![[The Future of Korean FAST] News and Sports: The Two Genres That Open the Market](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/07/6t6y02_202607050750.png)

The conditions for opening Korea's domestic FAST market, read through genre data in Amagi's June 2026 AIRTIME Report and the market outlook

News takes 33% of ad impressions on 27% of viewing; CTV advertising heads to $81B by 2030, overtaking linear TV

The genres that open Korea's FAST (free ad-supported streaming TV) market are not drama, but news and sports. Korean FAST has struggled to take root — not for lack of viewers, but because three constraints are locked together: a demand structure without cord-cutting, a content supply blocked by holdbacks, and a still-immature connected-TV (CTV) advertising market. News and sports are the genres that can release these constraints in order.

Jung Han

Jung Han

With no holdback windows they do not collide with pay-TV or OTT revenue, so supply opens first; they fill the live viewing hours pay TV cannot cover, creating demand; and as brand-safe, real-time ad inventory they draw advertisers into CTV.

News has emerged in the global market as a monetization genre whose advertising exceeds its viewing share, and in Asia-Pacific, the region Korea belongs to, sports has begun to show the same pattern. And 'news' here means more than hard news: K-culture news and entertainment news aimed at the Hallyu fandom, plus fandom verticals such as K-dance and K-pop performance — every genre that moves Korea's own IP into the grammar of news and live — is a candidate.

The evidence is the June 2026 AIRTIME Report from Amagi, the global cloud broadcast solutions company. The report compares Q2 2026 (April 1–June 15) data against the prior-year period across roughly 6,500 channel deliveries distributed through THUNDERSTORM, Amagi's server-side ad insertion platform.

Korean FAST's first constraint: there is no cord-cutting

American FAST began with pay-TV cancellation. According to Korean press reports, U.S. pay-TV fees run about seven times Korea's, and more than 10 million subscribers are reported to have dropped pay TV for streaming in recent years. With 'streamflation' — successive subscription price hikes by Netflix and other streamers — layered on top, free, ad-supported viewing emerged as the alternative. In Kantar Media's research, the share of U.S. households watching FAST at least weekly jumped from 24% in Q3 2022 to 47% a year later.

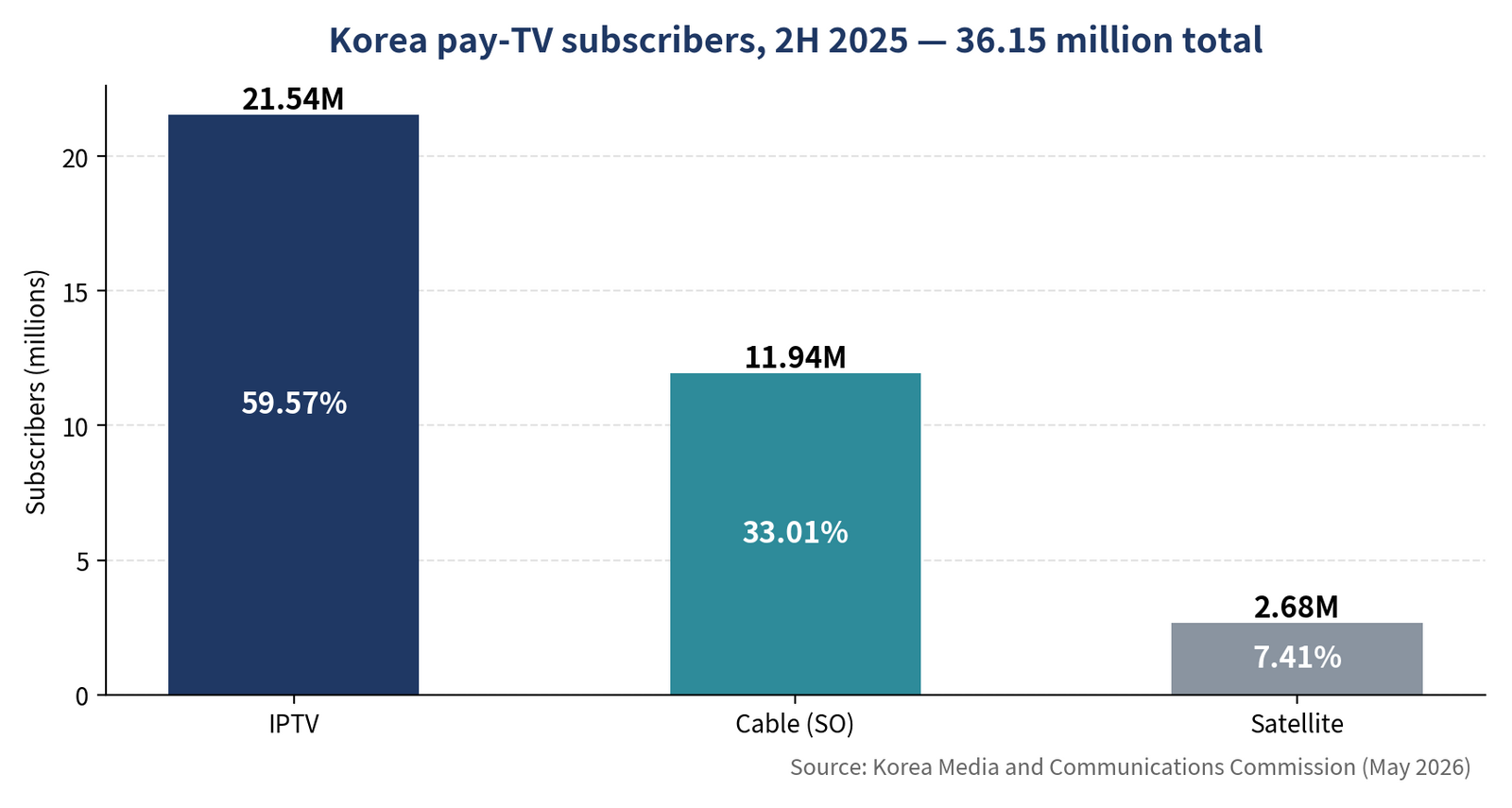

Korea's circumstances are the opposite. According to the Korea Media and Communications Commission's figures for the second half of 2025, released in May 2026, Korea counts 36.15 million pay-TV subscribers — 21.54 million on IPTV (59.6%), 11.94 million on cable SO (33.0%) and 2.68 million on satellite (7.4%).

The total turned negative for the first time in the first half of 2024, but the decline runs at only around 100,000 per half-year — nothing like the millions-strong cord-cutting seen in the U.S. Penetration is near-universal, fees are rated among the lowest in the world, and telecom bundles push the perceived cost lower still. With no reason to cut the cord, the American FAST formula — growing on pay-TV defectors — does not work in Korea. Domestic streamers offering live linear channels narrow the space FAST can squeeze into even further.

[Figure 1] Korea pay-TV subscribers, 2H 2025 — 36.15 million total; IPTV 59.57%, cable SO 33.01%, satellite 7.41% (Source: Korea Media and Communications Commission)

The second constraint: content does not flow in

The supply gap is just as wide. Per Samsung Electronics' January 2026 announcement, Samsung TV Plus operates roughly 4,300 channels across 30 countries and has passed 100 million monthly active users, yet its Korean lineup stops at around 100 channels. LG Channels likewise runs a global channel count many times its domestic one. For content owners, with pay-TV program fees and OTT licensing revenue at stake, there is no reason to hand core libraries to a free platform first. Holdbacks lengthen, and FAST is left with channels built on aging back catalog.

The third constraint: the ad market has not caught up

FAST revenue comes entirely from advertising. In Amagi's data, the U.S. and Canada accounted for 54% of global viewing hours while capturing 74% of ad impressions — proof of how much more ad revenue the region extracts per hour of viewing, and of how mature its CTV ad trading and measurement infrastructure is. Korea's CTV ad market, by contrast, remains early-stage in both transaction volume and measurement standards. Even if channels launch, low ad rates leave no room for content investment; weak content depresses viewing and advertising in turn.

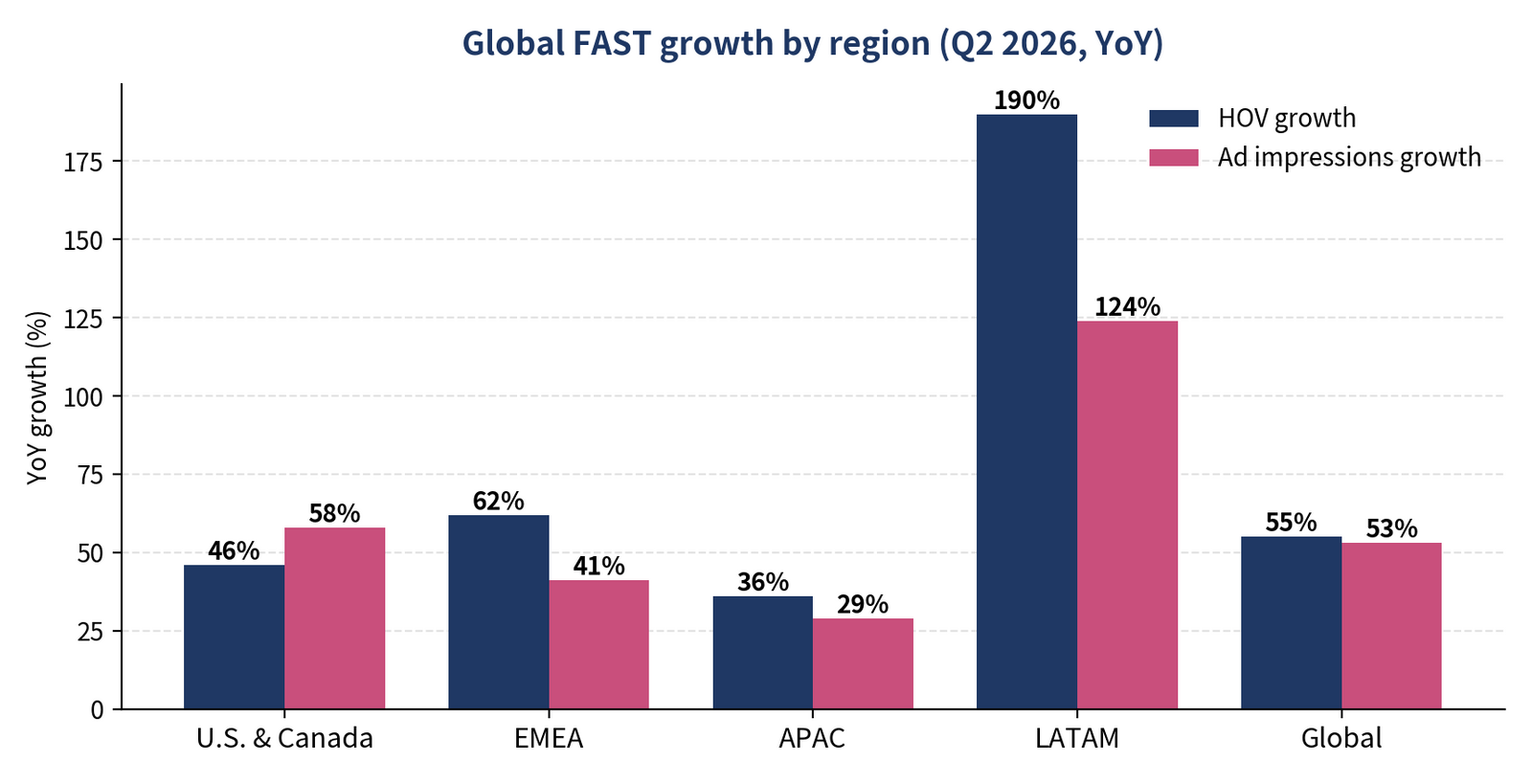

Meanwhile, global momentum has not slowed. On Amagi's platform, total global hours of viewing (HOV) rose 55% year over year and ad impressions rose 53%. By region, Latin America grew fastest with viewing up 190%, followed by EMEA (Europe, Middle East and Africa) at 62%, the U.S. and Canada at 46%, and Asia-Pacific at 36%.

[Figure 2] Global FAST growth by region, HOV vs. ad impressions (Source: recomposed from Amagi AIRTIME Report, June 2026)

Why drama is not the answer

Under these three constraints, a drama-and-variety library strategy has no exit. The rights and IP to new and buzzworthy K-dramas are locked into global streamers, Netflix above all. What can be supplied to FAST is back catalog past its holdback — content also available on OTT and pay-TV VOD. Asking viewers to watch the same titles with ads persuades neither Korean households on bundles costing around 10,000 won a month, nor overseas audiences already consuming K-drama on subscription platforms.

It is true that entertainment leads the global data at 41% of viewing hours. But that market has already been filled by Pluto TV, Tubi, The Roku Channel and others with vast English-language libraries. Rather than fighting for share inside it with aging Korean dramas, Korean players have better odds seizing the genres that do not overlap with OTT and exist only on FAST. Those genres are news and sports. The regional data bears this out — and it also dictates the order in which the domestic market opens.

The U.S. market: entertainment is biggest, but the money moves to news

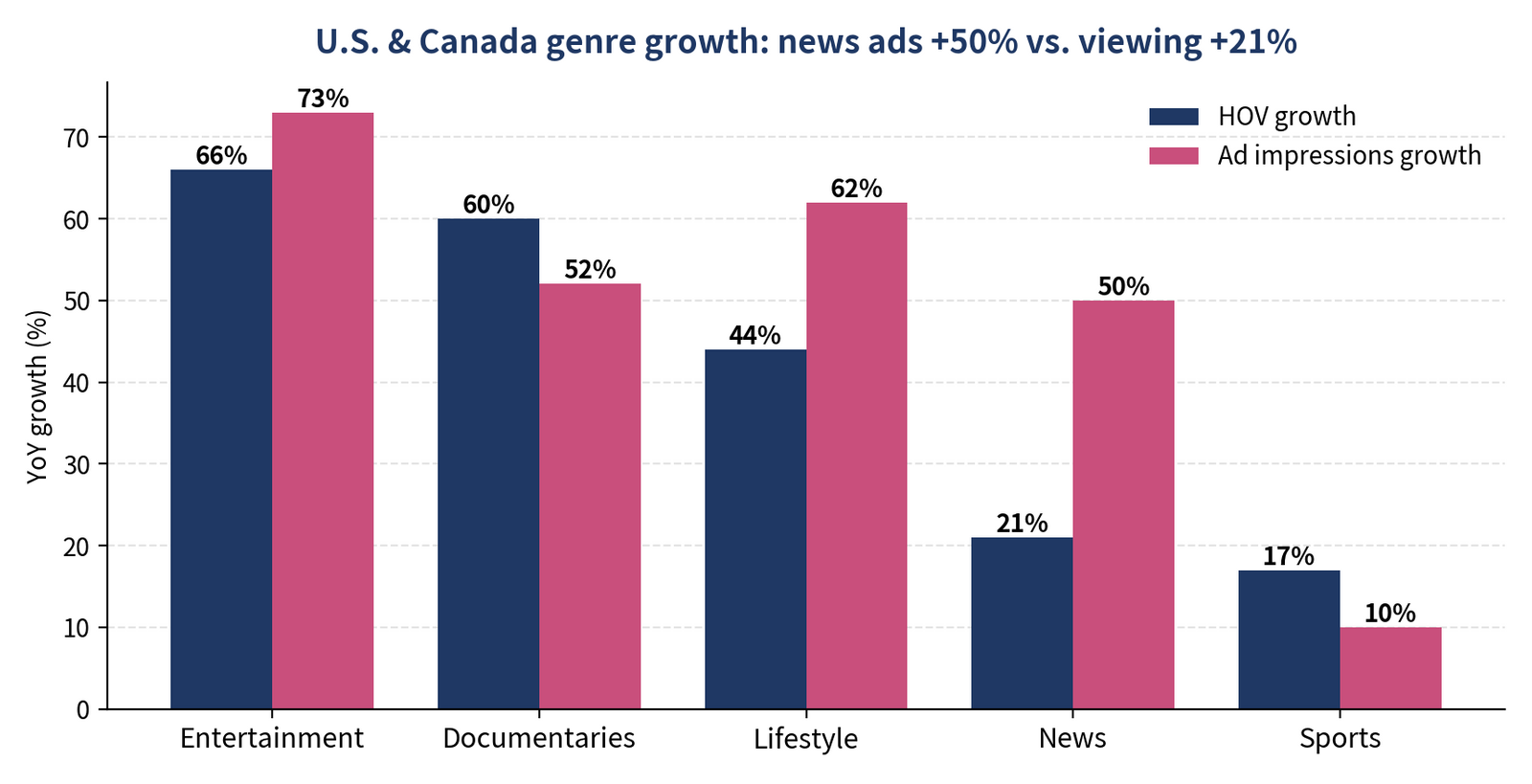

Per the Amagi report, entertainment leads FAST's largest market — the U.S. and Canada — at 43% of viewing hours, followed by news (31%) and lifestyle (11%). By growth, kids dominated at 187%, with entertainment (66%) and documentaries (60%) next. News viewing grew a modest 21% — but news ad impressions rose 50%. It is the only genre in this market where advertisers are loading budgets at more than twice the pace the audience is growing.

[Figure 3] U.S. & Canada genre growth — only in news does ad growth far outpace viewing growth (Source: recomposed from Amagi AIRTIME Report, June 2026)

Local news generated 23% of U.S. news viewing. Not just national channels but community-level news builds its own audience and ad market on FAST — confirming in numbers the strategy of U.S. broadcast groups converting their local newscasts into FAST channels. In sports, general sports programming (42%) and motorsports (35%) accounted for three-quarters of viewing; documentaries were led by general documentary (31%) and science (20%).

Beyond the U.S.: Europe, Asia and Latin America grow differently

If the U.S. holds FAST's money, the growth comes from outside it. Regional genre maps differ from one another — and so does the playbook for Korean channels entering each region.

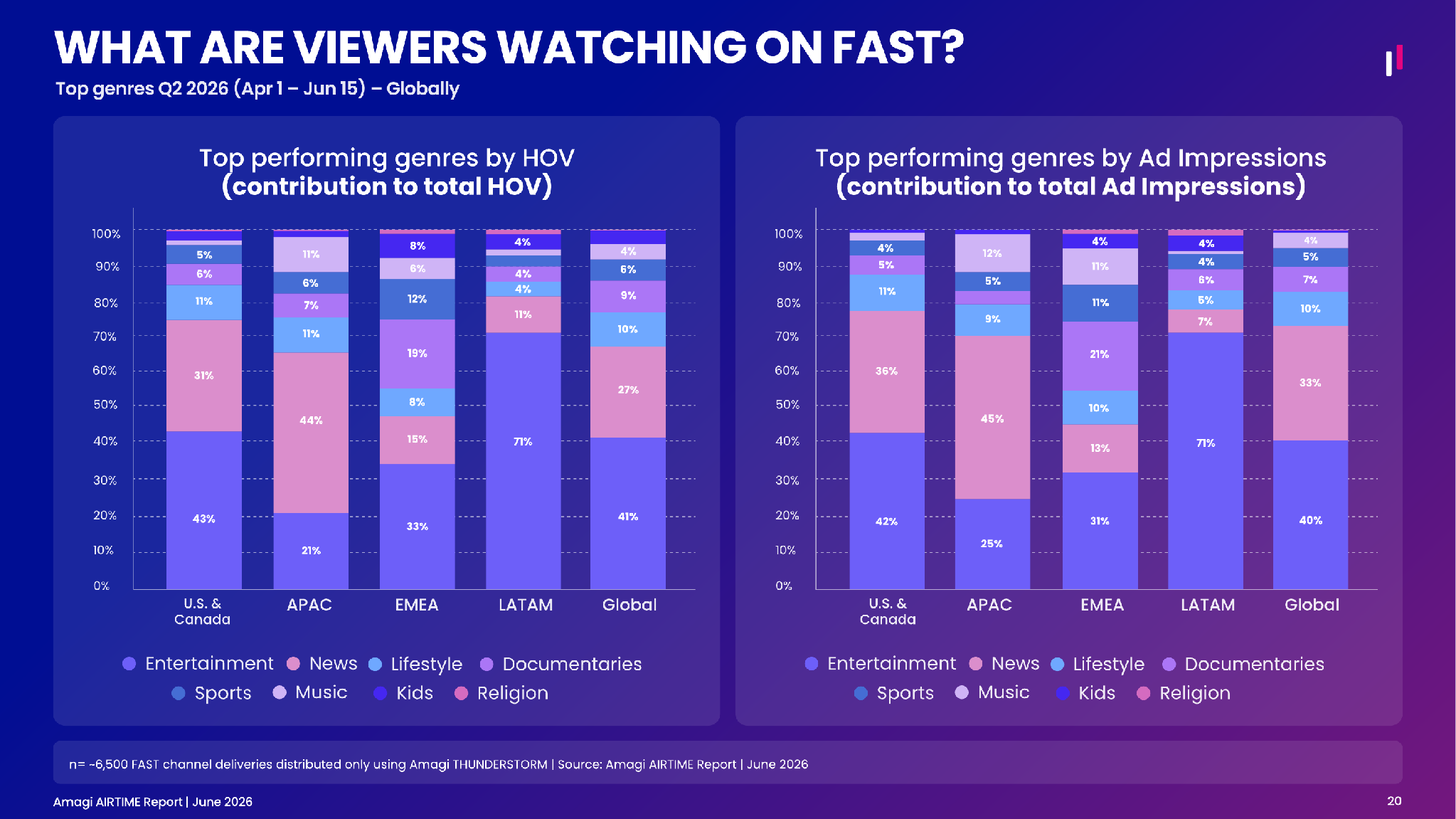

[Figure 4] Top genres by region — contribution to HOV and ad impressions (Source: Amagi AIRTIME Report, June 2026)

EMEA: a documentary and sports market

In EMEA, entertainment (33%) leads, followed by documentaries (19%) and news (15%). By growth, kids (262%) came first, then sports (98%) and news (85%). Documentary viewing concentrated in nature (39%) and wildlife (31%); sports was led by motorsports (31%), tennis (20%) and football (15%). It is a market where single-discipline channels build sports viewing without Premier League-scale rights.

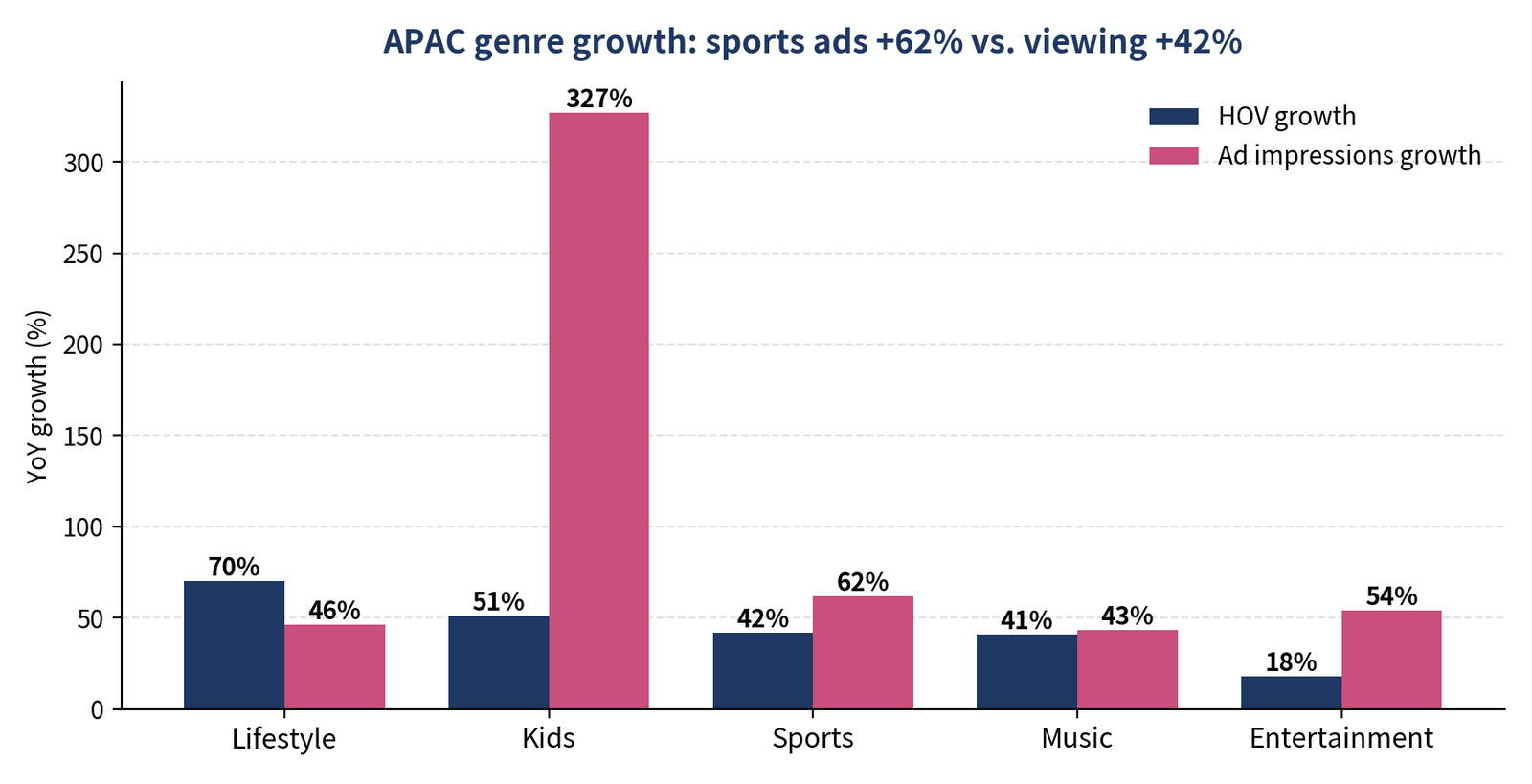

Asia-Pacific: news is the center of the market

In Asia-Pacific, Korea's home region, news is the top genre at 44% of viewing hours and 45% of ad impressions — more than double entertainment's 21%. Growth was led by lifestyle (70%), kids (51%) and sports (42%). Among these, sports ad impressions rose 62%, outpacing viewing, and kids ad impressions surged 327%. Sports viewing combined broad general-sports programming (37%) with motorsports (18%) and tennis (15%).

[Figure 5] APAC genre growth — sports and kids ad growth outpaces viewing growth (Source: recomposed from Amagi AIRTIME Report, June 2026)

Latin America: entertainment dominates, news grows fastest

Latin America is effectively a single-genre market, with entertainment at 71% of viewing hours — general entertainment (49%) and drama (37%) together produce over 85% of the genre. By growth, however, documentaries (587%) and news (350%) led, with sports up 121%. Even in emerging FAST markets, once the library genres fill their space, news rises as the growth genre.

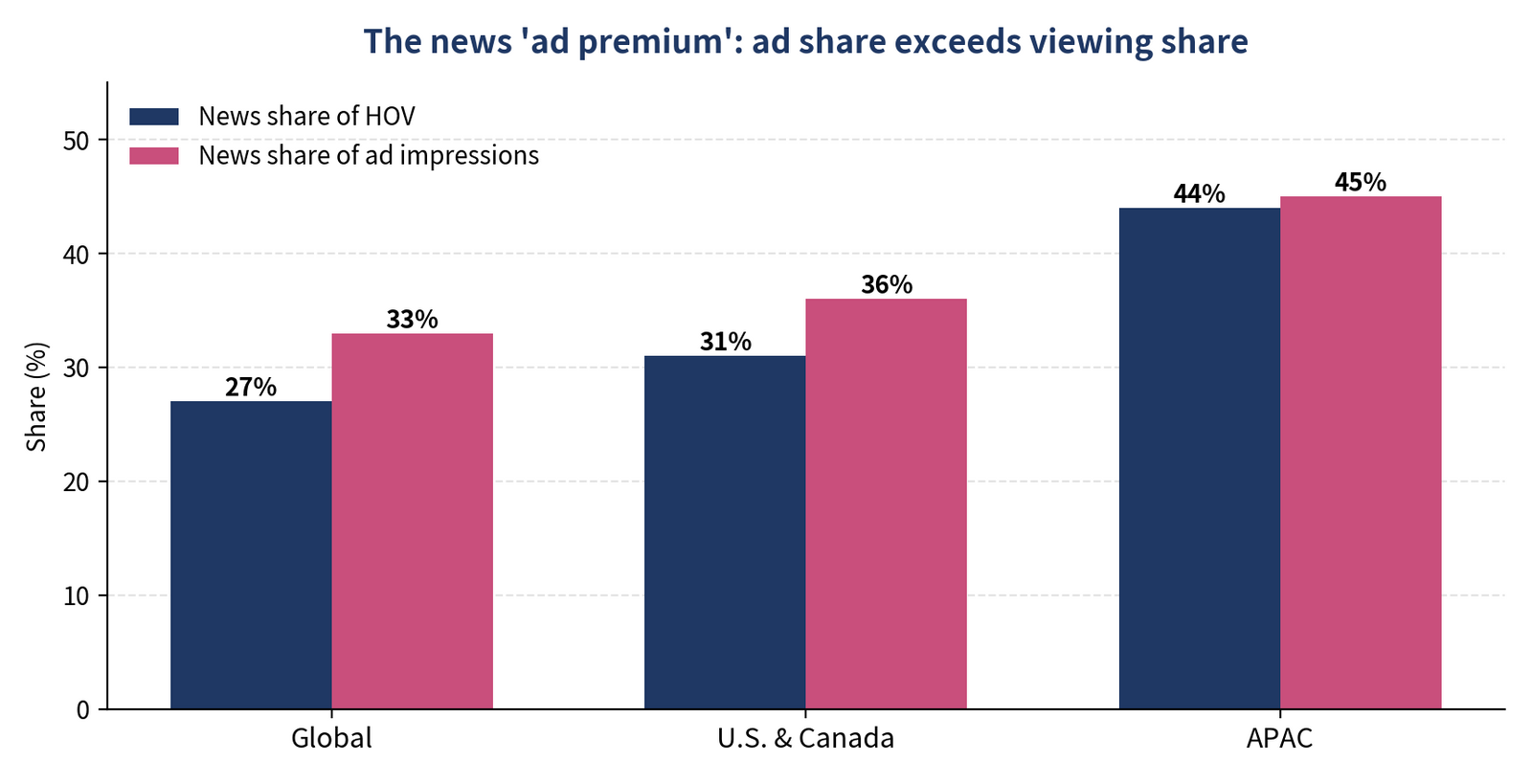

Answer one, news — 27% of viewing, 33% of advertising

The thread running through every region is news. News accounted for 27% of global viewing hours while capturing 33% of ad impressions — an ad share six percentage points above its viewing share — and the report names news among the strongest monetizing genres. A genre with no beginning or end suits FAST's lean-back viewing, and its immediacy and locality provide the brand-safe environment advertisers favor. The gap holds consistently in the U.S. and Canada (31% of viewing, 36% of ads) and Asia-Pacific (44% and 45%).

[Figure 6] News share of viewing vs. share of ad impressions (Source: recomposed from Amagi AIRTIME Report, June 2026)

Korean news assets can be deployed into this genre immediately. News from the all-news channels, terrestrial and general-programming broadcasters is linear content that fills a 24-hour schedule without additional production cost, and with no holdback it does not collide with OTT rights. Korean platforms are already moving. In January 2026, Samsung became the first domestic FAST operator to add 24-hour terrestrial news channels — 'KBS News 24' and 'SBS No.1 News Live' — to Samsung TV Plus. With terrestrial channels joining JTBC News, MBN News, YTN and Yonhap News TV, a domestic FAST lineup once centered on variety and drama has begun widening into news.

[Figure 7] Samsung TV Plus news channel lineup — 24-hour terrestrial news channels including 'KBS News 24' and 'SBS News' (Source: Samsung Electronics)

The extension of news is K-culture news. For Hallyu fans worldwide, an artist's comeback, a world tour, an awards show or a drama production announcement is news. The formula Amagi's report confirmed for U.S. local news — community-level news generating 23% of news viewing — holds for communities of interest as much as communities of place.

The Hallyu fandom scattered across the globe is not a geographic local but an 'interest local,' and a 24-hour K-culture, Hallyu and entertainment news channel aimed at them is the Korean edition of the local-news formula. Content from entertainment media, agencies and broadcasters' entertainment desks can be scheduled in real time with no holdback, just like hard news, and it inherits news's strength as brand-safe ad inventory. It is a news channel only Korea can build — using K-content IP without colliding with global streamers' drama rights.

Answer two, sports — in Asia-Pacific, viewing up 42%, advertising up 62%

Sports is the genre driving growth. On top of viewing gains of 98% in EMEA, 121% in Latin America and 42% in Asia-Pacific, ad impressions in Asia-Pacific rose 62% — the same ad-premium pattern news shows. As the regional sub-genre data indicates, viewing and advertising are built through broad schedules and single-discipline channels, without ultra-premium rights.

Rights holders are changing how they treat FAST. The report features Tennis Australia, operator of the Australian Open; according to the report's interview, the organization is structuring footage from more than 1,260 matches across 16 simultaneous courts with AI tagging and logging — turning the archive into a distributable asset, and showing a rights holder moving beyond selling broadcast rights to operating channels.

The third inventory: K-dance and K-pop performance — entertainment works when it is fandom-driven

That drama back catalog is not the answer does not mean folding entertainment altogether. Within the same genre, unlike dramas whose rights sit with global streamers, K-pop performance, K-dance and music variety are fandom verticals whose IP is held directly by agencies and broadcasters — and they grow stronger the more they combine with live. According to press reports, in 2025 Samsung launched the 'SM TOWN' channel on Samsung TV Plus, carrying content from SM Entertainment artists, and livestreamed an LA concert featuring aespa, NCT 127 and others on FAST. Live events — concerts, showcases, comeback stages — pull the fandom into the channel, while choreography videos, dance challenges and stage archives fill the 24 hours in between.

The data points the same way. Per the Amagi report, the music genre in Asia-Pacific grew 41% in viewing hours and 43% in ad impressions — viewing and advertising rising in step. K-dance and K-pop performance channels combine the grammar of news (real-time, linear, holdback-free) with entertainment's fandom, forming — alongside K-culture news — a third ad inventory Korea can differentiate on global FAST. And because they serve as the entry point of fandom spending that extends to concerts, merchandise and tourism, they carry strong success potential for the K-content industry as a whole.

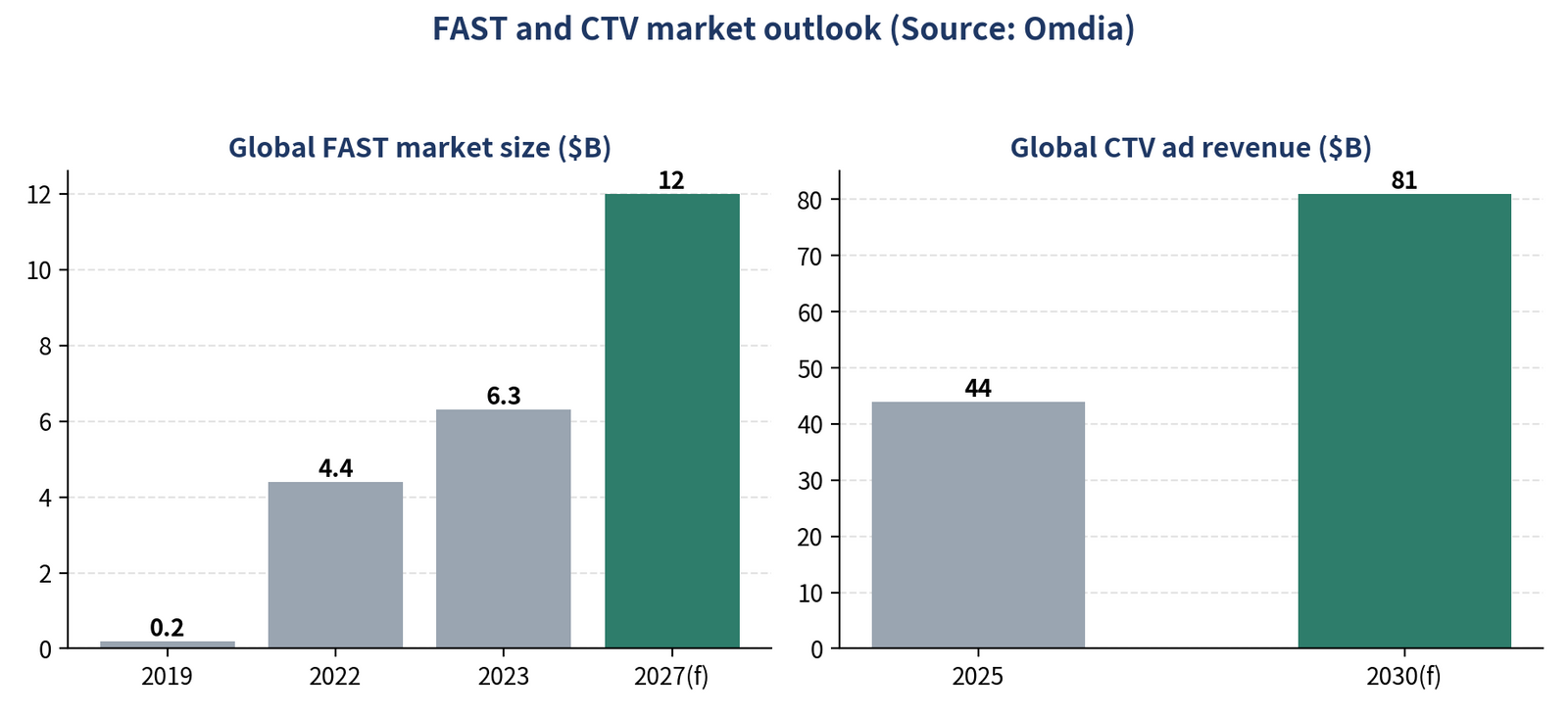

Market outlook: CTV advertising overtakes linear TV in the 2030s

The outlook for the CTV ad market that FAST rides on adds weight to genre strategy. According to Omdia's May 2026 forecast, global CTV advertising revenue will grow from $44 billion in 2025 to $81 billion by 2030 and overtake all traditional linear TV advertising during the 2030s. Per Omdia's tallies and projections, the FAST market itself grew from $0.2 billion in 2019 to $4.4 billion in 2022 and $6.3 billion in 2023, with roughly $12 billion projected for 2027. Industry reports also put worldwide FAST users at a projected 1.1 billion in 2027.

[Figure 8] FAST market size and global CTV ad revenue outlook (Source: Omdia; industry reports)

As the pie grows, its owners are being decided. Omdia expects Google (26%), Amazon (13%) and Netflix (9%) to capture a combined 50% of global CTV ad revenue by 2030. In an environment where Big Tech takes hold of the living room's advertising infrastructure, a channel operator's leverage comes from the quality of its ad inventory. Operators holding genres whose ad share exceeds their viewing share — the genres advertisers fund first — take the larger cut of the expanding pie.

Five keys that open Korea's FAST market

The three constraints must be released in order: without content there is no viewing, and without viewing there is no advertising. News and sports are the answer because they are the genres that can open the first slot in that sequence — content supply.

One: Supply news first — the only genre that does not collide with pay TV

What blocks content supply on Korean FAST is the holdback. Drama and variety cannot be released to a free platform first, with pay-TV program fees and OTT rights at stake. News is different: it is the only genre that can go out on FAST simultaneously with broadcast without cannibalizing existing revenue, and the 24-hour linear assets are already secured. Samsung's January 2026 addition of terrestrial 24-hour news channels 'KBS News 24' and 'SBS No.1 News Live' to Samsung TV Plus — a first for Korean FAST — is the signal that this door is actually opening. Amagi's finding that news accounts for 44% of Asia-Pacific viewing shows that for viewers in this region, news is FAST's default. Korea's first killer schedule is not drama back catalog; it is news that is always on whenever the screen comes up. Add K-culture, Hallyu and entertainment news, and a news lineup that begins with hard-news channels extends into fandom channels.

Two: Build viewing habits with sports and live events

In a Korea without cord-cutting, FAST must enter as a complement to pay TV, not a substitute. The target is the viewing hours pay TV cannot fill — smart monitors and mobile, second screens, ambient viewing — and what opens those hours is live content.

Samsung TV Plus streaming the KLPGA Tour live in Korea, and the 'Bao Family' panda first-birthday livestream from a YouTube-native channel topping the platform's ratings, show that live events become the occasion that draws Korean users to FAST. Add the domestic leagues and amateur or semi-pro competitions that pay-TV sports channels cannot fully carry, live K-pop concerts and showcases, plus fandom-driven creator content, and FAST can become Korea's window for universal free live viewing. Beyond recycling broadcaster content, discovering new content that gathers fandoms is the crux of opening the domestic market.

Three: Build the ad inventory that brings advertisers in

For Korea's CTV ad market to open, ad inventory that advertisers trust must come first. Brand-safe live news and reach-guaranteed live sports are that inventory. Globally, news takes 33% of ad impressions on 27% of viewing; in Asia-Pacific, sports answered 42% viewing growth with 62% ad growth. Once the genres advertisers fund first take root in Korea, the third constraint — low ad rates choking content investment — is released, and with viewing measurement and trading standards in place, the domestic CTV ad ecosystem starts to turn.

Four: Lower the channel's break-even point with AI

In an early market with low ad rates, channel operating costs decide survival — and AI drives them down. Tennis Australia structured footage from more than 1,260 matches across 16 courts with AI tagging and logging, turning its archive into raw material for linear channels; according to press reports, the KBO channel from LG Uplus and Hudson AI replicated a single broadcast into multilingual channels through real-time AI translation and dubbing, peaking above 250,000 daily users. The same method creates the economics for domestic channels: a news or sports channel built for Korea, localized by AI and distributed overseas as-is, earns foreign revenue that sustains the channel until the domestic ad market ripens — a dual-revenue structure.

Five: Point policy at supply, measurement and standards

Since the Media and Content Industry Convergence Development Plan, the government has positioned FAST as a bridgehead for K-content's global expansion. Opening the domestic market needs the same leverage: rules that encourage terrestrial and all-news channels to supply FAST, CTV viewing measurement and ad trading standards, and support that reaches beyond broadcasters to creator and fandom content. In Amagi's survey, 86% of practitioners said poor metadata is already costing them real money, and 68% expect major platforms to dictate metadata standards within three years. Standardizing genre- and program-level metadata is also the policy task that keeps Korean channels alive in global recommendation systems.

Conclusion: the first door has already begun to open

The 2030s, when CTV advertising overtakes linear TV, are already forecast — and Korea's domestic market is not outside that current. Korean FAST stayed shut not because the market does not exist, but because the wrong key — drama back catalog — was used on the door. When holdback-free news opens content supply, live sports and events build the viewing habit, and the two genres' ad premium brings advertisers in, the three constraints on Korean FAST release in order. With terrestrial news now on Samsung TV Plus, the first door has already begun to open.

Sources: Amagi AIRTIME Report, June 2026 — approx. 6,500 channel deliveries via Amagi THUNDERSTORM, Q2 2026 (Apr 1–Jun 15) vs. prior-year period; Figures 2, 3, 5 and 6 recomposed from report data; Figure 1 from Korea Media and Communications Commission data; Figure 7 courtesy of Samsung Electronics. Market outlook: Omdia (incl. May 2026 CTV advertising forecast). Korean market context: Korea Media and Communications Commission pay-TV subscriber figures for 2H 2025 (May 2026), Samsung Electronics Newsroom (Jan 2026), Kantar Media, Korea Communications Agency (KCA) and Korean press reports (incl. Media Today, Aug 2025).