· Madeline Berg, “Private jets descend on Sun Valley's invite-only summer camp for billionaires”, Business Insider, July 7, 2026 — 300-350 daily aircraft movements, 100-125 jet parking cap, sub-1,800 population, Amodei guest-list report, Greg Peters and Rupert Murdoch expected.

· Wikipedia, “Allen & Company” — firm history, Columbia Pictures stake and sale, advisory track record (Google, Activision, WhatsApp, Time Warner and others).

· Korea impact analysis is the author's interpretation based on the reported facts above.