The 39% National Ownership Cap Becomes the Battleground Where Politics and Regulation Collide

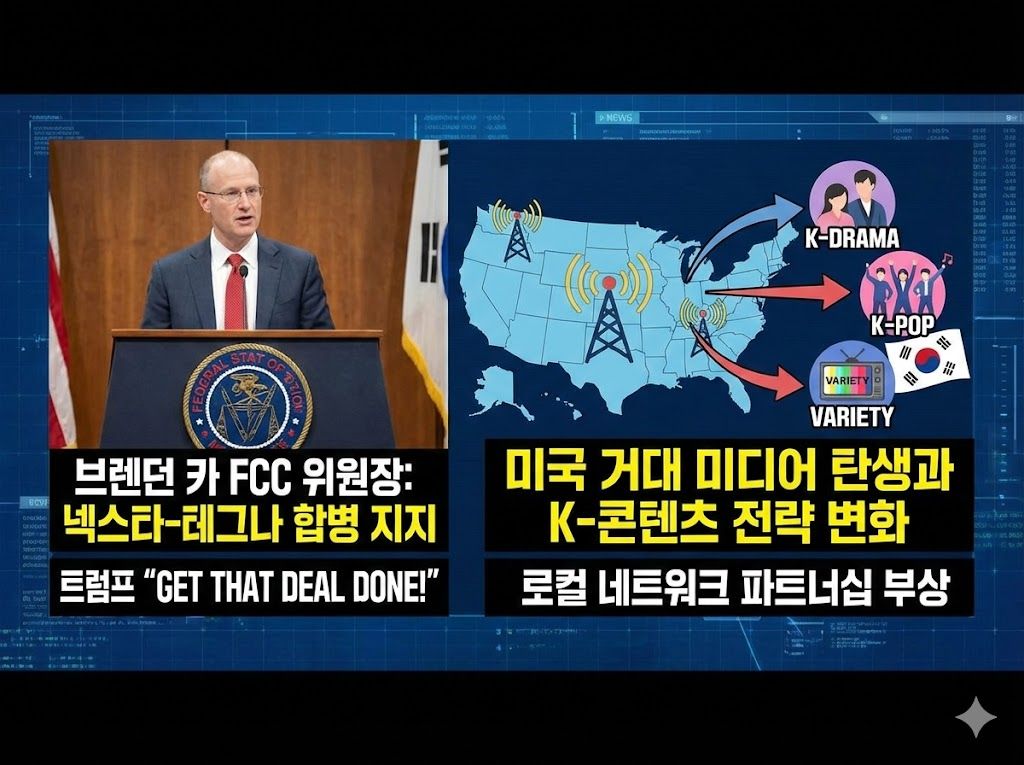

U.S. broadcast regulation is once again being pushed to its limits. Federal Communications Commission (FCC) Chairman Brendan Carr publicly threw his weight behind Nexstar Media Group's acquisition of TEGNA on February 19 in Washington, making clear that the nation's top broadcast regulator intends to clear the path for Nexstar — already the dominant force in local TV stations across the country — to expand into a broadcasting behemoth that also commands national network affiliates and news channels.

Nexstar started in the 1990s as a small Pennsylvania regional broadcaster, then grew into a media giant controlling local TV stations across dozens of U.S. states through repeated acquisitions. If this deal closes, a single company will hold sway over more than half of all U.S. TV households — a hyper-concentrated structure unlike anything the industry has seen. The broader media landscape is already in flux: following the Netflix–Warner Bros. Discovery merger talks, even legacy broadcast markets are now in motion.

"With respect to Nexstar-TEGNA, I support that transaction."

— Brendan Carr, FCC Chairman Washington press conference, February 19, 2026

The Deal's Scale: 265 Stations, Reaching 54.5% of U.S. TV Households

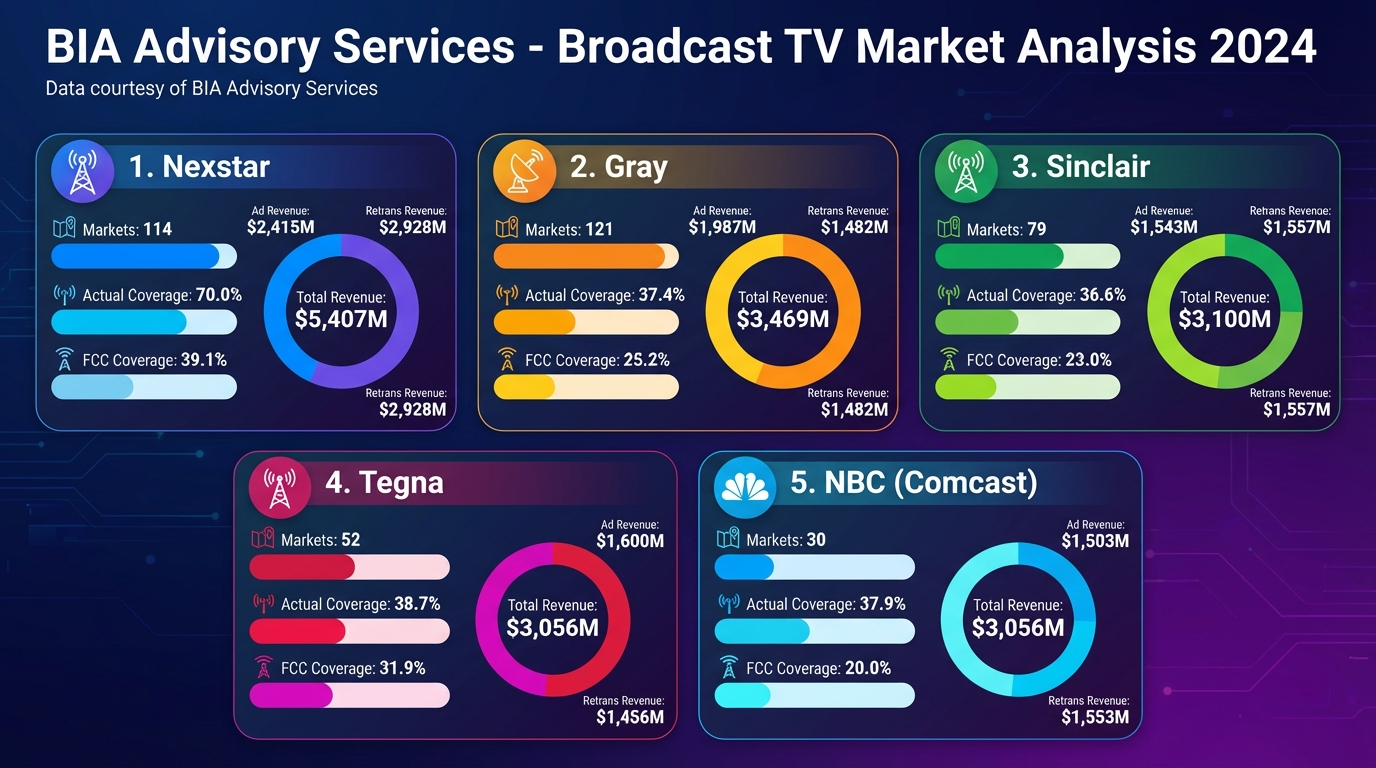

If Nexstar Media Group's $6.2 billion acquisition of TEGNA is completed, it will create the largest broadcast group in U.S. history, owning 265 stations nationwide. Under FCC calculation methods, this combined entity would potentially reach 54.5% of all U.S. TV households.

The problem: the current national ownership cap sits at 39%. That gap of more than 15 percentage points is not merely an FCC-imposed rule — it is a statutory limit rooted in federal law. Crossing it requires either a temporary waiver that effectively circumvents the law's intent, or a full-scale regulatory overhaul that requires congressional involvement.

This is not a question of scale alone. Surpassing the 39% legal cap by more than 15 points amounts to a declaration that the existing regulatory framework must be redrawn to allow what it currently prohibits in principle. The moment Chairman Carr said publicly that he supports the transaction, the Nexstar–TEGNA deal ceased to be a corporate M&A story and became a test case for the future of U.S. broadcast regulatory philosophy.

K-EnterTech Hub Analysis

For the K-content industry, this is not a distant event. If the U.S. local broadcast landscape consolidates under a single dominant operator, the number of negotiating windows for syndication agreements and programming rights for Korean dramas, variety shows, and K-pop content will narrow to a handful of mega-groups. That concentration cuts two ways.

On one hand, "break through once and you get nationwide simultaneous distribution" — a massive pipe opens. On the other, Nexstar's buying power at the scale of a super-group could sharply reduce the negotiating leverage of individual production companies and mid-sized distributors.

Korean content industry stakeholders should read this deal not as "someone else's M&A" but as a structural signal requiring a full redesign of their U.S. distribution strategy.

Trump's Direct Push — The Administration's Intent Goes Official

It is historically unusual for a sitting president to publicly demand the approval of a specific corporate merger under active regulatory review. Yet President Donald Trump did exactly that on February 7, posting directly to Truth Social:

"Those that are opposed don't fully understand how good the concept of this Deal is for them, but they will in the future. GET THAT DEAL DONE! PRESIDENT DJT"

— Donald Trump, President of the United States Truth Social, February 7, 2026

Chairman Carr responded the same day, sending what amounted to a public political endorsement of the local broadcaster coalition while criticizing the national network establishment:

"President Trump is exactly right. The national networks like Comcast & Disney have amassed too much power. For years, they've been pushing this Hollywood & New York programming all over the country with no real checks."

— Brendan Carr, FCC Chairman February 7, 2026

K-EnterTech Hub Analysis

Chairman Carr's remarks go beyond a simple pro-deregulation signal. They reveal a political and regulatory reframing of media power dynamics.

First, by targeting the concentrated influence of national networks like Comcast and Disney, Carr is publicly criticizing the existing structure in which "Hollywood & New York programming" has been pushed nationwide without real checks.

Second, he is positioning local broadcaster coalitions — Nexstar, Sinclair, TEGNA — as a new power axis, a "counter-power" to the national networks.

From a K-content perspective, this is a signal that U.S. market entry partners need not be limited to streaming platforms or national networks (ABC, NBC, FOX, CBS). With the administration officially backing local broadcaster groups as rivals to the national networks, K-content operators should proactively explore strategic partnerships with local station coalitions (e.g., Sinclair affiliates), including ATSC 3.0 channel launches, advertising, sports, and news collaboration.

The Procedural Battle: Full Commissioner Vote vs. Media Bureau Unilateral Approval

How the deal gets processed at the FCC has become just as contentious as whether it gets approved. Democratic FCC Commissioner Anna Gomez pushed back directly at the February 19 press conference:

"This should be voted at the Commissioner level. It should absolutely not be done at the bureau level. It's a new and novel issue. And it is also a very difficult issue because actually approving the transaction would be prohibited by the statutory cap on ownership."

— Anna Gomez, FCC Commissioner FCC press conference, February 19, 2026

Commissioner Gomez's argument operates on two levels.

First, procedurally: because a transaction that exceeds the statutory 39% national ownership cap is an unprecedented and legally complex matter, it should not be delegated to the Media Bureau but must be decided through a full vote of all five commissioners.

Second, legally: because approving the Nexstar–TEGNA combination — which would push estimated national reach above 54% — would directly conflict with the statutory cap set in the Communications Act, a simple waiver cannot provide a lawful basis for approval.

If Chairman Carr's side opts for Media Bureau-level processing, the deal can move forward without a formal recorded vote against it from Democratic commissioners. If it goes to a full commission vote, the statutory cap violation and delegation-of-authority debate becomes front and center.

K-EnterTech Hub Analysis

This episode confirms the foundational principle of regulatory politics: procedure is power. Which body handles a matter, under which delegated authority, and at which level of review shapes outcomes before substance is even debated.

Korean media companies examining U.S. partnerships, investments, or M&A should build procedural selection risk into their analysis — not just the substantive merits of a deal.

The Unlikely Leading Opponent: A Trump Ally, Newsmax CEO Chris Ruddy

The loudest voice against the deal comes from a surprising direction. Chris Ruddy, CEO of conservative cable news channel Newsmax — long known as a close ally of President Trump — has taken a hardline public position against the Nexstar–TEGNA acquisition and the regulatory relaxation being pushed to enable it. At a recent Senate Commerce Committee hearing, he drew a clear line:

"I am prepared to litigate FCC departure from the 39% cap."

— Chris Ruddy, CEO, Newsmax Senate Committee hearing, February 10, 2026

Ruddy's logic is straightforward. If the merged Nexstar–TEGNA group expands to cover more than half of all U.S. households, it would exercise near-monopoly power in local advertising and retransmission consent negotiations, potentially passing excessive costs onto cable, satellite, and independent channels. An independent conservative channel like Newsmax — dependent on local distribution deals — could find itself edged out by competing channels bundled into retransmission packages (such as NewsNation) with the new super-group.

More fundamentally, Ruddy argues that the 39% cap is a congressionally mandated statutory limit, and that the FCC acting unilaterally to waive or de facto abolish it would constitute a violation of federal law and an exceeded authority — grounds for federal court action. Newsmax has already filed an official petition to deny with the FCC, documenting how the transaction would harm local news diversity and competition.

President Trump initially appeared to echo Ruddy's caution, but by February 7 had pivoted decisively, publicly demanding the deal be done — effectively brushing aside his old ally's position. The result: a visible intra-conservative clash over media ownership between the President, the FCC Chairman, and a major cable news operator.

'Media Is Business, Not Politics'

The Newsmax episode sends two important signals to the K-content industry.

First: in the streaming era, media is industry, not ideology. Basing U.S. media market strategy solely on political alignment or administration posture is dangerous. Even within the same political camp, national broadcast groups, local station coalitions, independent news channels, cable/satellite operators, and big tech/streaming platforms each have distinct — and sometimes directly conflicting — interests in ownership rules, retransmission fees, and advertising markets.

Second: whether a strategic alliance or equity stake with a particular major broadcast group could simultaneously damage relationships with other conservative or liberal channels, regional broadcasters, or distribution platforms — and whether it could trigger litigation or regulatory risk — must be evaluated on its own axis, separately and rigorously.

In short: this episode demonstrates that political alignment cannot substitute for regulatory risk hedging or market entry security. K-content operators selecting U.S. partners must conduct multi-dimensional stakeholder analysis — ownership structure, regulatory positioning, litigation history, local advertising and retransmission strategy — rather than relying on political or ideological labels.

The DOJ Variable: Slater Out, Assefi In — The Last Independent Brake Weakens

Beyond FCC approval, the deal must also clear the Department of Justice (DOJ) Antitrust Division — a second independent regulatory gate. Last week, a significant personnel shift hit that gate.

Abigail Slater, Trump's own appointee as Assistant Attorney General for Antitrust, resigned abruptly on February 12. Reports suggested the White House effectively pushed her out over internal disagreements and policy differences. Deputy Omeed Assefi was installed immediately as acting head of the Antitrust Division. The news raised immediate questions about whether DOJ's willingness to push back on major media consolidation had materially weakened.

Blair Levin, policy advisor at New Street Research, framed the implications of the change this way:

"We think Slater would have been more likely than her successor to entertain certain Top Four divestitures notwithstanding the repeal of the FCC's Top Four rule. Her successor will be more likely to follow the FCC's lead and determine that owning two top four stations (other than perhaps in a handful of middle or smaller markets) would not harm competition."

— Blair Levin, Policy Advisor, New Street Research

Slater's departure signals the effective weakening of DOJ's independent oversight function — its ability to operate as a check separate from FCC. If acting head Assefi realigns DOJ to follow the FCC's direction, two separate regulatory gates collapse into a single political line of authority.

K-EnterTech Hub Analysis

Under Slater, the DOJ had the potential to act as a separate counterweight to the FCC — checking the merger on competition and market structure grounds independently of ownership rule changes. Specifically, even if the FCC weakened or effectively nullified the Top Four rule, the DOJ could have required divestitures of certain stations on the grounds that a single entity owning two of the top four network affiliates in the same market harms competition.

As Levin's analysis suggests, Slater would likely have examined Top Four divestiture conditions based on market structure analysis, independent of FCC rule changes. Under the Assefi acting regime, the dominant expectation is alignment with the FCC's ownership rulings.

The core issue: the risk that DOJ and FCC — two independent regulatory axes — converge under a single political will has grown materially. In the history of U.S. media regulation, it has been rare for both agencies to move in lockstep on a major broadcast deal under the same political and interpretive framework. In the past, FCC (applying public interest and ownership rules) and DOJ (applying antitrust and market competition standards) served as mutual checks. That structural check is now in question.

Implications for K-content companies entering the U.S. market:

The U.S. TV broadcast regulatory environment has limited direct impact on K-content operators. But indirect structural effects — on distribution, advertising markets, and retransmission dynamics — deserve close attention.

Relying on a dual-review risk hedge — assuming one agency will restrain what the other allows — may no longer be reliable. When FCC and DOJ can align rapidly under the same political-industrial policy direction, the assumption that "one side will hold the line" does not hold.

Broadcast content partnerships, channel acquisition, and joint venture or M&A structures must account not only for individual deal competition and ownership risk, but also for the scenario in which regulatory lines shift rapidly with changes in administration and personnel.

Long-term contracts or equity partnerships with major broadcast groups or local coalitions carry the risk of backlash if the U.S. regulatory climate swings back toward anti-consolidation and pro-independence. Contract structure should include policy risk provisions: exit clauses, renegotiation triggers for regulatory changes, and legal/financial architecture that absorbs such shifts.

K-EnterTechHub Outlook: Three Scenarios

The Nexstar–TEGNA merger is not a story confined to U.S. broadcast industry restructuring. It is a structural shift that K-content operators and Korean media companies targeting the U.S. market must urgently re-examine in terms of partner selection, syndication strategy, and advertising positioning. The three scenarios below reflect K-EnterTech Hub's baseline assessment, incorporating current FCC, DOJ, and congressional dynamics.

S1

High

Conditional Approval — Deal Closes in 2026

FCC effectively neutralizes the 39% cap via waiver or rulemaking; DOJ approves with limited divestitures in a handful of smaller markets. Nexstar emerges as a super local broadcaster covering 50%+ of U.S. households. For K-content, deal-making with the "#1 local coalition" becomes the baseline for U.S. broadcast syndication, local advertising/sponsorship, and sports/entertainment format licensing. How to structure package deals not just with national networks but with a local super-group becomes a core question in K-content's U.S. broadcast entry strategy.

S2

Medium

Litigation — Years of Uncertainty

Opponents including Newsmax file as threatened; courts question the administrative basis for waiving the statutory 39% cap. Regardless of FCC approval, deal closing is delayed for years. U.S. broadcast M&A broadly enters a watch-and-wait freeze. For K-content, a fixed local broadcaster landscape persists for several years, but regulatory risk keeps mega-deals constrained — requiring sustained parallel partnerships across multiple mid-size groups, FAST channels, cable, and streaming.

S3

Low

Congressional Legislation — Slowest but Most Durable

Congress adjusts the statutory cap or explicitly delegates waiver authority to the FCC. Takes the longest to realize, but once enacted provides clear legal precedent and predictability for future similar transactions. Broadcast ownership rules are then organized into a clean three-tier structure: statute → FCC regulation → individual deal conditions. K-content operators can design long-term partnerships, joint channels, and co-investment structures on a legal framework less vulnerable to shifts in administration or political climate.

The moment FCC Chairman Carr's promised document is released — the one he told reporters to "stay tuned" for — a new chapter in U.S. broadcast regulation begins.

And that chapter will redraw the balance of power between national networks and local broadcaster coalitions, between linear broadcast and streaming/FAST, between super-groups and independent channels. When it does, it will also require the K-content industry to redraw the strategic map through which it reads the American media market.

Jung Han

Jung Han

![[보고서]전통 언론사의 크리에이터 전략 대전환](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/02/0nwc9z_202602100212.png)