Samsung TV Plus posts the sharpest expansion of any platform (13 → 34 in two years); the same MSO–PP integration logic that built NBCUniversal and CJ ENM is now reshaping FAST.

As the FAST (Free Ad-Supported Streaming TV) market enters a phase of mounting financial pressure, owned-and-operated (O&O) channels have emerged as the industry's most strategically valuable asset. Unlike licensed third-party channels, O&Os are fully owned by the platforms that run them — generating advertising revenue with no profit-sharing obligation. Every ad dollar earned on an O&O channel stays inside the platform.

90년 대 케이블TV 전략을 벤치마킹하는 FAST 플랫폼..이용자를 가둬라

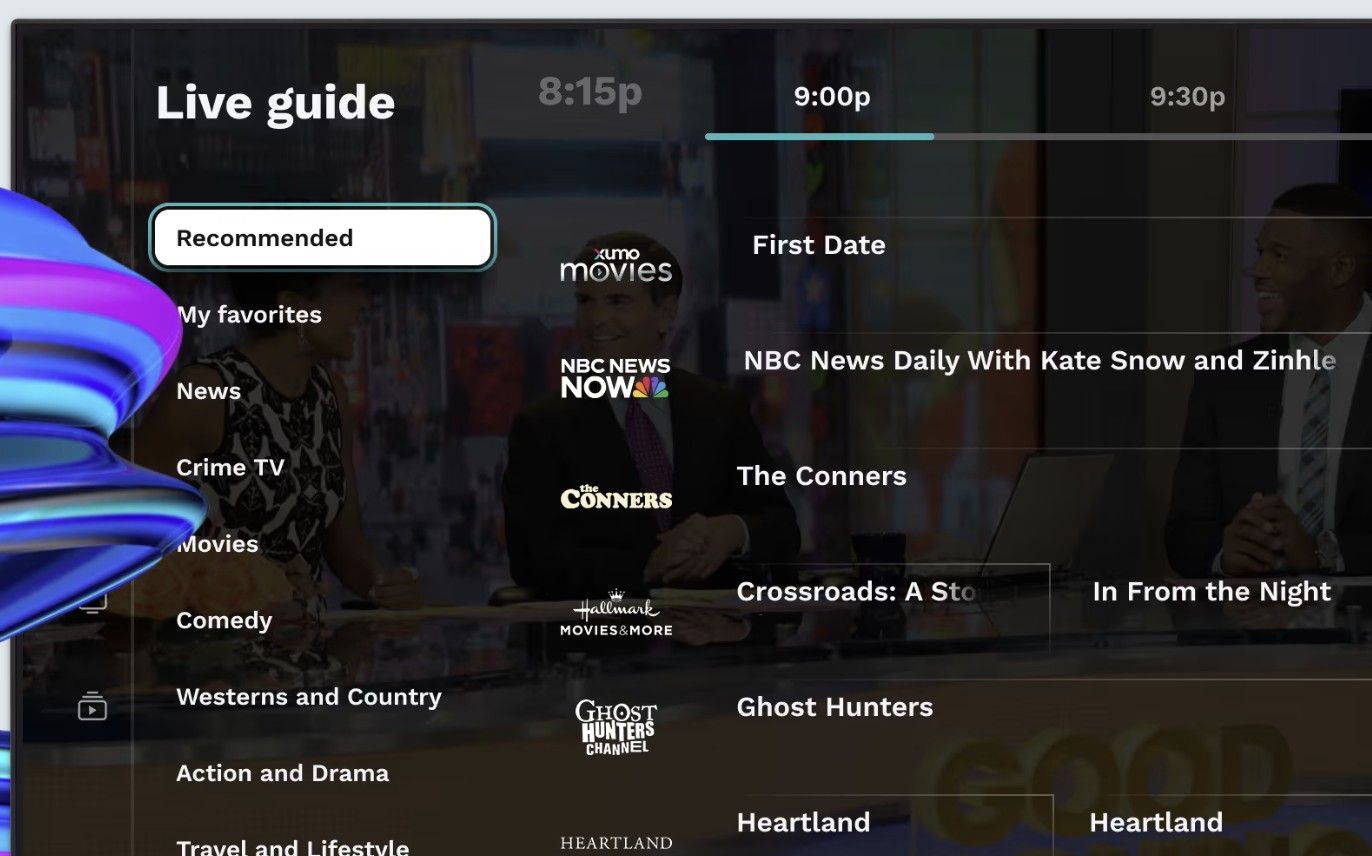

FAST O&O 채널은 2020년 이후 빠르게 늘어 2024년에 피크를 찍은 뒤 2026년에 약간 줄었지만, 그 안을 들여다보면 파라마운트(Pluto TV)는 비효율 채널을 정리하는 대신 핵심 IP 중심으로 효율화하고, 삼성 TV Plus·LG Channels·Vizio WatchFree+ 같은 디바이스 OS 진영 자체 브랜드 채널을 공격적으로 늘려. ‘유통+편성+데이터+광고기술’을 한 번에 쥐는 방향으로 수직통합 가속하는 국면

Jung Han

Jung Han