'K팝 데몬 헌터스', 아카데미 장편 애니메이션상 수상… "이것은 한국과 전 세계 한국인을 위한 것"

by

2026년 3월 15일

Politicized antitrust, Hollywood megamergers, and Big Tech's AI ad dominance are reshaping the US media landscape — with direct consequences for Korea's content industry, negotiating leverage, and revenue models.

March 5, 2026. A White House conference room. Just five days into the Department of Justice's antitrust trial against Live Nation, CEO Michael Rapino and Attorney General Pam Bondi sat across the same table. By the end of that meeting, a settlement agreement had been signed. The DOJ's lead trial attorney told the judge he had only seen the term sheet that morning. It was a scene that encapsulated a new era in US antitrust: not the law regulating corporations, but political connections determining corporate fate.

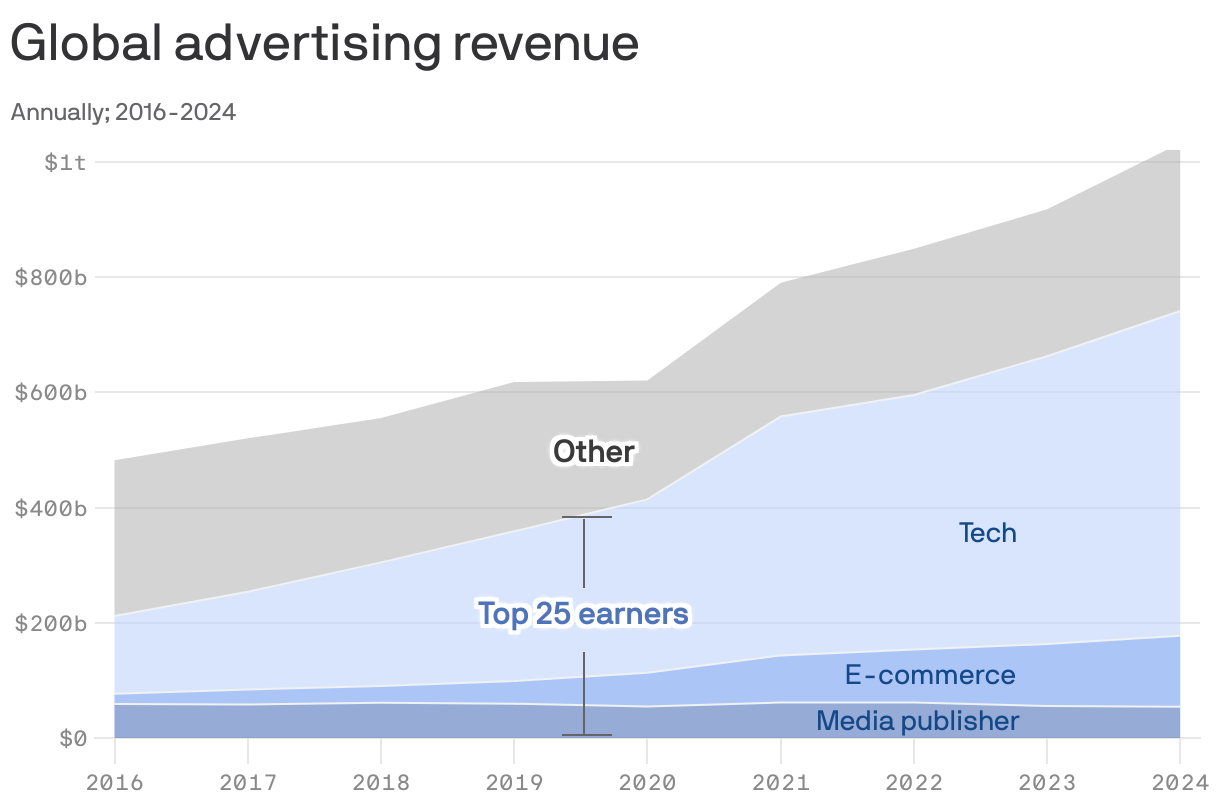

That scene is just one episode of a sweeping structural transformation playing out simultaneously across the US media industry. Hollywood is executing its third studio megamerger in six years. Local broadcasters are racing to consolidate under a permissive FCC. Google, Meta, and Amazon are deploying AI to monopolize advertising revenue, crowding out traditional media publishers. WPP Media data captures the shift in stark numbers: media publishers' share of top-25 advertising revenues has collapsed from 27.84% in 2016 to just 7.3% in 2024 — a fourfold decline in eight years.

Jung Han

Jung Han

For Korea's media and entertainment industry, these are not distant US-market developments. The negotiating landscape for K-pop concerts, K-drama IP deals, Korean broadcasters' advertising revenue, and FAST channel distribution — all of it is shifting beneath the industry's feet. This report maps the transformation sector by sector, and draws out the strategic implications for Korean players.

▣ Table 1. US Major Media M&A and Antitrust Cases (2025–2026)

Behind the scenes of US antitrust enforcement, no figure has attracted more scrutiny than attorney Mike Davis, 48. The Wall Street Journal, drawing on interviews with more than three dozen DOJ employees, lobbyists and lawyers, reported that Davis pressured antitrust officials to approve his clients' deals — and went over their heads when they refused. He describes himself as 'the best fixer in Washington, period. Full stop.'

Davis clerked for Supreme Court Justice Neil Gorsuch and helped shepherd his 2017 confirmation. He became one of Trump's most visible public defenders following the Mar-a-Lago search in 2022, claiming more than 5,000 media appearances on the president's behalf. He speaks frequently with Trump, according to aides, and is close to Deputy Attorney General Todd Blanche and Associate Attorney General Stanley Woodward. His retainer: as much as $300,000 per month, plus seven-figure deal fees.

▣ Table 2. Mike Davis — Client Outcomes at the DOJ

Former DOJ enforcers say antitrust work was largely insulated from day-to-day political interference even in Trump's first term, with top leadership intervening at most once or twice over four years. That buffer is gone. 'You would never want to be seen holding the knife,' William Kovacic, Bush-appointed FTC chair, told the Journal. 'In previous administrations... that was the norm.' The DOJ spokesman maintained all settlements 'are based on the merits.'

A senior DOJ official told Axios plainly: 'The big thing is: We're not the Biden administration. We're willing to bring cases. But we're also not afraid to settle. I don't think it's a secret to say this administration wants deals.' Former FTC chair Lina Khan's communications director Douglas Farrar was blunter: 'The Trump-Vance antitrust agenda should be obvious to everyone now: Monopolies pay cash to corrupt lobbyists to get out of lawsuits and keep padding their profits by gouging US consumers.' (Source: Axios, Mar. 13, 2026)

▶ Implications for Korea's Media & Entertainment Industry

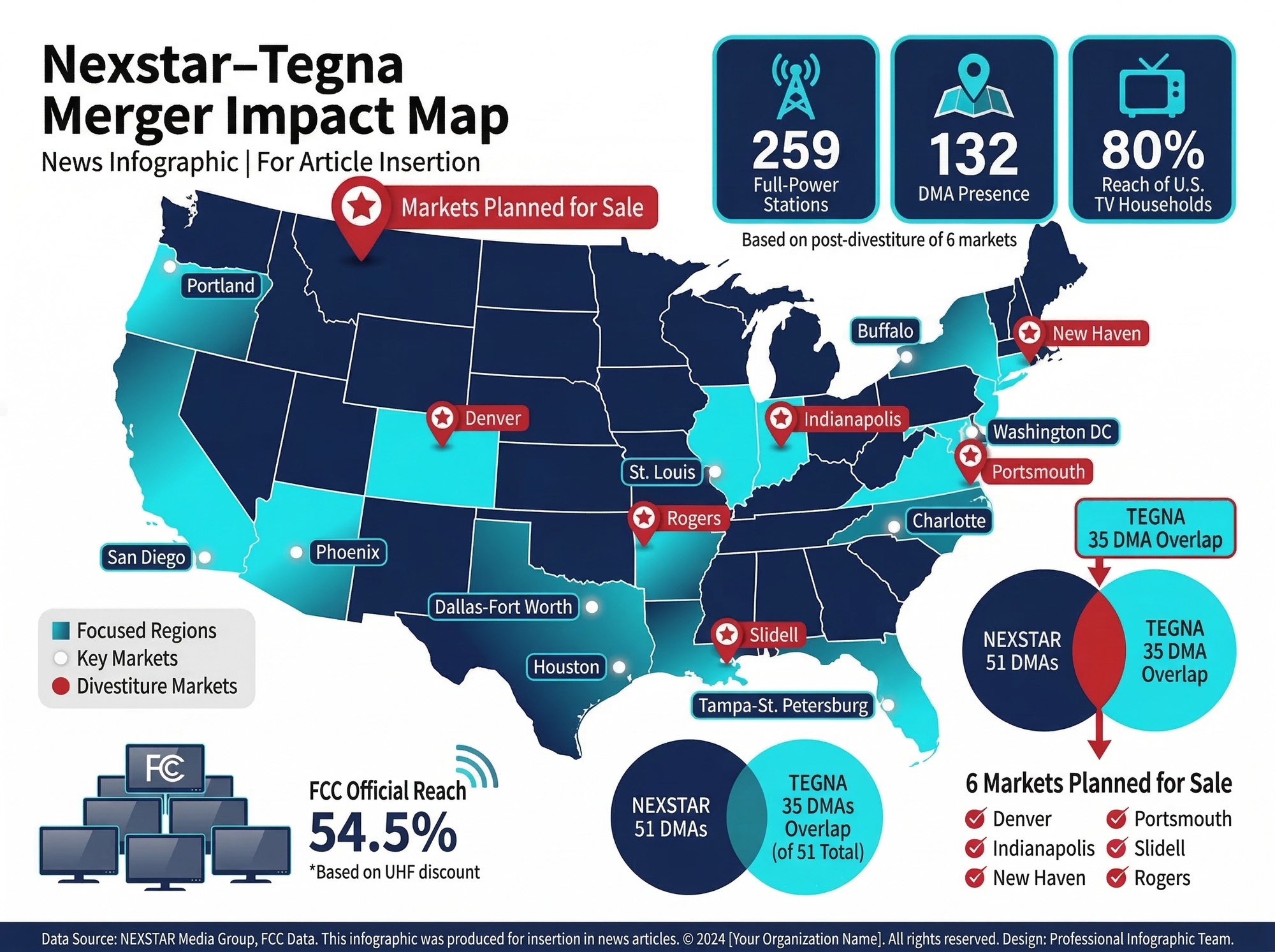

US local broadcasting has been fundamentally restructured. On March 19, 2026, the FCC Media Bureau and the DOJ Antitrust Division simultaneously cleared Nexstar Media Group's $6.2 billion acquisition of TEGNA. Nexstar declared the deal closed within hours. The FCC had received the application on November 18, 2025 — just 121 days earlier. Under Obama and Biden, comparable broadcast mergers routinely sat under review for 300 days or more. The speed itself was the message.

The combined entity spans 265 TV stations across 44 states and Washington D.C., reaching approximately 80% of US television households. With $8.1 billion in annual revenue and affiliates across all four major networks — ABC, CBS, FOX, and NBC — Nexstar becomes a single super-group with unprecedented reach in US local television. The political dimension was explicit: President Trump posted 'Get that deal done!' on social media in February, framing the merger as a check on 'fake news networks.' FCC Chair Brendan Carr responded publicly: 'Let's get it done.' The spectacle of a regulatory chief publicly endorsing a specific private transaction in response to a presidential post was unprecedented.

Meanwhile, Sinclair Broadcast Group — the third-largest local broadcaster — launched a $538 million hostile bid for Scripps at $7 per share. Scripps' board rejected it unanimously as 'not in the best interests of Scripps and its shareholders,' and activated a one-year poison pill defense, buying time to evaluate alternatives. The FCC ownership cap — which prohibits any single broadcaster from reaching more than 39% of US television households — remains a constraint, though FCC Chair Carr has signaled it is an agency rule open to waiver, not a statutory hard limit. That interpretation, applied in the Nexstar approval, means the door to further consolidation is structurally open.

For Korean content in the US, SBS has already moved. In March 2026, SBS signed a strategic partnership with Sinclair to launch K82, a K-drama and variety block on Sinclair's NextGen TV (ATSC 3.0) infrastructure targeting up to tens of millions of households in major US cities — the first time K-content has been distributed on US over-the-air broadcast television. (Source: K-EnterTech Hub, Mar. 21, 2026)

▶ Implications for Korea's Media & Entertainment Industry

The proposed merger between Paramount·Skydance and Warner Bros. Discovery (WBD) marks the third major studio consolidation event in six years, following the Fox-Disney merger in 2019 and the Skydance-Paramount deal in 2025. Hollywood is moving from a five-to-six major studio system toward a three-to-four supergroup architecture.

The combined entity would control HBO Max (Max), Paramount+, a major theatrical distribution network, and a vast IP library — completing the vertical integration of content production, distribution, and streaming platform in a single corporate structure. The logic is structural: Netflix's global dominance has made standalone SVOD platforms unviable without scale. Without scale, there is no original content budget; without content, there are no subscribers. Merger is not an ambition — it is a survival calculation.

▶ Implications for Korea's Media & Entertainment Industry

The Department of Justice settled its antitrust case against Live Nation and Ticketmaster without ordering a corporate breakup, closing a legal challenge that had argued the 2010 merger of the two companies created an illegal monopoly that raised prices for consumers and suppressed competition. The case was filed in 2024; trial began in early March 2026. It ended five days later with a White House settlement.

The settlement's terms: no venue divestitures from Live Nation's portfolio of roughly 50–60 large amphitheaters; termination of 13 exclusive ticketing agreements with specific venues; and an opening of those venues to all promoters. Dozens of state attorneys general are continuing their own separate case. Antitrust experts have been critical: the settlement does not address Live Nation's control of roughly 50% of the concert promotion market, and critics argue that fee caps and platform opening fall well short of meaningful structural remedy.

The political backstory is significant. According to the Wall Street Journal, President Trump personally called aides to ask why the case hadn't been settled, and Ariel Emanuel — a Hollywood talent agent and former Live Nation board member — advised the president to settle. The White House meeting between Live Nation CEO Michael Rapino and AG Bondi occurred on March 5; the settlement was signed that day. 'I only saw the term sheet when you did,' the DOJ's lead trial attorney told the judge in court.

Axios framed the broader signal clearly: companies looking to consolidate, acquire rivals, or merge — including in AI and emerging tech — 'may be seeing a green light from Washington.' The former DOJ official added: 'A little bit of modest enforcement could have gone a long way to preventing the kind of concentration that we see today. The same is true in AI where a little bit of enforcement up front could save a lot of difficult litigation later on.' (Source: Axios, Mar. 13, 2026)

▶ Implications for Korea's Media & Entertainment Industry

▣ Table 3. Global Advertising Market Share Shift and FAST Growth Forecast

Google, Meta, and Amazon are recording successive advertising revenue highs, powered by AI-driven targeting and data infrastructure that competitors cannot replicate at scale. Traditional media publishers are being squeezed out: their combined share of the top-25 advertising earner pool has fallen from 27.84% in 2016 to 7.3% in 2024, according to WPP Media. The trend is structural, not cyclical.

On the antitrust front, Big Tech has weathered the storm. The government lost its case against Meta. It won two cases against Google but a judge rejected the breakup of its search business. With AI advertising ecosystems consolidating around their platforms, Big Tech's market dominance is set to deepen further. The only meaningful counterforce — Congressional legislation — faces a low probability of near-term enactment under the current political configuration.

▶ Implications for Korea's Media & Entertainment Industry

The Live Nation settlement crystallized the Trump administration's antitrust doctrine in a single phrase, delivered by a senior DOJ official to Axios: 'We're willing to bring cases. But we're also not afraid to settle. I don't think it's a secret to say this administration wants deals.' This is the MAGA antitrust model: enforcement as performance, settlement as outcome, political alignment as the operative variable.

The pattern is now three cases deep. HPE's $14 billion Juniper acquisition was settled without the Mist AI business divestiture that antitrust staff had demanded. Compass's $1.6 billion acquisition of Anywhere Real Estate cleared without even a second request after Davis appealed to Blanche's office and antitrust staff were overruled. Live Nation kept its venues. In each case, the antitrust division's professional recommendations were superseded by senior political appointees.

Former Biden-era antitrust officials have described the settlement as 'the end of the left-right antitrust coalition' — the bipartisan political consensus that had previously made consumer-facing monopoly cases like Ticketmaster politically untouchable. Alford, the fired Slater deputy, warned at an antitrust policy forum: 'The cost to the country of this new pay-to-play approach to antitrust enforcement is enormous.' (Sources: WSJ, Mar. 20, 2026; Axios, Mar. 13, 2026)

The historical arc is telling. When Live Nation first acquired Ticketmaster in 2010, the Obama DOJ imposed behavioral restrictions rather than blocking the merger. In 2019, Trump's first-term DOJ accused Ticketmaster of violating those terms and amended the consent decree. In 2024, the Biden DOJ filed for full structural separation. In 2026, Trump's second term ended that pursuit in five trial days. Sixteen years of regulatory history, effectively reset.

▶ Implications for Korea's Media & Entertainment Industry

▣ Table 4. K-Content Industry Risk Matrix and Strategic Response

The cases documented in this report — across local broadcasting, studio consolidation, live events, and Big Tech advertising — collectively show that oligopoly structures centered on a small number of dominant corporations are becoming institutionally entrenched across the US media landscape. Korea's media and entertainment industry has reached the point where it must quantify these risks and translate them into actionable strategic responses.

Strategy 1. Platform Diversification and Direct FAST Monetization

Strategy 2. IP Sovereignty and Preemptive Contract Design

Strategy 3. Asian Content Alliance

In the US media market, scale has become not a choice but a condition of survival. Whether Korean content companies emerge from this restructuring as component suppliers or as partners with independent value to bring to the negotiating table depends entirely on the choices made right now.

Sources & References

① Dana Mattioli, Rebecca Ballhaus & Josh Dawsey, "The Threats and Bare-Knuckle Tactics of MAGA's Top Antitrust Fixer," The Wall Street Journal, March 20, 2026.

② Dan Primack, "DOJ settles antitrust case with Live Nation and Ticketmaster," Axios, March 9, 2026.

③ Ashley Gold, "The emerging MAGA antitrust model," Axios, March 13, 2026.

④ Sara Fischer, "Scripps rejects Sinclair's hostile bid," Axios, March 2026.

⑤ Jung Han, "미국 방송 지형의 대전환: 넥스타–테그나 62억 달러 합병, 한국 미디어에도 직격탄," K-EnterTech Hub, March 21, 2026.

⑥ Todd Spangler, "Nexstar Claims Its $6.2 Billion Deal for Tegna Has Closed Following DOJ and FCC Approvals," Variety, March 19, 2026.

⑦ Todd Spangler, "Nexstar-Tegna Deal: Eight States File Emergency Motion to Halt 'Disastrous' Merger," Variety, March 20, 2026.

⑧ Raquel Calhoun, "DirecTV Files Antitrust Lawsuit to Block $6.2 Billion Nexstar-Tegna Merger," TheWrap, March 19, 2026.

⑨ Ted Hearn, "D.C. Memo: Nexstar-TEGNA Deal Sails Through Carr's FCC in a Speedy 121 Days," Policyband, March 20, 2026.

⑩ WPP Media, Top 25 Global Advertising Earner Data, 2016 vs. 2024.

This report was produced by the K-EnterTech Hub Industry Analysis Team. It synthesizes the above sources with original analysis focused on strategic implications for Korea's media and entertainment sector. Market figures reference cited sources; FAST market projections reflect K-EnterTech Hub's own estimates. All company and individual names are cited as they appear in the original source materials.

![[투비]The Stream 2026: When Intention Becomes Attention](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/03/6h3xe4_202603220154.png)

![[SXSW2026]에이미 웹 트렌드 리포트(Convergence

Outlook 2026)](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/03/kty3s8_202603152312.png)

![[보고서]전통 언론사의 크리에이터 전략 대전환](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/02/0nwc9z_202602100212.png)