유튜브 1위·FAST의 역습… '포스트 넷플릭스' 시대, K-콘텐츠 유통 공식이 바뀐다

by

2026년 2월 19일

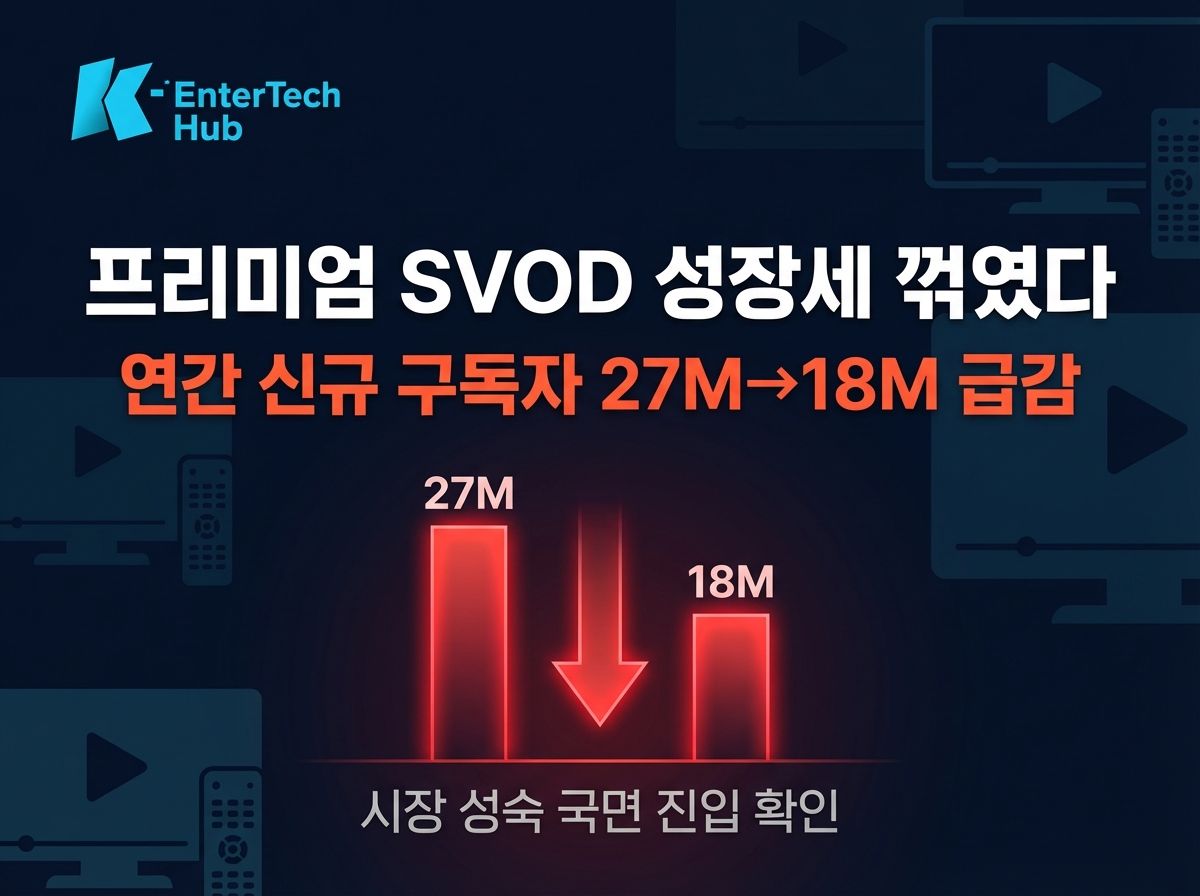

Annual net new subscribers plunge from 27M to 18M — signaling a market maturity inflection point

The U.S. premium subscription streaming (SVOD) market has officially crossed into maturity. Year-over-year subscription growth across major platforms — including Netflix, Disney+, and HBO Max — decelerated sharply from 12% in Q4'24 to just 7% in Q4'25, while net new subscribers over the same period dropped 33%, from 27 million to 18 million. As market saturation, price hikes, and the rise of free ad-supported streaming (FAST) converge, the growth engine that powered the streaming revolution is clearly losing momentum.

Jung Han

Jung Han

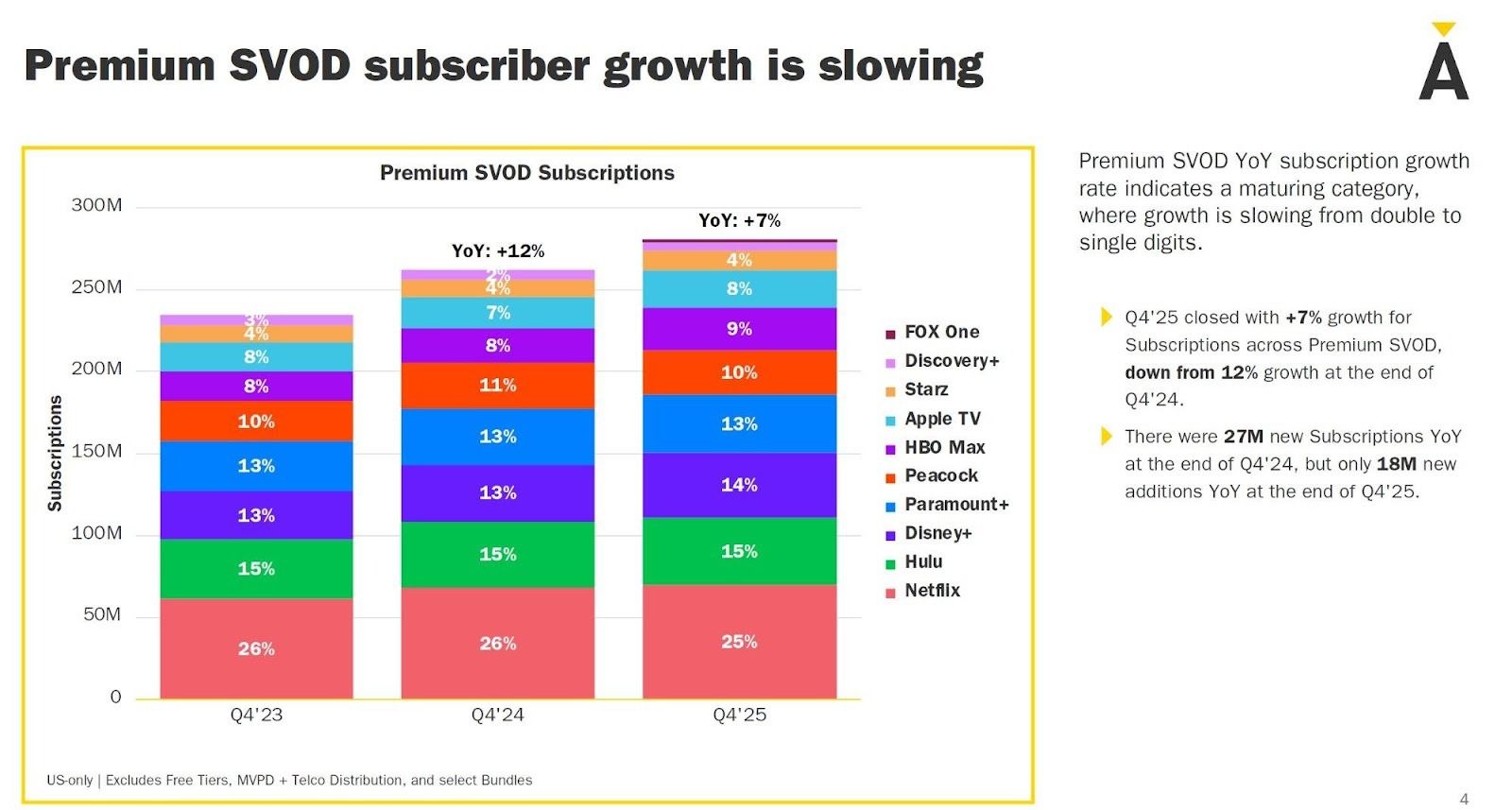

▲ U.S. Premium SVOD Subscriptions by Platform, Q4'23–Q4'25 | Source: Ampere Analysis (Excludes free tiers, MVPD & telco distribution, and select bundles)

According to data from Ampere Analysis, total U.S. premium SVOD subscriptions grew steadily from approximately 230 million in Q4'23 to 258 million in Q4'24, and reached roughly 276 million by Q4'25. On the surface, the trajectory looks healthy. But beneath the headline numbers, the growth mechanics are deteriorating.

The year-over-year growth rate fell from 12% to 7% in just twelve months — a transition from double-digit to single-digit expansion that industry analysts widely interpret as the hallmark of a maturing category. More telling is the collapse in net new subscribers: the market added 27 million new subscriptions in the year ending Q4'24, but only 18 million in the year ending Q4'25. That's a 33% drop in incremental demand in a single year.

The platform share structure remained broadly stable across the three quarters examined. Netflix maintained its commanding lead at 25–26% of total subscriptions, with Hulu holding steady in second at around 15%. Disney+ and Paramount+ each held 13–14%, while Max (HBO Max) showed the most notable momentum — expanding its share from 8% to 11% over the period.

Peacock stayed flat at 10% and Apple TV+ remained range-bound at 8–9%, both struggling to find a breakout growth catalyst. Starz and Discovery+ each occupied the 2–4% range at the bottom of the stack. The overall picture is one of consolidation: the top three or four platforms are cementing their oligopoly while mid-tier services face mounting pressure to differentiate or merge.

The data reflects a broader strategic shift underway across the industry — from chasing subscriber counts to maximizing revenue per user. Netflix's password-sharing crackdown and the industry-wide rollout of ad-supported tiers are not coincidental; they are deliberate responses to a market where marginal subscriber acquisition has become expensive and unreliable.

As platforms shift their KPIs from gross subscriber additions to ARPU (average revenue per user) and engagement depth, content procurement strategies will inevitably tighten. Studios and independent producers should expect more selective greenlight decisions, shorter content deals, and intensified negotiation pressure on licensing fees.

For the Korean content industry, the SVOD slowdown is both a warning and an opportunity. As premium platforms prioritize cost efficiency over volume, K-drama and K-variety productions competing for SVOD deals may face tighter budgets and harder terms. The strategic reliance on a handful of global streaming gatekeepers is becoming increasingly risky.

The FAST channel market offers a compelling alternative. Projected to grow from $5.8 billion in 2025 to $10.6 billion by 2030, FAST is expanding at double-digit rates precisely as SVOD stagnates. K-content owners with an established global fanbase — built in part through SVOD exposure — are uniquely positioned to launch or license dedicated FAST channels, capturing advertising revenue while maintaining direct-to-consumer distribution. The window to act is now.

* Data covers paid U.S. subscriptions only. Excludes free tiers, MVPD & telco distribution, and select bundles.

* Source: Ampere Analysis | Analysis & Commentary: K-EnterTech Hub

![[보고서]전통 언론사의 크리에이터 전략 대전환](https://cdn.media.bluedot.so/bluedot.kentertechhub/2026/02/0nwc9z_202602100212.png)